Gold standard

A gold standard is a monetary system in which the standard economic unit of account is based on a fixed quantity of gold. The gold standard was widely used in the 19th and early part of the 20th century. Most nations abandoned the gold standard as the basis of their monetary systems at some point in the 20th century, although many still hold substantial gold reserves.[1][2]

History

The gold standard was originally implemented as a gold specie standard, by the circulation of gold coins. The monetary unit is associated with the value of circulating gold coins, or the monetary unit has the value of a certain circulating gold coin, but other coins may be made of less valuable metal. With the invention and spread in use of paper money, gold coins were eventually supplanted by banknotes, creating the gold bullion standard, a system in which gold coins do not circulate, but the authorities agree to sell gold bullion on demand at a fixed price in exchange for the circulating currency.

Lastly, countries may implement a gold exchange standard, where the government guarantees a fixed exchange rate, not to a specified amount of gold, but rather to the currency of another country that uses a gold standard. This creates a de facto gold standard, where the value of the means of exchange has a fixed external value in terms of gold that is independent of the inherent value of the means of exchange itself.

Origins

The gold specie standard arose from the widespread acceptance of gold as currency.[3] Various commodities have been used as money; typically, the one that loses the least value over time becomes the accepted form.[4]

The use of gold as money began thousands of years ago in Asia Minor.[5]

During the early and high Middle Ages, the Byzantine gold solidus, commonly known as the bezant, was used widely throughout Europe and the Mediterranean. However, as the Byzantine Empire's economic influence declined, so too did the use of the bezant.[6] In its place, European territories chose silver as their currency over gold, leading to the development of silver standards.[7]

Silver pennies based on the Roman denarius became the staple coin of Mercia in Great Britain around the time of King Offa, circa 757–796 CE.[8] Similar coins, including Italian denari, French deniers, and Spanish dineros, circulated in Europe. Spanish explorers discovered silver deposits in Mexico in 1522 and at Potosí in Bolivia in 1545.[9] International trade came to depend on coins such as the Spanish dollar, the Maria Theresa thaler, and, later, the United States trade dollar.

In modern times, the British West Indies was one of the first regions to adopt a gold specie standard. Following Queen Anne's proclamation of 1704, the British West Indies gold standard was a de facto gold standard based on the Spanish gold doubloon. In 1717, Sir Isaac Newton, the master of the Royal Mint, established a new mint ratio between silver and gold that had the effect of driving silver out of circulation and putting Britain on a gold standard.[10]

A formal gold specie standard was first established in 1821, when Britain adopted it following the introduction of the gold sovereign by the new Royal Mint at Tower Hill in 1816. The Province of Canada in 1854, Newfoundland in 1865, and the United States and Germany (de jure) in 1873 adopted gold. The United States used the eagle as its unit, Germany introduced the new gold mark, while Canada adopted a dual system based on both the American gold eagle and the British gold sovereign.[11]

Australia and New Zealand adopted the British gold standard, as did the British West Indies, while Newfoundland was the only British Empire territory to introduce its own gold coin.[12] Royal Mint branches were established in Sydney, Melbourne, and Perth for the purpose of minting gold sovereigns from Australia's rich gold deposits.

The gold specie standard came to an end in the United Kingdom and the rest of the British Empire with the outbreak of World War I.[13]

Silver

From 1750 to 1870, wars within Europe as well as an ongoing trade deficit with China (which sold to Europe but had little use for European goods) drained silver from the economies of Western Europe and the United States. Coins were struck in smaller and smaller numbers, and there was a proliferation of bank and stock notes used as money.

United Kingdom

In the 1790s, the United Kingdom suffered a silver shortage. It ceased to mint larger silver coins and instead issued "token" silver coins and overstruck foreign coins. With the end of the Napoleonic Wars, the Bank of England began the massive recoinage programme that created standard gold sovereigns, circulating crowns, half-crowns and eventually copper farthings in 1821. The recoinage of silver after a long drought produced a burst of coins. The United Kingdom struck nearly 40 million shillings between 1816 and 1820, 17 million half crowns and 1.3 million silver crowns.

The 1819 Act for the Resumption of Cash Payments set 1823 as the date for resumption of convertibility, which was reached by 1821. Throughout the 1820s, small notes were issued by regional banks. This was restricted in 1826, while the Bank of England was allowed to set up regional branches. In 1833 however, Bank of England notes were made legal tender and redemption by other banks was discouraged. In 1844, the Bank Charter Act established that Bank of England notes were fully backed by gold and they became the legal standard. According to the strict interpretation of the gold standard, this 1844 act marked the establishment of a full gold standard for British money.

