Market failure

In neoclassical economics, market failure is a situation in which the allocation of goods and services by a free market is not Pareto efficient, often leading to a net loss of economic value. Market failures can be viewed as scenarios where individuals' pursuit of pure self-interest leads to results that are not efficient– that can be improved upon from the societal point of view.[1][2] The first known use of the term by economists was in 1958,[3] but the concept has been traced back to the Victorian philosopher Henry Sidgwick.[4] Market failures are often associated with public goods,[5] time-inconsistent preferences,[6] information asymmetries,[7] non-competitive markets, principal–agent problems, or externalities.[8]

The existence of a market failure is often the reason that self-regulatory organizations, governments or supra-national institutions intervene in a particular market.[9][10] Economists, especially microeconomists, are often concerned with the causes of market failure and possible means of correction.[11] Such analysis plays an important role in many types of public policy decisions and studies.

However, government policy interventions, such as taxes, subsidies, wage and price controls, and regulations, may also lead to an inefficient allocation of resources, sometimes called government failure.[12] Given the tension between the economic costs caused by market failure and costs caused by "government failure", policymakers attempting to maximize economic value are sometimes (but not always) faced with a choice between two inefficient outcomes, i.e. inefficient market outcomes with or without government interventions.

Most mainstream economists believe that there are circumstances (like building codes or endangered species) in which it is possible for government or other organizations to improve the inefficient market outcome. Several heterodox schools of thought disagree with this as a matter of ideology.[13]

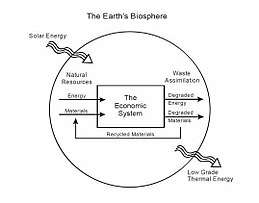

An ecological market failure exists when human activity in a market economy is exhausting critical non-renewable resources, disrupting fragile ecosystems, or overloading biospheric waste absorption capacities. In none of these cases does the criterion of Pareto efficiency obtain.[14]

Categories

Different economists have different views about what events are the sources of market failure. Mainstream economic analysis widely accepts that a market failure (relative to Pareto efficiency) can occur for three main reasons: if the market is "monopolised" or a small group of businesses hold significant market power, if production of the good or service results in an externality (external costs or benefits), or if the good or service is a "public good".[15]

Nature of the market

Agents in a market can gain market power, allowing them to block other mutually beneficial gains from trade from occurring. This can lead to inefficiency due to imperfect competition, which can take many different forms, such as monopolies,[16] monopsonies, or monopolistic competition, if the agent does not implement perfect price discrimination.

It is then a further question about what circumstances allow a monopoly to arise. In some cases, monopolies can maintain themselves where there are "barriers to entry" that prevent other companies from effectively entering and competing in an industry or market. Or there could exist significant first-mover advantages in the market that make it difficult for other firms to compete. Moreover, monopoly can be a result of geographical conditions created by huge distances or isolated locations. This leads to a situation where there are only few communities scattered across a vast territory with only one supplier. Australia is an example that meets this description.[17] A natural monopoly is a firm whose per-unit cost decreases as it increases output; in this situation it is most efficient (from a cost perspective) to have only a single producer of a good. Natural monopolies display so-called increasing returns to scale. It means that at all possible outputs marginal cost needs to be below average cost if average cost is declining. One of the reasons is the existence of fixed costs, which must be paid without considering the amount of output, what results in a state where costs are evenly divided over more units leading to the reduction of cost per unit.[18]

Nature of the goods

Non-excludability

Some markets can fail due to the nature of the goods being exchanged. For instance, some goods can display the attributes of public goods[16] or common goods, wherein sellers are unable to exclude non-buyers from using a product, as in the development of inventions that may spread freely once revealed, such as developing a new method of harvesting. This can cause underinvestment because developers cannot capture enough of the benefits from success to make the development effort worthwhile. This can also lead to resource depletion in the case of common-pool resources, where, because use of the resource is rival but non-excludable, there is no incentive for users to conserve the resource. An example of this is a lake with a natural supply of fish: if people catch the fish faster than the fish can reproduce, then the fish population will dwindle until there are no fish left for future generations.

