Theory of the firm

The theory of the firm consists of a number of economic theories that explain and predict the nature of the firm, company, or corporation, including its existence, behaviour, structure, and relationship to the market.[1]

Overview

In simplified terms, the theory of the firm aims to answer these questions:

- Existence. Why do firms emerge? Why are not all transactions in the economy mediated over the market?

- Boundaries. Why is the boundary between firms and the market located exactly there with relation to size and output variety? Which transactions are performed internally and which are negotiated on the market?

- Organization. Why are firms structured in such a specific way, for example as to hierarchy or decentralization? What is the interplay of formal and informal relationships?

- Heterogeneity of firm actions/performances[2]. What drives different actions and performances of firms?

- Evidence. What tests are there for respective theories of the firm?[3]

Firms exist as an alternative system to the market-price mechanism when it is more efficient to produce in a non-market environment. For example, in a labor market, it might be very difficult or costly for firms or organizations to engage in production when they have to hire and fire their workers depending on demand/supply conditions. It might also be costly for employees to shift companies every day looking for better alternatives. Similarly, it may be costly for companies to find new suppliers daily. Thus, firms engage in a long-term contract with their employees or a long-term contract with suppliers to minimize the cost or maximize the value of property rights.[4][5][6]

Background

The First World War period saw change of emphasis in economic theory away from industry-level analysis which mainly included analyzing markets to analysis at the level of the firm, as it became increasingly clear that perfect competition was no longer an adequate model of how firms behaved. Economic theory until then had focused on trying to understand markets alone and there had been little study on understanding why firms or organisations exist. Markets are guided by prices and quality as illustrated by vegetable markets where a buyer is free to switch sellers in an exchange.

The need for a revised theory of the firm was emphasized by empirical studies by Adolf Berle and Gardiner Means, who made it clear that ownership of a typical American corporation is spread over a wide number of shareholders, leaving control in the hands of managers who own very little equity themselves.[7] R. L. Hall and Charles J. Hitch found that executives made decisions by rule of thumb rather than in the marginalist way.[8]

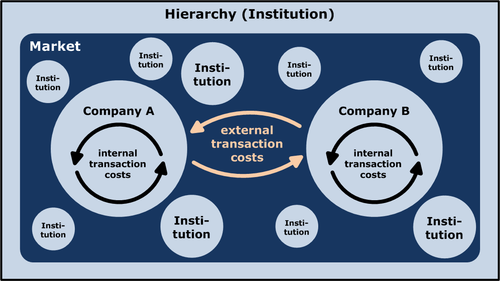

Transaction cost theory

According to Ronald Coase, people begin to organise their production in firms when the transaction cost of coordinating production through the market exchange, given imperfect information, is greater than within the firm.[4]

Ronald Coase set out his transaction cost theory of the firm in 1937, making it one of the first (neo-classical) attempts to define the firm theoretically in relation to the market.[4] One aspect of its 'neoclassicism' lies in presenting an explanation of the firm consistent with constant returns to scale, rather than relying on increasing returns to scale.[9] Another is in defining a firm in a manner which is both realistic and compatible with the idea of substitution at the margin, so instruments of conventional economic analysis apply. He notes that a firm's interactions with the market may not be under its control (for instance because of sales taxes), but its internal allocation of resources are: “Within a firm, … market transactions are eliminated and in place of the complicated market structure with exchange transactions is substituted the entrepreneur … who directs production.” He asks why alternative methods of production (such as the price mechanism and economic planning), could not either achieve all production, so that either firms use internal prices for all their production, or one big firm runs the entire economy.

Coase begins from the standpoint that markets could in theory carry out all production, and that what needs to be explained is the existence of the firm, with its "distinguishing mark … [of] the supersession of the price mechanism." Coase identifies some reasons why firms might arise, and dismisses each as unimportant:

- if some people prefer to work under direction and are prepared to pay for the privilege (but this is unlikely);

- if some people prefer to direct others and are prepared to pay for this (but generally people are paid more to direct others);

- if purchasers prefer goods produced by firms.

Instead, for Coase the main reason to establish a firm is to avoid some of the transaction costs of using the price mechanism. These include discovering relevant prices (which can be reduced but not eliminated by purchasing this information through specialists), as well as the costs of negotiating and writing enforceable contracts for each transaction (which can be large if there is uncertainty). Moreover, contracts in an uncertain world will necessarily be incomplete and have to be frequently re-negotiated. The costs of haggling about division of surplus, particularly if there is asymmetric information and asset specificity, may be considerable.