The pound left the gold standard in 1931 and a number of currencies of countries that historically had performed a large amount of their trade in sterling were pegged to sterling instead of to gold. The Bank of England took the decision to leave the gold standard abruptly and unilaterally.[14]

United States

In the 1780s, Thomas Jefferson, Robert Morris and Alexander Hamilton recommended to Congress the value of a decimal system. This system would also apply to monies in the United States. The question was what type of standard: gold, silver or both.[15] The United States adopted a silver standard based on the Spanish milled dollar in 1785.

International

From 1860 to 1871 various attempts to resurrect bi-metallic standards were made, including one based on the gold and silver franc; however, with the rapid influx of silver from new deposits, the expectation of scarce silver ended.

The interaction between central banking and currency basis formed the primary source of monetary instability during this period. The combination of a restricted supply of notes, a government monopoly on note issuance and indirectly, a central bank and a single unit of value produced economic stability. Deviation from these conditions produced monetary crises.

Devalued notes or leaving silver as a store of value caused economic problems. Governments, demanding specie as payment, could drain the money out of the economy. Economic development expanded need for credit. The need for a solid basis in monetary affairs produced a rapid acceptance of the gold standard in the period that followed.

Japan

Following Germany's decision after the 1870–1871 Franco-Prussian War to extract reparations to facilitate a move to the gold standard, Japan gained the needed reserves after the Sino-Japanese War of 1894–1895. For Japan, moving to gold was considered vital for gaining access to Western capital markets.[16]

Bimetallic standard

US: Pre-Civil War

In 1792, Congress passed the Mint and Coinage Act. It authorized the federal government's use of the Bank of the United States to hold its reserves, as well as establish a fixed ratio of gold to the U.S. dollar. Gold and silver coins were legal tender, as was the Spanish real. In 1792 the market price of gold was about 15 times that of silver.[15] Silver coins left circulation, exported to pay for the debts taken on to finance the American Revolutionary War. In 1806 President Jefferson suspended the minting of silver coins. This resulted in a derivative silver standard, since the Bank of the United States was not required to fully back its currency with reserves. This began a long series of attempts by the United States to create a bi-metallic standard.

The intention was to use gold for large denominations, and silver for smaller denominations. A problem with bimetallic standards was that the metals' absolute and relative market prices changed. The mint ratio (the rate at which the mint was obligated to pay/receive for gold relative to silver) remained fixed at 15 ounces of silver to 1 ounce of gold, whereas the market rate fluctuated from 15.5 to 1 to 16 to 1. With the Coinage Act of 1834, Congress passed an act that changed the mint ratio to approximately 16 to 1. Gold discoveries in California in 1848 and later in Australia lowered the gold price relative to silver; this drove silver money from circulation because it was worth more in the market than as money.[17] Passage of the Independent Treasury Act of 1848 placed the U.S. on a strict hard-money standard. Doing business with the American government required gold or silver coins.

Government accounts were legally separated from the banking system. However, the mint ratio (the fixed exchange rate between gold and silver at the mint) continued to overvalue gold. In 1853, the U.S. reduced the silver weight of coins to keep them in circulation and in 1857 removed legal tender status from foreign coinage. In 1857 the final crisis of the free banking era began as American banks suspended payment in silver, with ripples through the developing international financial system. Due to the inflationary finance measures undertaken to help pay for the U.S. Civil War, the government found it difficult to pay its obligations in gold or silver and suspended payments of obligations not legally specified in specie (gold bonds); this led banks to suspend the conversion of bank liabilities (bank notes and deposits) into specie. In 1862 paper money was made legal tender. It was a fiat money (not convertible on demand at a fixed rate into specie). These notes came to be called "greenbacks".[17]

US: Post-Civil War

After the Civil War, Congress wanted to reestablish the metallic standard at pre-war rates. The market price of gold in greenbacks was above the pre-War fixed price ($20.67 per ounce of gold) requiring deflation to achieve the pre-War price. This was accomplished by growing the stock of money less rapidly than real output. By 1879 the market price matched the mint price of gold. The coinage act of 1873 (also known as the Crime of ‘73) demonetized silver. This act removed the 412.5 grain silver dollar from circulation. Subsequently silver was only used in coins worth less than $1 (fractional currency). With the resumption of convertibility on June 30, 1879 the government again paid its debts in gold, accepted greenbacks for customs and redeemed greenbacks on demand in gold. Greenbacks were therefore perfect substitutes for gold coins. During the latter part of the nineteenth century the use of silver and a return to the bimetallic standard were recurrent political issues, raised especially by William Jennings Bryan, the People's Party and the Free Silver movement. In 1900 the gold dollar was declared the standard unit of account and a gold reserve for government issued paper notes was established. Greenbacks, silver certificates, and silver dollars continued to be legal tender, all redeemable in gold.[17]