Externalities

A good or service could also have significant externalities,[8][16] where gains or losses associated with the product, production or consumption of a product, differ from the private cost. These externalities can be innate to the methods of production or other conditions important to the market.[2]

Traffic congestion is an example of market failure that incorporates both non-excludability and externality. Public roads are common resources that are available for the entire population's use (non-excludable), and act as a complement to cars (the more roads there are, the more useful cars become). Because there is very low cost but high benefit to individual drivers in using the roads, the roads become congested, decreasing their usefulness to society. Furthermore, driving can impose hidden costs on society through pollution (externality). Solutions for this include public transportation, congestion pricing, tolls, and other ways of making the driver include the social cost in the decision to drive.[2]

Perhaps the best example of the inefficiency associated with common/public goods and externalities is the environmental harm caused by pollution and overexploitation of natural resources.[2]

Nature of the exchange

Some markets can fail due to the nature of their exchange. Markets may have significant transaction costs, agency problems, or informational asymmetry.[2][16] Such incomplete markets may result in economic inefficiency but also a possibility of improving efficiency through market, legal, and regulatory remedies. From contract theory, decisions in transactions where one party has more or better information than the other is an asymmetry. This creates an imbalance of power in transactions which can sometimes cause the transactions to go awry. Examples of this problem are adverse selection and moral hazard. Most commonly, information asymmetries are studied in the context of principal–agent problems. George Akerlof, Michael Spence, and Joseph E. Stiglitz developed the idea and shared the 2001 Nobel Prize in Economics.[19]

Bounded rationality

In Models of Man, Herbert A. Simon points out that most people are only partly rational, and are emotional/irrational in the remaining part of their actions. In another work, he states "boundedly rational agents experience limits in formulating and solving complex problems and in processing (receiving, storing, retrieving, transmitting) information" (Williamson, p. 553, citing Simon). Simon describes a number of dimensions along which "classical" models of rationality can be made somewhat more realistic, while sticking within the vein of fairly rigorous formalization. These include:

- limiting what sorts of utility functions there might be.

- recognizing the costs of gathering and processing information.

- the possibility of having a "vector" or "multi-valued" utility function.

Simon suggests that economic agents employ the use of heuristics to make decisions rather than a strict rigid rule of optimization. They do this because of the complexity of the situation, and their inability to process and compute the expected utility of every alternative action. Deliberation costs might be high and there are often other, concurrent economic activities also requiring decisions.

Coase theorem

The Coase theorem, developed by Ronald Coase and labeled as such by George Stigler, states that private transactions are efficient as long as property rights exist, only a small number of parties are involved, and transactions costs are low. Additionally, this efficiency will take place regardless of who owns the property rights. This theory comes from a section of Coase's Nobel prize-winning work The Problem of Social Cost. While the assumptions of low transactions costs and a small number of parties involved may not always be applicable in real-world markets, Coase's work changed the long-held belief that the owner of property rights was a major determining factor in whether or not a market would fail.[20] The Coase theorem points out when one would expect the market to function properly even when there are externalities.

A market is an institution in which individuals or firms exchange not just commodities, but the rights to use them in particular ways for particular amounts of time. [...] Markets are institutions which organize the exchange of control of commodities, where the nature of the control is defined by the property rights attached to the commodities.[10]

As a result, agents' control over the uses of their commodities can be imperfect, because the system of rights which defines that control is incomplete. Typically, this falls into two generalized rights – excludability and transferability. Excludability deals with the ability of agents to control who uses their commodity, and for how long – and the related costs associated with doing so. Transferability reflects the right of agents to transfer the rights of use from one agent to another, for instance by selling or leasing a commodity, and the costs associated with doing so. If a given system of rights does not fully guarantee these at minimal (or no) cost, then the resulting distribution can be inefficient.[10] Considerations such as these form an important part of the work of institutional economics.[21] Nonetheless, views still differ on whether something displaying these attributes is meaningful without the information provided by the market price system.[22]

Business cycles

Macroeconomic business cycles are a part of the market. They are characterized by constant downswings and upswings which influence economic activity. Therefore, this situation requires some kind of government intervention.[17]

Interpretations and policy examples

The above causes represent the mainstream view of what market failures mean and of their importance in the economy. This analysis follows the lead of the neoclassical school, and relies on the notion of Pareto efficiency,[23] which can be in the "public interest", as well as in interests of stakeholders with equity.[11] This form of analysis has also been adopted by the Keynesian or new Keynesian schools in modern macroeconomics, applying it to Walrasian models of general equilibrium in order to deal with failures to attain full employment, or the non-adjustment of prices and wages.