If a firm operated internally under the market system, many contracts would be required (for instance, even for procuring a pen or delivering a presentation). In contrast, a real firm has very few (though much more complex) contracts, such as defining a manager's power of direction over employees, in exchange for which the employee is paid. These kinds of contracts are drawn up in situations of uncertainty, in particular for relationships which last long periods of time. Such a situation runs counter to neo-classical economic theory. The neo-classical market is instantaneous, forbidding the development of extended agent-principal (employee-manager) relationships, of planning, and of trust. Coase concludes that “a firm is likely therefore to emerge in those cases where a very short-term contract would be unsatisfactory”, and that “it seems improbable that a firm would emerge without the existence of uncertainty”.

He notes that government measures relating to the market (sales taxes, rationing, price controls) tend to increase the size of firms, since firms internally would not be subject to such transaction costs. Thus, Coase defines the firm as "the system of relationships which comes into existence when the direction of resources is dependent on the entrepreneur." We can therefore think of a firm as getting larger or smaller based on whether the entrepreneur organises more or fewer transactions.

The question then arises of what determines the size of the firm; why does the entrepreneur organise the transactions he does, why no more or less? Since the reason for the firm's being is to have lower costs than the market, the upper limit on the firm's size is set by costs rising to the point where internalising an additional transaction equals the cost of making that transaction in the market. (At the lower limit, the firm's costs exceed the market's costs, and it does not come into existence.) In practice, diminishing returns to management contribute most to raising the costs of organising a large firm, particularly in large firms with many different plants and differing internal transactions (such as a conglomerate), or if the relevant prices change frequently.

Coase concludes by saying that the size of the firm is dependent on the costs of using the price mechanism, and on the costs of organisation of other entrepreneurs. These two factors together determine how many products a firm produces and how much of each.[10]

Reconsiderations of transaction cost theory

According to Louis Putterman, most economists accept distinction between intra-firm and interfirm transaction but also that the two shade into each other; the extent of a firm is not simply defined by its capital stock.[11] George Barclay Richardson for example, notes that a rigid distinction fails because of the existence of intermediate forms between firm and market such as inter-firm co-operation.[12]

Klein (1983) asserts that “Economists now recognise that such a sharp distinction does not exist and that it is useful to consider also transactions occurring within the firm as representing market (contractual) relationships.” The costs involved in such transactions that are within a firm or even between the firms are the transaction costs.

Ultimately, whether the firm constitutes a domain of bureaucratic direction that is shielded from market forces or simply “a legal fiction”, “a nexus for a set of contracting relationships among individuals” (as Jensen and Meckling put it) is “a function of the completeness of markets and the ability of market forces to penetrate intra-firm relationships”.[13]

Managerial and behavioural theories

It was only in the 1960s that the neo-classical theory of the firm was seriously challenged by alternatives such as managerial and behavioral theories. Managerial theories of the firm, as developed by William Baumol (1959 and 1962), Robin Marris (1964) and Oliver E. Williamson (1966), suggest that managers would seek to maximise their own utility and consider the implications of this for firm behavior in contrast to the profit-maximising case. (Baumol suggested that managers’ interests are best served by maximising sales after achieving a minimum level of profit which satisfies shareholders.) More recently this has developed into ‘principal–agent’ analysis (e.g., Spence and Zeckhauser[14] and Ross (1973) on problems of contracting with asymmetric information) which models a widely applicable case where a principal (a shareholder or firm for example) cannot costlessly infer how an agent (a manager or supplier, say) is behaving. This may arise either because the agent has greater expertise or knowledge than the principal, or because the principal cannot directly observe the agent's actions; it is asymmetric information which leads to a problem of moral hazard. This means that to an extent managers can pursue their own interests. Traditional managerial models typically assume that managers, instead of maximising profit, maximise a simple objective utility function (this may include salary, perks, security, power, prestige) subject to an arbitrarily given profit constraint (profit satisficing).

