Poll tax

A poll tax, also known as head tax or capitation, is a tax levied as a fixed sum on every liable individual.[1]

Head taxes were important sources of revenue for many governments from ancient times until the 19th century. In the United Kingdom, poll taxes were levied by the governments of John of Gaunt in the 14th century, Charles II in the 17th and Margaret Thatcher in the 20th century. In the United States, voting poll taxes (whose payment was a precondition to voting in an election) have been used to disenfranchise impoverished and minority voters (especially under Reconstruction).[2]

By their very nature, poll taxes are considered very regressive taxes, are usually very unpopular and have been implicated in many uprisings.

The word "poll" is an archaic term for "head" or "top of the head". The sense of "counting heads" is found in phrases like polling place and opinion poll.[3]

Religious law

Mosaic law

As prescribed in Exodus (30: 11-16) Jewish law imposed a poll tax of half-shekel, payable by every man above the age of twenty ("the rich shall not pay more and the poor shall not pay less").

Exodus 30:11-16:

11 And the LORD spake unto Moses, saying,

12 When thou takest the sum of the children of Israel after their number, then shall they give every man a ransom for his soul unto the LORD, when thou numberest them; that there be no plague among them, when thou numberest them.

13 This they shall give, every one that passeth among them that are numbered, half a shekel after the shekel of the sanctuary: (a shekel is twenty gerahs:) an half shekel shall be the offering of the LORD.

14 Every one that passeth among them that are numbered, from twenty years old and above, shall give an offering unto the LORD.

15 The rich shall not give more, and the poor shall not give less than half a shekel, when they give an offering unto the LORD, to make an atonement for your souls.

16 And thou shalt take the atonement money of the children of Israel, and shalt appoint it for the service of the tabernacle of the congregation; that it may be a memorial unto the children of Israel before the LORD, to make an atonement for your souls. (Authorized Version)

The money was designated for the Tabernacle in the Exodus narrative and later for the upkeep of the Temple of Jerusalem. Priests, women, slaves and minors were exempted, although they could offer it voluntarily. Payment by Samaritans or Gentiles was rejected. It was collected yearly during the month of Adar, both at the Temple and at special collection bureaux in the provinces.

Islamic law

Zakat al-Fitr is an obligatory charity that must be given by every Muslim (or their guardian) near the end of every Ramadan. Muslims in dire poverty are exempt from it.[4] The amount is 2 kg of wheat or barley, or its cash equivalent. Zakat al-Fitr is to be given to the poor.[5]

Jizya was a poll tax imposed under Islamic law on non-Muslims permanently residing in a Muslim state as part of their dhimmi status. The tax is levied on free-born abled-bodied men of military age. The indigent were exempt, as well as slaves, women, children, the old, the sick, monks and hermits.

Several rationales for the jizya have been advanced. They include the argument that jizya was a fee in exchange for the dhimma (permission to practice one's faith, enjoy communal autonomy, and to be entitled to Muslim protection from outside aggression), and the argument that imposition of jizya on non-Muslims is similar to the imposition of zakat (one of the Five Pillars of Islam, an obligatory wealth tax paid on certain assets which are not used productively for a period of a year) on Muslims.

Although jizya is often called a poll tax, its assessment and collection was commonly qualified by income. For instance, Amr ibn al-As, after conquering Egypt, set up a census to measure the population for the jizya, and thus the total expected jizya revenue for the whole province, but organized the actual collection by partitioning the population into wealth classes, so that the rich paid more and the poor less jizya of that total sum. Elsewhere, it is reported customary to partition into three classes, e.g. 48 dirhams for the rich, 24 for middle class and 12 for the poor.[6]

In 1855, the Ottoman Empire abolished the jizya tax, as part of reforms to equalize the status of Muslims and non-Muslims. It was replaced by a military-exemption tax on non-Muslims, the Bedel-i Askeri.