Fluctuations in the U.S. gold stock, 1862–1877

| US gold stock | |

|---|---|

| 1862 | 59 tons |

| 1866 | 81 tons |

| 1875 | 50 tons |

| 1878 | 78 tons |

The U.S. had a gold stock of 1.9 million ounces (59 t) in 1862. Stocks rose to 2.6 million ounces (81 t) in 1866, declined in 1875 to 1.6 million ounces (50 t) and rose to 2.5 million ounces (78 t) in 1878. Net exports did not mirror that pattern. In the decade before the Civil War net exports were roughly constant; postwar they varied erratically around pre-war levels, but fell significantly in 1877 and became negative in 1878 and 1879. The net import of gold meant that the foreign demand for American currency to purchase goods, services, and investments exceeded the corresponding American demands for foreign currencies. In the final years of the greenback period (1862–1879), gold production increased while gold exports decreased. The decrease in gold exports was considered by some to be a result of changing monetary conditions. The demands for gold during this period were as a speculative vehicle, and for its primary use in the foreign exchange markets financing international trade. The major effect of the increase in gold demand by the public and Treasury was to reduce exports of gold and increase the Greenback price of gold relative to purchasing power.[18]

Gold exchange standard

Towards the end of the 19th century, some silver standard countries began to peg their silver coin units to the gold standards of the United Kingdom or the United States. In 1898, British India pegged the silver rupee to the pound sterling at a fixed rate of 1s 4d, while in 1906, the Straits Settlements adopted a gold exchange standard against sterling, fixing the silver Straits dollar at 2s 4d.

Around the start of the 20th century, the Philippines pegged the silver peso/dollar to the U.S. dollar at 50 cents. This move was assisted by the passage of the Philippines Coinage Act by the United States Congress on March 3, 1903.[19] Around the same time Mexico and Japan pegged their currencies to the dollar. When Siam adopted a gold exchange standard in 1908, only China and Hong Kong remained on the silver standard.

When adopting the gold standard, many European nations changed the name of their currency, for instance from Daler (Sweden and Denmark) or Gulden (Austria-Hungary) to Crown, since the former names were traditionally associated with silver coins and the latter with gold coins.

Impact of World War I

Governments with insufficient tax revenue suspended convertibility repeatedly in the 19th century. The real test, however, came in the form of World War I, a test which "it failed utterly" according to economist Richard Lipsey.[3]

By the end of 1913, the classical gold standard was at its peak but World War I caused many countries to suspend or abandon it.[20] According to Lawrence Officer the main cause of the gold standard's failure to resume its previous position after World War I was “the Bank of England's precarious liquidity position and the gold-exchange standard.” A run on sterling caused Britain to impose exchange controls that fatally weakened the standard; convertibility was not legally suspended, but gold prices no longer played the role that they did before.[21] In financing the war and abandoning gold, many of the belligerents suffered drastic inflations. Price levels doubled in the U.S. and Britain, tripled in France and quadrupled in Italy. Exchange rates changed less, even though European inflations were more severe than America's. This meant that the costs of American goods decreased relative to those in Europe. Between August 1914 and spring of 1915, the dollar value of U.S. exports tripled and its trade surplus exceeded $1 billion for the first time.[22]

Ultimately, the system could not deal quickly enough with the large balance of payments deficits and surpluses; this was previously attributed to downward wage rigidity brought about by the advent of unionized labor, but is now considered as an inherent fault of the system that arose under the pressures of war and rapid technological change. In any case, prices had not reached equilibrium by the time of the Great Depression, which served to kill off the system completely.[3]

For example, Germany had gone off the gold standard in 1914, and could not effectively return to it because War reparations had cost it much of its gold reserves. During the Occupation of the Ruhr the German central bank (Reichsbank) issued enormous sums of non-convertible marks to support workers who were on strike against the French occupation and to buy foreign currency for reparations; this led to the German hyperinflation of the early 1920s and the decimation of the German middle class.