Behavioural approach

The behavioural approach, as developed in particular by Richard Cyert and James G. March of the Carnegie School places emphasis on explaining how decisions are taken within the firm, and goes well beyond neoclassical economics.[15] Much of this depended on Herbert A. Simon’s work in the 1950s concerning behaviour in situations of uncertainty, which argued that “people possess limited cognitive ability and so can exercise only ‘bounded rationality’ when making decisions in complex, uncertain situations”. Thus individuals and groups tend to "satisfice"—that is, to attempt to attain realistic goals, rather than maximize a utility or profit function. Cyert and March argued that the firm cannot be regarded as a monolith, because different individuals and groups within it have their own aspirations and conflicting interests, and that firm behaviour is the weighted outcome of these conflicts. Organisational mechanisms (such as "satisficing" and sequential decision-taking) exist to maintain conflict at levels that are not unacceptably detrimental. Compared to ideal state of productive efficiency, there is organisational slack (Leibenstein's X-inefficiency).

Team production

Armen Alchian and Harold Demsetz's analysis of team production extends and clarifies earlier work by Coase.[16] Thus according to them the firm emerges because extra output is provided by team production, but that the success of this depends on being able to manage the team so that metering problems (it is costly to measure the marginal outputs of the co-operating inputs for reward purposes) and attendant shirking (the moral hazard problem) can be overcome, by estimating marginal productivity by observing or specifying input behaviour. Such monitoring as is therefore necessary, however, can only be encouraged effectively if the monitor is the recipient of the activity's residual income (otherwise the monitor herself would have to be monitored, ad infinitum). For Alchian and Demsetz, the firm therefore is an entity which brings together a team which is more productive working together than at arm's length through the market, because of informational problems associated with monitoring of effort. In effect, therefore, this is a "principal-agent" theory, since it is asymmetric information within the firm which Alchian and Demsetz emphasise must be overcome. In Barzel (1982)’s theory of the firm, drawing on Jensen and Meckling (1976), the firm emerges as a means of centralising monitoring and thereby avoiding costly redundancy in that function (since in a firm the responsibility for monitoring can be centralised in a way that it cannot if production is organised as a group of workers each acting as a firm).

The weakness in Alchian and Demsetz’s argument, according to Williamson, is that their concept of team production has quite a narrow range of application, as it assumes outputs cannot be related to individual inputs. In practice this may have limited applicability (small work group activities, the largest perhaps a symphony orchestra), since most outputs within a firm (such as manufacturing and secretarial work) are separable, so that individual inputs can be rewarded on the basis of outputs. Hence team production cannot offer the explanation of why firms (in particular, large multi-plant and multi-product firms) exist.

Asset specificity

For Oliver E. Williamson, the existence of firms derives from ‘asset specificity’ in production, where assets are specific to each other such that their value is much less in a second-best use.[17] This causes problems if the assets are owned by different firms (such as purchaser and supplier), because it will lead to protracted bargaining concerning the gains from trade, because both agents are likely to become locked into a position where they are no longer competing with a (possibly large) number of agents in the entire market, and the incentives are no longer there to represent their positions honestly: large-numbers bargaining is transformed into small-number bargaining.

If the transaction is a recurring or lengthy one, re-negotiation may be necessary as a continual power struggle takes place concerning the gains from trade, further increasing the transaction costs. Moreover, there are likely to be situations where a purchaser may require a particular, firm-specific investment of a supplier which would be profitable for both; but after the investment has been made it becomes a sunk cost and the purchaser can attempt to re-negotiate the contract such that the supplier may make a loss on the investment (this is the hold-up problem, which occurs when either party asymmetrically incurs substantial costs or benefits before being paid for or paying for them). In this kind of a situation, the most efficient way to overcome the continual conflict of interest between the two agents (or coalitions of agents) may be the removal of one of them from the equation by takeover or merger. Asset specificity can also apply to some extent to both physical and human capital, so that the hold-up problem can also occur with labour (e.g. labour can threaten a strike, because of the lack of good alternative human capital; but equally the firm can threaten to fire).

Probably the best constraint on such opportunism is reputation (rather than the law, because of the difficulty of negotiating, writing and enforcement of contracts). If a reputation for opportunism significantly damages an agent's dealings in the future, this alters the incentives to be opportunistic.[18]

Williamson sees the limit on the size of the firm as being given partly by costs of delegation (as a firm's size increase its hierarchical bureaucracy does too), and the large firm's increasing inability to replicate the high-powered incentives of the residual income of an owner-entrepreneur. This is partly because it is in the nature of a large firm that its existence is more secure and less dependent on the actions of any one individual (increasing the incentives to shirk), and because intervention rights from the centre characteristic of a firm tend to be accompanied by some form of income insurance to compensate for the lesser responsibility, thereby diluting incentives. Milgrom and Roberts (1990) explain the increased cost of management as due to the incentives of employees to provide false information beneficial to themselves, resulting in costs to managers of filtering information, and often the making of decisions without full information. This grows worse with firm size and more layers in the hierarchy. Empirical analyses of transaction costs have attempted to measure and operationalize transaction costs.[19][20] Research that attempts to measure transaction costs is the most critical limit to efforts to potential falsification and validation of transaction cost economics.