Policies to prevent market failure are already commonly implemented in the economy. For example, to prevent information asymmetry, members of the New York Stock Exchange agree to abide by its rules in order to promote a fair and orderly market in the trading of listed securities. The members of the NYSE presumably believe that each member is individually better off if every member adheres to its rules – even if they have to forego money-making opportunities that would violate those rules.

A simple example of policies to address market power is government antitrust policies. As an additional example of externalities, municipal governments enforce building codes and license tradesmen to mitigate the incentive to use cheaper (but more dangerous) construction practices, ensuring that the total cost of new construction includes the (otherwise external) cost of preventing future tragedies. The voters who elect municipal officials presumably feel that they are individually better off if everyone complies with the local codes, even if those codes may increase the cost of construction in their communities.

CITES is an international treaty to protect the world's common interest in preserving endangered species – a classic "public good" – against the private interests of poachers, developers and other market participants who might otherwise reap monetary benefits without bearing the known and unknown costs that extinction could create. Even without knowing the true cost of extinction, the signatory countries believe that the societal costs far outweigh the possible private gains that they have agreed to forego.

Some remedies for market failure can resemble other market failures. For example, the issue of systematic underinvestment in research is addressed by the patent system that creates artificial monopolies for successful inventions.

Objections

Public choice

Economists such as Milton Friedman from the Chicago school and others from the Public Choice school, argue that market failure does not necessarily imply that the government should attempt to solve market failures, because the costs of government failure might be worse than those of the market failure it attempts to fix. This failure of government is seen as the result of the inherent problems of democracy and other forms of government perceived by this school and also of the power of special-interest groups (rent seekers) both in the private sector and in the government bureaucracy. Conditions that many would regard as negative are often seen as an effect of subversion of the free market by coercive government intervention. Beyond philosophical objections, a further issue is the practical difficulty that any single decision maker may face in trying to understand (and perhaps predict) the numerous interactions that occur between producers and consumers in any market.

Austrian

Some advocates of laissez-faire capitalism, including many economists of the Austrian School, argue that there is no such phenomenon as "market failure". Israel Kirzner states that, "Efficiency for a social system means the efficiency with which it permits its individual members to achieve their individual goals."[24] Inefficiency only arises when means are chosen by individuals that are inconsistent with their desired goals.[25] This definition of efficiency differs from that of Pareto efficiency, and forms the basis of the theoretical argument against the existence of market failures. However, providing that the conditions of the first welfare theorem are met, these two definitions agree, and give identical results. Austrians argue that the market tends to eliminate its inefficiencies through the process of entrepreneurship driven by the profit motive; something the government has great difficulty detecting, or correcting.[26]

Marxian

Objections also exist on more fundamental bases, such as Marxian analysis. Colloquial uses of the term "market failure" reflect the notion of a market "failing" to provide some desired attribute different from efficiency – for instance, high levels of inequality can be considered a "market failure", yet are not Pareto inefficient, and so would not be considered a market failure by mainstream economics.[2] In addition, many Marxian economists would argue that the system of private property rights is a fundamental problem in itself, and that resources should be allocated in another way entirely. This is different from concepts of "market failure" which focuses on specific situations – typically seen as "abnormal" – where markets have inefficient outcomes. Marxists, in contrast, would say that markets have inefficient and democratically unwanted outcomes – viewing market failure as an inherent feature of any capitalist economy – and typically omit it from discussion, preferring to ration finite goods not exclusively through a price mechanism, but based upon need as determined by society expressed through the community.