Canada

The Chinese head tax was a fixed fee charged to each Chinese person entering Canada. The head tax was first levied after the Canadian parliament passed the Chinese Immigration Act of 1885 and was meant to discourage Chinese people from entering Canada after the completion of the Canadian Pacific Railway. The tax was abolished by the Chinese Immigration Act of 1923, which stopped all Chinese immigration except for business people, clergy, educators, students, and other categories.[7]

Ceylon

In Ceylon, a Poll tax was levied by the British colonial government of Ceylon in 1920. The tax charged 2 Rupees per year per male adult. Those who did not pay had to work on the roads for one day in lieu of the tax. The Young Lanka League protested the tax, lead by A. Ekanayake Gunasinha, and it was repealed by the Legislative Council of Ceylon in 1925 following a motion submitted by C. H. Z. Fernando.[8]

Great Britain

The poll tax was essentially a lay subsidy, a tax on the movable property of most of the population, to help fund war. It had first been levied in 1275 and continued under different names until the 17th century. People were taxed a percentage of the assessed value of their movable goods. That percentage varied from year to year and place to place, and which goods could be taxed differed between urban and rural locations. Churchmen were exempt, as were the poor, workers in the Royal Mint, inhabitants of the Cinque Ports, tin workers in Cornwall and Devon, and those who lived in the Palatinate counties of Cheshire and Durham.

14th century

The Hilary Parliament, held between January and March 1377, levied a poll tax in 1377 to finance the war against France at the request of John of Gaunt who, since King Edward III was mortally sick, was the de facto head of government at the time. This tax covered almost 60% of the population, far more than lay subsidies had earlier. It was levied two more times, in 1379 and 1381. Each time the taxation basis was slightly different. In 1377, every lay person over the age of 14 years who was not a beggar had to pay a groat (4d) to the Crown. By 1379 that had been graded by social class, with the lower age limit changed to 16, and to 15 two years later. The levy of 1381 operated under a combination of both flat rate and graduated assessments. The minimum amount payable was set at 4d, however tax collectors had to account for a 12d a head mean assessment. Payments were therefore variable; the poorest would theoretically pay the lowest rate, with the deficit being met by a higher payment from those able to afford it.[9] The 1381 tax has been credited as one of the main reasons behind the Peasants' Revolt in that year, due in part to attempts to restore feudal conditions in rural areas.

17th century

The poll tax was resurrected during the 17th century, usually related to a military emergency. It was imposed by Charles I in 1641 to finance the raising of the army against the Scottish and Irish uprisings. With the Restoration of Charles II in 1660, the Convention Parliament of 1660 instituted a poll tax to finance the disbanding of the New Model Army (pay arrears, etc.) (12 Charles II c.9).[10] The poll tax was assessed according to "rank", e.g. dukes paid £100, earls £60, knights £20, esquires £10. Eldest sons paid 2/3rds of their father's rank, widows paid a third of their late husband's rank. The members of the livery companies paid according to company's rank (e.g. masters of first-tier guilds like the Mercers paid £10, whereas masters of fifth-tier guilds, like the Clerks, paid 5 shillings). Professionals also paid differing rates, e.g. physicians (£10), judges (£20), advocates (£5), attorneys (£3), and so on. Anyone with property (land, etc.) paid 40 shillings per £100 earned, anyone over the age of 16 and unmarried paid twelvepence and everyone else over 16 paid sixpence.

The poll tax was imposed again by William III and Mary II in 1689 (1 Will. & Mar. c.13), reassessed in 1690 adjusting rank for fortune, and then again in 1691 back to rank irrespective of fortune. The poll tax was imposed again in 1692, and one final time in 1698 (the last poll tax in England until the 20th century). A poll tax was imposed on Scotland between 1694 and 1699.

As the greater weight of the 17th century poll taxes fell primarily upon the wealthy and powerful, it was not too unpopular. There were grumblings within the taxed ranks about lack of differentiation by income within ranks. Ultimately, it was the inefficiency of their collection (what they brought in routinely fell far short of expected revenues) that prompted the government to abandon the poll tax after 1698.

Far more controversial was the hearth tax introduced in 1662 (13 & 14 Charles II c.10), which imposed a hefty two shillings on every hearth in a family dwelling, which was easier to count than persons. Heavier, more permanent and more regressive than the poll tax proper, the intrusive entry of tax inspectors into private homes to count hearths was a very sore point, and it was promptly repealed with the Glorious Revolution in 1689. It was replaced with a "window tax" in 1695 since inspectors could count windows from outside homes.