Firm economies

The theory of the firm considers what bounds the size and output variety of firms. This includes how firms may be able to combine labour and capital so as to lower the average cost of output, either from increasing, decreasing, or constant returns to scale for one product line or from economies of scope for more than one product line.[9][21][22]

Other models

Efficiency wage models like that of Shapiro and Stiglitz (1984) suggest wage rents as an addition to monitoring, since this gives employees an incentive not to shirk, given a certain probability of detection and the consequence of being fired. Williamson, Wachter and Harris (1975) suggest promotion incentives within the firm as an alternative to morale-damaging monitoring, where promotion is based on objectively measurable performance. (The difference between these two approaches may be that the former is applicable to a blue-collar environment, the latter to a white-collar one). Leibenstein (1966) sees a firm's norms or conventions, dependent on its history of management initiatives, labour relations and other factors, as determining the firm's "culture" of effort, thus affecting the firm's productivity and hence size.

George Akerlof (1982) develops a gift exchange model of reciprocity, in which employers offer wages unrelated to variations in output and above the market level, and workers have developed a concern for each other's welfare, such that all put in effort above the minimum required, but the more able workers are not rewarded for their extra productivity; again, size here depends not on rationality or efficiency but on social factors.[23] In sum, the limit to the firm's size is given where costs rise to the point where the market can undertake some transactions more efficiently than the firm.

Recently, Yochai Benkler further questioned the rigid distinction between firms and markets based on the increasing salience of “commons-based peer production” systems such as open source software (e.g., Linux), Wikipedia, Creative Commons, etc. He put forth this argument in The Wealth of Networks: How Social Production Transforms Markets and Freedom, which was released in 2006 under a Creative Commons share-alike license.[24]

Grossman–Hart–Moore theory

In modern contract theory, the “theory of the firm” is often identified with the “property rights approach” that was developed by Sanford J. Grossman, Oliver D. Hart, and John H. Moore.[25][26] The property rights approach to the theory of the firm is also known as the “Grossman–Hart–Moore theory”. In their seminal work, Grossman and Hart (1986), Hart and Moore (1990) and Hart (1995) developed the incomplete contracting paradigm.[27][28][29] They argue that if contracts cannot specify what is to be done given every possible contingency, then property rights (and hence firm boundaries) matter. Specifically, consider a seller of an intermediate good and a buyer. Should the seller own the physical assets that are necessary to produce the good (non-integration) or should the buyer be the owner (integration)? After relationship-specific investments have been made, the seller and the buyer bargain. When they are symmetrically informed, they will always agree to collaborate. Yet, the division of the ex post surplus depends on the parties’ disagreement payoffs (the payoffs they would get if no ex post agreement were reached), which in turn depend on the ownership structure. Thus, the ownership structure has an influence on the incentives to invest. A central insight of the theory is that the party with the more important investment decision should be the owner. Another prominent conclusion is that joint asset ownership is suboptimal if investments are in human capital.

The Grossman–Hart–Moore model has been successfully applied in many contexts, e.g. with regard to privatization.[30] Chiu (1998) and DeMeza and Lockwood (1998) have extended the model by considering different bargaining games that the parties may play ex post (which can explain ownership by the less important investor).[31][32] Oliver Williamson (2002) has criticized the Grossman–Hart–Moore model because it is focused on ex ante investment incentives, while it neglects ex post inefficiencies.[33] Schmitz (2006) has studied a variant of the Grossman–Hart–Moore model in which a party may have or acquire private information about its disagreement payoff, which can explain ex post inefficiencies and ownership by the less important investor.[34] Several variants of the Grossman–Hart–Moore model such as the one with private information can also explain joint ownership.[35]

See also

Notes

- Kantarelis, Demetri (2007). Theories of the Firm. Geneve: Inderscience. ISBN 978-0-907776-34-5. Description & review.

