Private foundation

A private foundation is a charitable organization that, while serving a good cause, might or might not qualify as a public charity by government standards.[1] The Bill & Melinda Gates Foundation is the largest private foundation in the U.S. with over $38 billion in assets.[2] Most private foundations are much smaller. Approximately two-thirds of the more than 84,000 foundations which file with the IRS, in 2008, have less than $1 million in assets, and 93% have less than $10 million in assets.[2] In aggregate, private foundations in the U.S. control over $628 billion in assets[2] and made more than $44 billion in charitable contributions in 2007.[3]

Unlike a charitable foundation, a private foundation does not generally solicit funds from the public or have the legal requirements and reporting responsibilities of a registered, non-profit or charitable foundation. Not all foundations engage in philanthropy: some private foundations are used for estate planning purposes.

Description

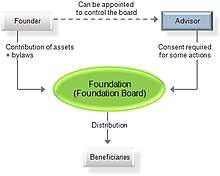

One of the characteristics of the legal entities existing under the status of "Foundations" is a wide diversity of structures and purposes. Nevertheless, there are some common structural elements that are the first observed under legal scrutiny or classification.

- Legal requirements followed for establishment

- Purpose of the foundation

- Economic activity

- Supervision and management provisions

- Accountability and auditing provisions

- Provisions for the amendment of the statutes or articles of incorporation

- Provisions for the dissolution of the entity

- Tax status of corporate and private donors

- Tax status of the foundation

Some of the above must be, in most jurisdictions, expressed in the document of establishment. Others may be provided by the supervising authority at each particular jurisdiction.

Common law

The following foundations are set up under common law legal systems:

The Bahamas

Foundations were first introduced in The Bahamas in December 2004 following the Foundations Act.[4]

United States

A private foundation, in the United States, is a charitable organization described in the Internal Revenue Code by section 509.[5] A private foundation is necessarily a 501(c)(3) exempt organization (or a former such entity). It is defined by a negative definition: by what it is not. A private foundation is not a public charity, as described in section 170(b)(1)(A) (i) through (vi). Neither is it a section 509(a)(2) organization, nor a supporting organization.[6] Private foundations are subject to 2% excise taxes found in section 4940 through 4945 of the internal revenue code.[7] Once a charity becomes a private foundation, it retains that status unless it follows the difficult termination rules of section 507.

Every organization that qualifies for tax exemption as an organization described in section 501(c)(3) is a private foundation unless it falls into one of the categories specifically excluded from the definition of that term (referred to in section 509(a)). In addition, certain nonexempt charitable trusts are also treated as private foundations. Organizations that fall into the excluded categories are institutions such as hospitals or universities and those that generally have broad public support or actively function in a supporting relationship to such organizations.[8]

In the United States, there are several restrictions and requirements on private foundations, including:

- restrictions on self-dealing between private foundations and their substantial contributors and other disqualified persons;

- requirements that the foundation annually distribute income for charitable purposes;

- limits on their holdings in private businesses;

- provisions that investments must not jeopardize the carrying out of exempt purposes; and

- provisions to assure that expenditures further exempt purposes. Violations of these provisions give rise to taxes and penalties against the private foundation and, in some cases, its managers, its substantial contributors, and certain related persons.[8]

Violations of these provisions give rise to taxes and penalties against the private foundation and, in some cases, its managers, its substantial contributors, and certain related persons.[8]

Civil law

The following foundations are set up under civil law legal systems:

Austria

The Austrian Private Foundation (Privatstiftung) was last reformed under the Private Foundation Act in September 1993. The Austrian private foundation is considered a legal person having beneficiaries rather than shareholders or proprietors and may be established for any purpose.[9] There are three levels of taxation related to Austrian private foundations: taxation of asset transfers, ongoing taxation of the private foundation's income; and taxation of distributions from the private foundation to beneficiaries.[10]

Canada

In Canada the Canada Revenue Agency is a branch of the Canadian government which regulates all foundations. Under Canadian law, since 1967, a private foundation is controlled by a single donor or family through a board that is made up of a majority (more than 50%) of directors at non-arm’s length. It is a legally registered charity with the Canada Revenue Agency. A public foundation is governed by a board that is made up of a majority of directors at arm’s length. A private foundation is not allowed to engage in any business activity, but it can operate its own charitable program.[11]

Canada Revenue Agency designates the application as a “charitable organization,” a “public foundation,” or a “private foundation,” depending on its structure, its source of funding and its operation. The Income Tax Act requirements are different, depending on the type of charity.(Canada Income Tax Act, R.S.C. 1985 (5th supp.) c. 1, para. 149.1(4)(a))[12]