Ecological

| Part of a series on |

| Ecological economics |

|---|

Humanity's economic system viewed as a subsystem of the global environment |

|

Works

|

In ecological economics, the concept of externalities is considered a misnomer, since market agents are viewed as making their incomes and profits by systematically 'shifting' the social and ecological costs of their activities onto other agents, including future generations. Hence, externalities is a modus operandi of the market, not a failure: The market cannot exist without constantly 'failing'.

The fair and even allocation of non-renewable resources over time is a market failure issue of concern to ecological economics. This issue is also known as 'intergenerational fairness'. It is argued that the market mechanism fails when it comes to allocating the Earth's finite mineral stock fairly and evenly among present and future generations, as future generations are not, and cannot be, present on today's market.[27]:375 [28]:142f In effect, today's market prices do not, and cannot, reflect the preferences of the yet unborn.[29]:156–160 This is an instance of a market failure passed unrecognized by most mainstream economists, as the concept of Pareto efficiency is entirely static (timeless).[30]:181f Imposing government restrictions on the general level of activity in the economy may be the only way of bringing about a more fair and even intergenerational allocation of the mineral stock. Hence, Nicholas Georgescu-Roegen and Herman Daly, the two leading theorists in the field, have both called for the imposition of such restrictions: Georgescu-Roegen has proposed a minimal bioeconomic program, and Daly has proposed a comprehensive steady-state economy.[27]:374–79 [30] However, Georgescu-Roegen, Daly, and other economists in the field agree that on a finite Earth, geologic limits will inevitably strain most fairness in the longer run, regardless of any present government restrictions: Any rate of extraction and use of the finite stock of non-renewable mineral resources will diminish the remaining stock left over for future generations to use.[27]:366–69 [31]:369–71 [32]:165–67 [33]:270 [34]:37

Another ecological market failure is presented by the overutilisation of an otherwise renewable resource at a point in time, or within a short period of time. Such overutilisation usually occurs when the resource in question has poorly defined (or non-existing) property rights attached to it while too many market agents engage in activity simultaneously for the resource to be able to sustain it all. Examples range from over-fishing of fisheries and over-grazing of pastures to over-crowding of recreational areas in congested cities. This type of ecological market failure is generally known as the 'tragedy of the commons'. In this type of market failure, the principle of Pareto efficiency is violated the utmost, as all agents in the market are left worse off, while nobody are benefitting. It has been argued that the best way to remedy a 'tragedy of the commons'-type of ecological market failure is to establish enforceable property rights politically – only, this may be easier said than done.[14]:172f

The issue of anthropogenic global warming presents an overwhelming example of a 'tragedy of the commons'-type of ecological market failure: The Earth's atmosphere may be regarded as a 'global common' exhibiting poorly defined (non-existing) property rights, and the waste absorption capacity of the atmosphere with regard to carbon dioxide is presently being heavily overloaded by a large volume of emissions from the world economy.[35]:347f Historically, the fossil fuel dependence of the Industrial Revolution has unintentionally thrown mankind out of ecological equilibrium with the rest of the Earth's biosphere (including the atmosphere), and the market has failed to correct the situation ever since. Quite the opposite: The unrestricted market has been exacerbating this global state of ecological dis-equilibrium, and is expected to continue doing so well into the foreseeable future.[36]:95–101 This particular market failure may be remedied to some extent at the political level by the establishment of an international (or regional) cap and trade property rights system, where carbon dioxide emission permits are bought and sold among market agents.[14]:433–35

The term 'uneconomic growth' describes a pervasive ecological market failure: The ecological costs of further economic growth in a so-called 'full-world economy' like the present world economy may exceed the immediate social benefits derived from this growth.[14]:16–21

Chang's criticism

Chang states that "it is (implicitly) assumed the state knows everything and can do everything.”[17] Thus, this implies several assumptions about government in relation to market failures. There are three main statements. First of all, government representatives are able to evaluate the scope of market failures and to what extent it differs from efficient outcome. Secondly, having acquired the aforementioned knowledge they have capacity to re-establish market efficiency. Lastly, there has arisen an idea according to which decisions of policy-makers are not influenced by self-interest, but they are driven by altruism.