• Spulber, Daniel F. (2009). The Theory of the Firm, Cambridge. Description, front matter, and "Introduction" excerpt. - Ahmad, Imtiaz; Mahmood, Zafar (2020-04-02). "Firms' heterogeneity and margins of trade under uncertainty". The Journal of International Trade & Economic Development. 29 (3): 272–288. doi:10.1080/09638199.2019.1660396. ISSN 0963-8199.

- Thomas N. Hubbard (2008). "firm boundaries (empirical studies)," The New Palgrave Dictionary of Economics, 2nd Edition. Abstract.

• Barak D. Richman and Jeffrey Mache (2008). "Transaction Cost Economics: An Assessment of Empirical Research in the Social Sciences," Business and Politics, 10(1), pp. 1-63. Abstract. [ PDF. - Coase, Ronald H. (1937). "The Nature of the Firm". Economica. 4 (16): 386–405. doi:10.1111/j.1468-0335.1937.tb00002.x.

- Holmström, Bengt, and John Roberts (1998). "The Boundaries of the Firm Revisited," Journal of Economic Perspectives, 12(4), pp. 73–94 (close Pages tab).Jean Tirole (1988). The Theory of Industrial Organization. "The Theory of the Firm", pp. 15–60. MIT Press.

• Luigi Zingales (2008). "corporate governance," The New Palgrave Dictionary of Economics, 2nd Edition. Abstract.

• Oliver E. Williamson (2002). "The Theory of the Firm as Governance Structure: From Choice to Contract," Journal of Economic Perspectives, 16(3), pp. 171-195.

• _____ (2009). "Transaction Cost Economics: The Natural Progression," Nobel lecture. Reprinted in (2010) American Economic Review, 100(3), pp. 673–90. - Hart, Oliver and John Moore (1990). "Property Rights and the Nature of the Firm," Journal of Political Economy, 98(6), pp. 1119-1158.

- Berle, Adolph A.; Gardiner C. Means (1933). The Modern Corporation and Private Property. New York: Macmillan. ISBN 978-0-88738-887-3.

- Hall, R.; Charles J. Hitch (1939). "Price Theory and Business Behaviour". Oxford Economic Papers. 2 (1): 12–45. doi:10.1093/oxepap/os-2.1.12. JSTOR 2663449.

- Archibald, G.C. (1987 [2008]). "firm, theory of the," The New Palgrave: A Dictionary of Economics, v. 2, p. 357.

- Ronald H. Coase (1988). "The Nature of the Firm: Influence", Journal of Law, Economics, & Organization, 4(1), p p. 33-47. Reprinted in The Nature of the Firm: Origins, Evolution, and Development (1993), Oliver E. Williamson and S, G. Winter, ed., pp. 61–74.

- Putterman, Louis (1996). The Economic Nature of the Firm. Cambridge: Cambridge University Press. ISBN 978-0-521-47092-6.

- Richardson, George Barclay (1972). "The Organisation of Industry". The Economic Journal. 82 (327): 883–896. doi:10.2307/2230256. JSTOR 2230256.

- Jensen, Michael C.; Meckling, William H. (1976). "Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure". Journal of Financial Economics. 3 (4): 305–360. doi:10.1016/0304-405x(76)90026-x. SSRN 94043.

- Spence, Michael A.; Zeckhauser, Richard (1971). "Insurance, Information, and Individual Action". American Economic Review. 61 (2): 380–387.

- Cyert, Richard; March, James (1963). Behavioral Theory of the Firm. Oxford: Blackwell. ISBN 978-0-631-17451-6.

- Alchian, Armen A.; Demsetz, Harold (1972). "Production, Information Costs, and Economic Organization". The American Economic Review. 62 (5): 777–795. JSTOR 1815199.

- Williamson, Oliver E. (1975). Markets and Hierarchies: Analysis and Antitrust Implications. New York: The Free Press.

- Oliar, Dotan; Sprigman, Christopher Jon (2008). "There's No Free Laugh (Anymore): The Emergence of Intellectual Property Norms and the Transformation of Stand-Up Comedy" (PDF). Virginia Law Review. 94 (8): 1787–1867.

- Barak D. Richman and Jeffrey Mache (2008). "Transaction Cost Economics: An Assessment of Empirical Research in the Social Sciences," Business and Politics, 10(1), pp. 1-63. Abstract. PDF.