20th century

The Community Charge, popularly dubbed the "poll tax", was a tax to fund local government, instituted in 1989 by the government of Margaret Thatcher. It replaced the rates that were based on the notional rental value of a house. The abolition of rates was in the Conservative Party manifesto for the 1979 general election; the replacement was proposed in the Green Paper of 1986, Paying for Local Government based on ideas developed by Dr. Madsen Pirie and Douglas Mason of the Adam Smith Institute.[11] It was a fixed tax per adult resident, but there was a reduction for those with lower household income. Each person was to pay for the services provided in their community. This proposal was contained in the Conservative Party manifesto for the 1987 general election. The new tax replaced the rates in Scotland from the start of the 1989/90 financial year and in England and Wales from the start of the 1990/91 financial year.[12]

The system was very unpopular since many thought it shifted the tax burden from the rich to the poor, as it was based on the number of occupants living in a house, rather than on the estimated market value of the house. Many tax rates set by local councils proved to be much higher than earlier predictions since the councils realised that not they but the central government would be blamed for the tax, which led to resentment, even among some who had supported the introduction of it.[13] The tax in different boroughs differed because local taxes paid by businesses varied and grants by central government to local authorities sometimes varied capriciously.

Mass protests were called by the All Britain Anti-Poll Tax Federation with which the vast majority of local Anti-Poll Tax Unions (APTUs) were affiliated. In Scotland, the APTUs called for mass nonpayment, which rapidly gathered widespread support and spread as far as England and Wales even though no-payment meant that people could be prosecuted. In some areas, 30% of former ratepayers defaulted. While owner-occupiers were easy to tax, nonpayers who regularly changed accommodation were almost impossible to trace. The cost of collecting the tax rose steeply, and its returns fell. Unrest grew and resulted in a number of poll tax riots. The most serious was in a protest at Trafalgar Square, London, on 31 March 1990, of more than 200,000 protesters. Terry Fields, Labour MP for Liverpool Broadgreen, was jailed for 60 days for his refusal to pay the poll tax.[14][15]

This unrest was a factor in the fall of Thatcher. Her successor, John Major, replaced the Community Charge with the Council Tax, similar to the rating system that preceded the Community Charge.[16] The main differences were that it was levied on capital value rather than notional rental value of a property, and that it had a 25% discount for single-occupancy dwellings.[17]

In 2015, Lord Waldegrave reflected in his memoirs that the Community Charge was all his own work and that it was a serious mistake. Although he felt the policy looked like it would work, it was implemented differently from his predictions "They went gung-ho and introduced it overnight in one go, which was never my plan and I thought they must know what they were doing - but they didn't."[18]

France

In France, a poll tax, the capitation, was first imposed by King Louis XIV in 1695 as a temporary measure to finance the War of the League of Augsburg, and thus repealed in 1699. It was resumed during the War of Spanish Succession and in 1704 set on a permanent basis, remaining until the end of the Ancien regime.

Like the English poll tax, the French capitation tax was assessed on rank – for taxation persons, French society was divided in twenty-two "classes", with the Dauphin (a class by himself) paying 2,000 livres, princes of the blood paying 1500 livres, and so on down to the lowest class, composed of day laborers and servants, who paid 1 livre each. The bulk of the common population was covered by four classes, paying 40, 30, 10 and 3 livres respectively. Unlike most other direct French taxes, nobles and clergy were not exempted from capitation taxes. It did, however, exempt the mendicant orders and the poor who contributed less than 40 sous.

The French clergy managed to temporarily escape capitation assessment by promising to pay a total sum of 4 million livres per annum in 1695, and then obtained permanent exemption in 1709 with a lump sum payment of 24 million livres. The Pays d'états (Brittany, Burgundy, etc.) and many towns also escaped assessment by promising annual fixed payments. The nobles did not escape assessment, but they obtained the right to appoint their own capitation tax assessors, which allowed them to escape most of the burden (in one calculation, they escaped 7⁄8 of it).

Compounding the burden, the assessment on the capitation did not remain stable. The pays de taille personelle (basically, Pays d'élection, the bulk of France and Aquitaine) secured the ability to assess the capitation tax proportionally to the taille – which effectively meant adjusting the burden heavily against the lower classes. According to the estimates of Jacques Necker in 1788, the capitation tax was so riddled in practice, that the privileged classes (nobles and clergy and towns) were largely exempt, while the lower classes were heavily crushed: the lowest peasant class, originally assessed to pay 3 livres, were now paying 24, the second lowest, assessed at 10 livres, were now paying 60 and the third-lowest assessed at 30 were paying 180. The total collection from the capitation, according to Necker in 1788, was 41 million livres, well short of the 54 million estimate, and it was projected that the revenues could have doubled if the exemptions were revoked and the original 1695 assessment properly restored.