Lipsey and Lancaster criticism

They came up with the theory of the so-called the “second best.” They refuse Chang's theory and state that is it not possible to restore Pareto optimality even if policy makers possess the sufficient knowledge, intervene efficiently and altruism serves as stimulus for their decisions. On the other hand, the “second best” theory holds that when market failure occurs in one branch of the economy, it should be feasible to increase social welfare in another branch of the economy by violating Pareto efficiency instead of restoring Pareto efficiency by government intervention.[37]

Zerbe and McCurdy

Zerbe and McCurdy connected criticism of market failure paradigm to transaction costs. Market failure paradigm is defined as follows:

"A fundamental problem with the concept of market failure, as economists occasionally recognize, is that it describes a situation that exists everywhere.”

Transaction costs are part of each market exchange, although the price of transaction costs is not usually determined. They occur everywhere and are unpriced. Consequently, market failures and externalities can arise in the economy every time transaction costs arise. There is no place for government intervention. Instead, government should focus on the elimination of both transaction costs and costs of provision.[38]

See also

- Contract failure

- Distortion (economics)

- Government failure

- Highest and best use

- Public economics

- Social cost

- Tyranny of small decisions

References

- John O. Ledyard (2008). "market failure," The New Palgrave Dictionary of Economics, 2nd Ed. Abstract.

- Paul Krugman and Robin Wells (2006). Economics, New York, Worth Publishers.

- Francis M. Bator (1958). "The Anatomy of Market Failure," Quarterly Journal of Economics, 72(3) pp. 351–79 (press +).

- Steven G. Medema (2007). "The Hesitant Hand: Mill, Sidgwick, and the Evolution of the Theory of Market Failure," History of Political Economy, 39(3), p p. 331–58. 2004 Online Working Paper.

- Joseph E. Stiglitz (1989). "Markets, Market Failures, and Development," American Economic Review, 79(2), pp. 197–203.

- •Ignacio Palacios-Huerta (2003) "Time-inconsistent preferences in Adam Smith and David Hume," History of Political Economy, 35(2), pp. 241–68

- • Charles Wilson (2008). "adverse selection," The New Palgrave Dictionary of Economics 2nd Edition. Abstract.

• Joseph E. Stiglitz (1998). "The Private Uses of Public Interests: Incentives and Institutions," Journal of Economic Perspectives, 12(2), pp. 3–22. - J.J. Laffont (2008). "externalities," The New Palgrave Dictionary of Economics, 2nd Ed. Abstract.

- Kenneth J. Arrow (1969). "The Organization of Economic Activity: Issues Pertinent to the Choice of Market versus Non-market Allocations," in Analysis and Evaluation of Public Expenditures: The PPP System, Washington, D.C., Joint Economic Committee of Congress. PDF reprint as pp. 1–16 (press +).

- Gravelle, Hugh; Ray Rees (2004). Microeconomics. Essex, England: Prentice Hall, Financial Times. pp. 314–46.

- Mankiw, Gregory; Ronald Kneebone; Kenneth McKenzie; Nicholas Row (2002). Principles of Microeconomics: Second Canadian Edition. United States: Thomson-Nelson. pp. 157–58.

- Weimer, David; Aidan R. Vining (2004). Policy Analysis: Concepts and Practice. Prentice Hall.

- Mankiw, N. Gregory (2009). Brief Principles of Macroeconomics. South-Western Cengage Learning. pp. 10–12.

- Daly, Herman E.; Farley, Joshua (2011). Ecological Economics. Principles and Applications (PDF contains full textbook) (2nd ed.). Washington: Island Press. ISBN 9781597266819.

- Krugman, Paul; Robin Wells; Anthony Myatt (2006). Microeconomics: Canadian Edition. Worth Publishers. pp. 160–62.

- DeMartino, George (2000). Global Economy, Global Justice. Routledge. p. 70. ISBN 0-415-22401-2.

- Brian., Dollery (2001). The political economy of local government. Wallis, Joe (Joe L.). Northampton, MA: Edward Elgar Pub. ISBN 1840644516. OCLC 46462759.

- "Natural monopolies exist when one firm dominates an industry". www.economicsonline.co.uk. Retrieved 2018-04-24.