- Special Issue of Journal of Retailing in Honor of The Sveriges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel 2009 to Oliver E. Williamson, 86(3), pp. 209-290, article-preview links (2010). Edited by Arne Nygaard and Robert Dahlstrom.

- John C. Panzar and Robert D. Willig (1981). "Economies of Scope," American Economic Review, 71(2), p p. 268–272.

- Jean Tirole (1988). The Theory of Industrial Organization. "The Theory of the Firm," pp. 18–20. MIT Press.

- Hans, V. Basil (December 2016). "Roles and Responsibilities of Managerial Economists: Empowering Business through Methodology and Strategy". 10. 2: 34.

- Benkler, Yochai (2006). The Wealth of Networks: How Social Production Transforms Markets. New Haven: Yale University Press.

- Bolton, Patrick; Dewatripont, Matthias (2005). Contract theory. MIT Press.

- Hart, Oliver (2011). "Thinking about the Firm: A Review of Daniel Spulber's The Theory of the Firm". Journal of Economic Literature. 49 (1): 101–113. doi:10.1257/jel.49.1.101. ISSN 0022-0515.

- Grossman, Sanford J.; Hart, Oliver D. (1986). "The Costs and Benefits of Ownership: A Theory of Vertical and Lateral Integration" (PDF). Journal of Political Economy. 94 (4): 691–719. doi:10.1086/261404. hdl:1721.1/63378. ISSN 0022-3808.

- Hart, Oliver; Moore, John (1990). "Property Rights and the Nature of the Firm". Journal of Political Economy. 98 (6): 1119–1158. CiteSeerX 10.1.1.472.9089. doi:10.1086/261729. ISSN 0022-3808.

- Hart, Oliver (1995). Firms, contracts, and financial structure. Oxford University Press.

- Hart, Oliver; Shleifer, Andrei; Vishny, Robert W. (1997). "The Proper Scope of Government: Theory and an Application to Prisons". The Quarterly Journal of Economics. 112 (4): 1127–1161. doi:10.1162/003355300555448. ISSN 0033-5533.

- Chiu, Y. Stephen (1998). "Noncooperative Bargaining, Hostages, and Optimal Asset Ownership". American Economic Review. 88: 882–901.

- Meza, David de; Lockwood, Ben (1998). "Does Asset Ownership Always Motivate Managers? Outside Options and the Property Rights Theory of the Firm". The Quarterly Journal of Economics. 113 (2): 361–386. doi:10.1162/003355398555621. ISSN 0033-5533.

- Williamson, Oliver E (2002). "The Theory of the Firm as Governance Structure: From Choice to Contract". Journal of Economic Perspectives. 16 (3): 171–195. CiteSeerX 10.1.1.196.6573. doi:10.1257/089533002760278776. ISSN 0895-3309.

- Schmitz, Patrick W (2006). "Information Gathering, Transaction Costs, and the Property Rights Approach". American Economic Review. 96 (1): 422–434. doi:10.1257/000282806776157722. ISSN 0002-8282.

- Gattai, Valeria; Natale, Piergiovanna (2015). "A New Cinderella Story: Joint Ventures and the Property Rights Theory of the Firm". Journal of Economic Surveys. 31: 281–302. doi:10.1111/joes.12135. ISSN 1467-6419.

References

- Crew, Michael A. (1975). Theory of the Firm. New York: Longman. p. 182. ISBN 978-0-582-44042-5.

- Clarke, Roger; McGuinness, Tony (1987). The Economics of the Firm. Cambridge: Blackwell. ISBN 978-0-631-14075-7.

- Foss, Nicolai J., ed. (2000). The Theory of the Firm: Critical Perspectives on Business and Management. Taylor and Francis. v. I–IV. Chapter preview links, including Bengt Holmström and Jean Tirole, "The Theory of the Firm," v. I, pp. 148–222 from Handbook of Industrial Organization (1989), R. Schmalensee and R. W. Willig, ed., v. 1, ch. 2, p p. 61–133.

- Hart, Oliver. Firms, Contracts, and Financial Structure. New York: Oxford University Press.

- Robé, Jean-Philippe, "The Legal Structure of the Firm", Accounting, Economics, and Law, Vol. 1, Iss. 1, Article 5, 2011.

Further reading

| Wikiquote has quotations related to: Theory of the firm |

- Kroszner, Randall S.; Putterman, Louis, eds. (2009). The Economic Nature of the Firm: A Reader (3rd ed.) Cambridge University Press.