The old capitation tax was repealed with the French Revolution and replaced, on 13 January 1791,[19] with a new poll tax as part of the contribution personnelle mobilière, which lasted well into the late 19th century. It was fixed for every individual at "three days's labor" (assessed locally, but by statute, no less than 1 franc 50 centimes and no more than 4 francs 50 centimes, depending on the area). A dwelling tax (impôt sur les portes et fenêtres, similar to the English window-tax) was imposed in 1798.

New Zealand

New Zealand imposed a poll tax on Chinese immigrants during the 19th and early 20th centuries as part of their broader efforts to reduce the number of Chinese immigrants. [20] The poll tax was effectively lifted in the 1930s following the invasion of China by Japan, and was finally repealed in 1944. Prime Minister Helen Clark offered New Zealand's Chinese community an official apology for the poll tax on 12 February 2002.[21]

Poland–Lithuania

The Jewish poll tax was a poll tax imposed on the Jews in Polish–Lithuanian Commonwealth. It was later absorbed into the hiberna tax.[22][23]

Roman Empire

The ancient Romans imposed a tributum capitis (poll tax) as one of the principal direct taxes on the peoples of the Roman provinces (Digest 50, tit.15). In the Republican period, poll taxes were principally collected by private tax farmers (publicani), but from the time of Emperor Augustus, the collections were gradually transferred to magistrates and the senates of provincial cities. The Roman census was conducted periodically in the provinces to draw up and update the poll tax register.

The Roman poll tax fell principally on Roman subjects in the provinces, but not on Roman citizens. Towns in the provinces who possessed the Jus Italicum (enjoying the "privileges of Italy") were exempted from the poll tax. The 212 edict of Emperor Caracalla (which formally conferred Roman citizenship on all residents of Roman provinces) did not, however, exempt them from the poll tax.

The Roman poll tax was deeply resented—Tertullian bewailed the poll tax as a "badge of slavery"—and it provoked numerous revolts in the provinces. Perhaps most famous is the Zealot revolt in Judaea of 66 AD. After the destruction of the temple in 70 AD, the Emperor Vespasian imposed an extra poll tax on Jews throughout the empire, the fiscus judaicus, of two denarii each.

The Italian revolt of the 720s, organized and led by Pope Gregory II, was originally provoked by the attempt of the Constantinople Emperor Leo III the Isaurian to introduce a poll tax in the Italian provinces of the Byzantine Empire in 722, and set in motion the permanent separation of Italy from the Byzantine empire. When King Aistulf of the Lombards availed himself of the Italian dissent and invaded the Exarchate of Ravenna in 751, one of his first acts was to institute a crushing poll tax of one gold solidus per head on every Roman citizen. Seeking relief from this burden, Pope Stephen II appealed to Pepin the Short of the Franks for assistance, that led to the establishment of the Papal States in 756.

Russia

The Russian Empire imposed a poll tax in 1718.[24] Nikolay Bunge, Finance Minister from 1881 to 1886 under Emperor Alexander III, abolished it in 1886.[25]

United States

Poll tax

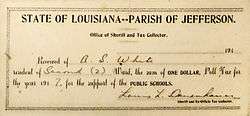

Prior to the mid 20th century, a poll tax was implemented in some U.S. state and local jurisdictions and paying it was a requirement before one could exercise one's right to vote. After this right was extended to all races by the Fifteenth Amendment to the Constitution, many Southern states enacted poll taxes as a means of excluding African-American voters, most of whom were poor and unable to pay a tax. So as not to disenfranchise the many poor whites, such laws typically included a grandfather clause, exempting from the tax any adult male whose father or grandfather had voted. The effect was to exempt whites from the tax blacks had to pay, because no black fathers or grandfathers had been able to vote. The poll tax, along with literacy tests and extra-legal intimidation,[26] achieved the desired effect of disenfranchising African Americans. Often in US discussions, the term poll tax is used to mean a tax that must be paid in order to vote, rather than a capitation tax simply. (For example, a bill that passed the Florida House of Representatives in April 2019 has been compared to a poll tax because it requires former felons to pay all "financial obligations" related to their sentence, including court fines, fees, and judgments, before their voting rights will be restored as required by a referendum that passed with 64% of the vote in 2018.[27][28]) The Twenty-fourth Amendment, ratified in 1964, prohibits both Congress and the states from conditioning the right to vote on payment of a poll tax or any other type of tax.