Liechtenstein

The Liechtenstein Family Foundation (Stiftung) was first introduced in 1926 and updated by the Act Reforming the Persons and Companies Act in 2008 which included a new Act on Foundations.[13] They are allowed to pursue non-commercial and/or private benefit purposes. Private Benefit Family Foundation pays no taxes.[14]

Netherlands

A foundation in the Netherlands (Stichting) is a legal person created through a legal act. This act is usually either a notarised deed (or a will) that contains the articles of the foundation which must include the first appointed board.[16]

Netherlands Antilles

Foundation legislation was last reformed in 1998, giving rise to the Netherlands Antilles Private Foundation (Stichting Particulier Fonds).[17]

Panama

The Panama Private Interest Foundation was introduced following the Law 25, June 12, 1995. [19]

Saint Kitts

The Saint Kitts Foundation was introduced following the Foundation Act of 2003.[20]

Seychelles

The Seychelles Foundation was introduced following the Foundation Act of 2009.[21]

Sweden

A private foundation in Sweden (Stiftelse) is formed by a letter of donation from a founder donating funds or assets to be administered for a specific purpose. A private foundation may have diverse purposes, including collective, familiar, or the purpose of passive administration of funds. Normally, the supervision of a private foundation is done by the county government where the foundation has its domicile, however, large foundations must be registered by the County Administrative Board (CAB), which must also supervise the administration of the foundation. The main legal instruments governing private foundations in Sweden are those that regulate foundations in general: the Foundation Act (1994:1220) and the Regulation for Foundations (1995:1280).[22]

See also

- Charitable organization

- Foundation (nonprofit organization)

- Institute

- Stichting

- Waqf

References

- Kagen, Julia. "Private Foundation". Investopedia. Retrieved 2018-12-19.

- National Center for Charitable Statistics

- "Foundation Center". (In 2019 the Foundation Center and "GuideStar". formed "Candid".)

- https://web.archive.org/web/20080514034256/http://www.bfsb-bahamas.com/foundations/index.html

- 26 U.S.C. § 509

- "IRS webpage, which defines private foundations". irs.gov. Archived from the original on 4 August 2012. Retrieved 4 May 2018.

- "Excise taxes on private foundations". irs.gov. Archived from the original on 2 July 2012. Retrieved 4 May 2018.

- "Private Foundations | Internal Revenue Service". www.irs.gov. Retrieved 2018-12-19.

- "Foundations in Austria and features of foundations | How and why Austrian private foundations organized by legal framework". www.slogold.net. Retrieved 2019-04-05.

- Pfister, Wolf Theiss-Cynthia; Stadler, Eva. "Austrian Private Client Taxation 101: Taxation of Austrian Private Foundations | Lexology". www.lexology.com. Retrieved 2020-06-30.

- Agency, Canada Revenue (2002-12-03). "Charities and giving glossary". aem. Retrieved 2019-04-05.

- "Canadian Foundation Facts". Philanthropic Foundations Canada. Retrieved 2019-04-05.

- Palmer, Edith (2008-09-08). "Liechtenstein: Reformed Law of Private Foundations | Global Legal Monitor". www.loc.gov. Retrieved 2019-04-05.

- "Liechtenstein Foundation Formation & Comparison to a Trust". Offshore Company. Retrieved 2020-06-30.

- Appleby. "Guide to Foundations in Mauritius" (PDF).

- "Archived copy". Archived from the original on 2015-04-25. Retrieved 2015-03-03.CS1 maint: archived copy as title (link)

- "Private Foundation - Dutch Caribbean Legal Portal". www.dutchcaribbeanlegalportal.com. Retrieved 2019-04-05.

- "Easy To Form Nevis Multiform Foundation, Offshore Tax Haven Of Nevis". www.nevisfoundation.com. Retrieved 2019-04-05.

- Asamblea Nacional de Panamá (12 Jun 1995). "Ley 25 de 1995 de Panama por la cual se regulan fundaciones de interes privadọ, promulgada en la Gaceta Oficial 22804 de 14 de junio de 1995" (PDF). asamblea.gob.pa. Retrieved 21 May 2018.

- "Use a St Kitts Foundation to Manage Assets". Discover-StKitts-Nevis-Beaches.com. Retrieved 2019-04-05.

- "Foundations Act | Seychelles Legal Information Institute". seylii.org. Retrieved 2019-04-05.

- "Practical Law UK Signon". signon.thomsonreuters.com. Retrieved 2019-04-05.