- Huffman, Max (December 2010). "Neo-Behavioralism?": 9. SSRN 1730365. Cite journal requires

|journal=(help) - Michael Parkin (2008). "Microeconomics," 9th Ed. p. 379. University of Western Ontario.

- Bowles, Samuel (2004). Microeconomics: Behavior, Institutions, and Evolution. United States: Russel Sage Foundation.

- Machan, R. Tibor, Some Skeptical Reflections on Research and Development, Hoover Press

- MacKenzie, D.W. (2002-08-26). "The Market Failure Myth". Ludwig von Mises Institute. Retrieved 2008-11-25.

- Israel Kirzner (1963). Market Theory and the Price System. Princeton. N.J.: D. Van Nostrand Company. p. 35.

- Roy E. Cordato (1980). "The Austrian Theory of Efficiency and the Role of Government" (PDF). The Journal of Libertarian Studies. 4 (4): 393–403 [396].

- Roy E. Cordato (1980). "The Austrian Theory of Efficiency and the Role of Government" (PDF). The Journal of Libertarian Studies. 4 (4): 393–403.

- Georgescu-Roegen, Nicholas (1975). "Energy and Economic Myths" (PDF). Southern Economic Journal. Tennessee: Southern Economic Association. 41 (3): 347–81. doi:10.2307/1056148. JSTOR 1056148.

- Perez-Carmona, Alexander (2013). "Growth: A Discussion of the Margins of Economic and Ecological Thought". In Meuleman, Louis (ed.). Transgovernance. Advancing Sustainability Governance. Heidelberg: Springer. pp. 83–161. doi:10.1007/978-3-642-28009-2_3. ISBN 9783642280085 – via SlideShare.

- Martínez-Alier, Juan (1987). Ecological Economics: Energy, Environment and Society. Oxford: Basil Blackwell. ISBN 0631171460.

- Daly, Herman E. (1992). Steady-state economics (2nd ed.). London: Earthscan Publications.

- Daly, Herman E., ed. (1980). Economics, Ecology, Ethics. Essays Towards a Steady-State Economy (PDF contains only the introductory chapter of the book) (2nd ed.). San Francisco: W.H. Freeman and Company. ISBN 0716711788.

- Boulding, Kenneth E. (1981). Evolutionary Economics. Beverly Hills: Sage Publications. ISBN 0803916485.

- Bonaiuti, Mauro (2008). "Searching for a Shared Imaginary – A Systemic Approach to Degrowth and Politics" (PDF contains all conference proceedings). In Flipo, Fabrice; Schneider, François (eds.). Proceedings of the First International Conference on Economic De-Growth for Ecological Sustainability and Social Equity. Paris.

- Valero Capilla, Antonio; Valero Delgado, Alicia (2014). Thanatia: The Destiny of the Earth's Mineral Resources. A Thermodynamic Cradle-to-Cradle Assessment (PDF contains only the introductory chapter of the book). Singapore: World Scientific Publishing. Bibcode:2014tdem.book.....C. doi:10.1142/7323. ISBN 9789814273930.

- McConnell, Campbell R.; et al. (2009). Economics. Principles, Problems and Policies (PDF) (18th ed.). New York: McGraw-Hill. ISBN 9780073375694. Archived from the original (PDF contains full textbook) on 2016-10-06. Retrieved 2016-04-15.

- Schmitz, John E.J. (2007). The Second Law of Life: Energy, Technology, and the Future of Earth As We Know It (Link to the author's science blog, based on his textbook). Norwich: William Andrew Publishing. ISBN 978-0815515371.

- Lipsey, Richard (2007). "Reflections on the General Theory of Second Best at its Golden Jubilee". International Tax and Public Finance. 14 (4): 349–364. doi:10.1007/s10797-007-9036-x.

- McCurdy, Howard E.; Zerbe Jr., Richard O. (1999). "The Failure of Market Failure". Journal of Policy Analysis and Management. 18 (4): 558–578. doi:10.1002/(SICI)1520-6688(199923)18:4<558::AID-PAM2>3.0.CO;2-U.

External links

- Market Failures – in Price Theory, an intermediate text by David D. Friedman

| Authority control |

|

|---|