Capitation and federal taxation

The ninth section of Article One of the Constitution places several limits on Congress's powers. Among them: "No capitation, or other direct, tax shall be laid, unless in proportion to the census or enumeration herein before directed to be taken". Capitation here means a tax of a uniform, fixed amount per taxpayer.[29] Direct tax means a tax levied directly by the United States federal government on taxpayers, as opposed to a tax on events or transactions.[30] The United States government levied direct taxes from time to time during the 18th and early 19th centuries. It levied direct taxes on the owners of houses, land, slaves and estates in the late 1790s but cancelled the taxes in 1802.

An income tax is neither a poll tax nor a capitation, as the amount of tax will vary from person to person, depending on each person's income. Until a United States Supreme Court decision in 1895, all income taxes were deemed to be excises (i.e., indirect taxes). The Revenue Act of 1861 established the first income tax in the United States, to pay for the cost of the American Civil War. This income tax was abolished after the war, in 1872. Another income tax statute in 1894 was overturned in Pollock v. Farmers' Loan & Trust Co. in 1895, where the Supreme Court held that income taxes on income from property, such as rent income, interest income, and dividend income (however excepting income taxes on income from "occupations and labor" if only for the reason of not having been challenged in the case, "We have considered the act only in respect of the tax on income derived from real estate, and from invested personal property") were to be treated as direct taxes. Because the statute in question had not apportioned income taxes on income from property by population, the statute was ruled unconstitutional. Finally, ratification of the Sixteenth Amendment to the United States Constitution in 1913 made possible modern income taxes, by limiting the Sixteenth Amendment income tax to the class of indirect excises (i.e. excises, duties, and imposts) – thus requiring no apportionment,[31] [32] a practice that would remain unchanged into the 21st century.

Employment-based head taxes

Various cities, including Chicago and Denver, have levied head taxes with a set rate per employee targeted at large employers.[33][34] After Cupertino postponed head tax proposals to 2020, Mountain View became the only city in Silicon Valley, California, to continue to pursue such type of taxes.[35]

In 2018, the Seattle city council proposed a "head tax" of $500 per year per employee.[36][37][38] The proposed tax was lowered to $275 per year per employee, was passed, and became "the biggest head tax in U.S. history,"[39] though it was repealed less than a month later.

References

- "poll tax". Oxford World Encyclopedia. Philip's. 2004. ISBN 9780199546091.

- Franklin, John Hope (1961). Reconstruction After the Civil War. U. of Chicago Press. pp. 127–151. OCLC 5845934.

- Moon, Nick (1999). Opinion Polls: History, Theory and Practice. Manchester University Press. p. 2. ISBN 0-7190-4224-0.

- Keskin, Tugrul, ed. (2012). The Sociology of Islam: Secularism, Economy and Politics. Ithaca Press. p. 449. ISBN 0-86372-425-6.

- Yvonne Yazbeck Haddad, Jane I. Smith (2014). The Oxford Handbook of American Islam. p. 166.

- Hassan, Abul; Choudhury, M. A. (2019). Islamic Economics: Theory and Practice. London: Routledge. p. 247. ISBN 978-1-138-36241-3.

- James Morton. "In the Sea of Sterile Mountains: The Chinese in British Columbia". Vancouver, BC: J.J. Douglas, 1974.

- Ekanayake Goonesinha, Kesera. "A. E. Goonesinha - May Day hero and Father of the Trade Union Movement". Daily News. Retrieved 6 August 2020.

- See Fenwick, Carolyn Christine (1983). The English Poll Taxes of 1377, 1379 and 1381: A Critical Examination of the Returns (PhD thesis). London School of Economics and Political Science (University of London).

- Statutes of the Realm, vol. v, p.207-225

- Pearce, Ed (19 April 1993). "The prophet of private profit". The Guardian.

- Collins, Nick (9 March 2011). "Local government funding timeline: From rates to poll tax to council tax". The Daily Telegraph.

- Smith, Peter (December 1991). "Lessons From the British Poll Tax Disaster" (PDF). National Tax Journal. 44 (4): 421–436.

- Chaplain, Chloe (22 October 2018). "The biggest protests in recent history... and the impact they had". inews.co.uk. Archived from the original on 14 October 2019. Retrieved 14 October 2019.

- Wheal, Chris (14 April 1999). "Poll tax is history". The Guardian.

- Higham, Nick (30 December 2016). "Thatcher's Community Charge miscalculation". BBC News.

- Waterhouse, Rosie (13 September 1992). "Uproar predicted over council tax". The Independent.

- "Poll tax a mistake, says Waldegrave". BBC News. 20 July 2015.

- Jones, Colin (2014). The Longman Companion to the French Revolution. Routledge. p. 15. ISBN 978-1-317-87080-7.

- https://natlib.govt.nz/events/the-poll-tax-on-chinese-in-new-zealand-what-s-it-all-about-november-06-2019

- New Zealand Office of Ethnic Affairs (2002). "Chinese Poll Tax in New Zealand – Formal Apology". New Zealand Department of Internal Affairs. Retrieved 18 August 2006.

- Scepter of Judah: The Jewish Autonomy in the Eighteenth-Century Crown Poland, pp. 15-16

- The Cambridge Dictionary of Judaism and Jewish Culture, p. 118 (browse for "skhumot" online)

- Vidal-Naquet, Pierre, ed. (1987). The Collins Atlas of World History. Great Britain: William Collins Sons & Co Ltd. p. 178. ISBN 978-0-00-217776-4.

- Holland, Andy (2010). Russia and its rulers 1855–1964. Access to History. Great Britain: Hodder Education. p. 126. ISBN 978-0-340-98370-6.

- "Civil Rights Movement -- Literacy Tests & Voter Applications". Archived from the original on 16 November 2015. Retrieved 19 October 2014.

- Judge, Monique. "Is This the New Poll Tax? Florida House Passes Bill Requiring Former Felons to Pay Up Before They Can Vote". The Root. Retrieved 25 April 2019.

- "Over 1 Million Florida Felons Win Right To Vote With Amendment 4". NPR.org. Retrieved 25 April 2019.

- United States Department of State (2004). "The Constitution of the United States of America with Explanatory Notes". US Department of State web site. United States. Archived from the original on 14 May 2008. Retrieved 18 May 2008.

- United States Department of the Treasury. "History of the U.S. Tax System". US Treasury Department : Education : Fact Sheets : Taxes. United States. Archived from the original on 27 November 2010. Retrieved 4 August 2009.

- "BRUSHABER v. UNION PACIFIC R. CO., 240 U.S. 1 (1916)". FindLaw : Supreme Court. FindLaw.

- "STANTON v. BALTIC MINING CO, 240 U.S. 103 (1916)". FindLaw : Supreme Court. FindLaw.

- "Seattle head tax: How 2 other big cities fared". KING 5. 9 May 2018. Retrieved 12 June 2018.

- "Seattle backs new tax on largest companies, including Amazon". CNBC. Reuters. 15 May 2018. Retrieved 15 May 2018.

The head tax approved on Monday is not the first. Denver has enacted a similar tax, and Chicago had one but repealed it. Seattle itself had a head tax in effect from 2006 to 2009

- KHALIDA SARWARI (1 August 2018). "Cupertino shelves proposed 'head tax' on Apple employees for now". The Mercury News. Retrieved 2 August 2018.

The council's 4-0 decision to wait until 2020 before putting the tax proposal before voters leaves Mountain View as the only Silicon Valley city proceeding with the so-called head tax this year.

- Jessica Lee (10 May 2018). "How did we get here? A look back on Seattle's head-tax plan and Amazon's response". Seattle Times. Retrieved 11 May 2018.

The Seattle Times has reported on the so-called "head tax" proposal

- "Seattle head tax 101: What to know about the proposal". MyNorthwest. Retrieved 11 May 2018.

The Seattle had tax proposal is an employee hours tax

- "NEW SEATTLE HEAD TAX PROPOSAL SETS UP POTENTIAL CLASH IN COUNCIL MEETING TODAY". KING 5. 11 May 2018. Retrieved 11 May 2018.

A new proposal to Seattle City Council's controversial head tax legislation could bring a compromise

- Chris Daniels; Natalie Brand (14 May 2018). "Seattle Mayor Durkan vows to sign head tax compromise". KGW. Retrieved 15 May 2018.

The head tax is the largest in U.S. history

External links

| Look up head tax in Wiktionary, the free dictionary. |

- Middle Ages Poll Tax

- Pictures by Paul Ross, who witnessed the riots

- The battle that brought down Thatcher – a perspective by the Trotskyist Militant group

| By owner | |||||

|---|---|---|---|---|---|

| By nature | |||||

| Commons | |||||

| Theory | |||||

| Applications |

| ||||

| Disposession/ redistribution | |||||

| Scholars (key work) | |||||

| |||||