The U.S. did not suspend the gold standard during the war. The newly created Federal Reserve intervened in currency markets and sold bonds to “sterilize” some of the gold imports that would have otherwise increased the stock of money. By 1927 many countries had returned to the gold standard.[17] As a result of World War I the United States, which had been a net debtor country, had become a net creditor by 1919.[23]

Abandonment of the gold standard

The gold specie standard ended in the United Kingdom and the rest of the British Empire at the outbreak of World War I, when Treasury notes replaced the circulation of gold sovereigns and gold half sovereigns. Legally, the gold specie standard was not repealed. The end of the gold standard was successfully effected by the Bank of England through appeals to patriotism urging citizens not to redeem paper money for gold specie. It was only in 1925, when Britain returned to the gold standard in conjunction with Australia and South Africa, that the gold specie standard was officially ended.

The British Gold Standard Act 1925 both introduced the gold bullion standard and simultaneously repealed the gold specie standard. The new standard ended the circulation of gold specie coins. Instead, the law compelled the authorities to sell gold bullion on demand at a fixed price, but "only in the form of bars containing approximately four hundred ounces troy [12 kg] of fine gold".[24][25] John Maynard Keynes, citing deflationary dangers, argued against resumption of the gold standard.[26] By fixing the price at the pre-war rate of $4.86, Churchill is argued to have made an error that led to depression, unemployment and the 1926 general strike. The decision was described by Andrew Turnbull as a "historic mistake".[27]

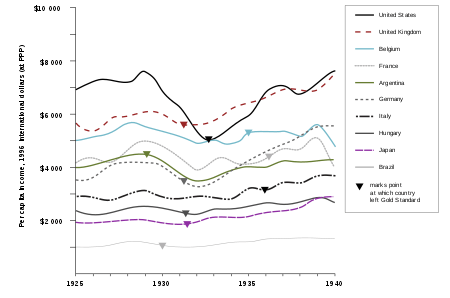

Many other countries followed Britain in returning to the gold standard, leading to a period of relative stability but also deflation.[28] This state of affairs lasted until the Great Depression (1929–1939) forced countries off the gold standard. On September 19, 1931, speculative attacks on the pound led the Bank of England to abandon the gold standard, ostensibly "temporarily".[14] However, the ostensibly temporary departure from the gold standard had unexpectedly positive effects on the economy, leading to greater acceptance of departing from the gold standard.[14] Loans from American and French Central Banks of £50,000,000 were insufficient and exhausted in a matter of weeks, due to large gold outflows across the Atlantic.[29][30][31] The British benefited from this departure. They could now use monetary policy to stimulate the economy. Australia and New Zealand had already left the standard and Canada quickly followed suit.

The interwar partially-backed gold standard was inherently unstable because of the conflict between the expansion of liabilities to foreign central banks and the resulting deterioration in the Bank of England's reserve ratio. France was then attempting to make Paris a world class financial center, and it received large gold flows as well.[32]

In May 1931 a run on Austria's largest commercial bank caused it to fail. The run spread to Germany, where the central bank also collapsed. International financial assistance was too late and in July 1931 Germany adopted exchange controls, followed by Austria in October. The Austrian and German experiences, as well as British budgetary and political difficulties, were among the factors that destroyed confidence in sterling, which occurred in mid-July 1931. Runs ensued and the Bank of England lost much of its reserves.

Depression and World War II

Great Depression

Some economic historians, such as Barry Eichengreen, blame the gold standard of the 1920s for prolonging the economic depression which started in 1929 and lasted for about a decade.[34] In the United States, adherence to the gold standard prevented the Federal Reserve from expanding the money supply to stimulate the economy, fund insolvent banks and fund government deficits that could "prime the pump" for an expansion. Once off the gold standard, it became free to engage in such money creation. The gold standard limited the flexibility of the central banks' monetary policy by limiting their ability to expand the money supply. In the US, the central bank was required by the Federal Reserve Act (1913) to have gold backing 40% of its demand notes.[35] Others, including former Federal Reserve Chairman Ben Bernanke and Nobel Prize-winner Milton Friedman, place the blame for the severity and length of the Great Depression at the feet of the Federal Reserve, mostly due to the deliberate tightening of monetary policy even after the end of the gold standard.[36] They blamed the U.S. major economic contraction in 1937 on tightening of monetary policy resulting in higher cost of capital, weaker securities markets, reduced net government contribution to income, the undistributed profits tax and higher labor costs.[37] The money supply peaked in March 1937, with a trough in May 1938.[38]

Higher interest rates intensified the deflationary pressure on the dollar and reduced investment in U.S. banks. Commercial banks converted Federal Reserve Notes to gold in 1931, reducing its gold reserves and forcing a corresponding reduction in the amount of currency in circulation. This speculative attack created a panic in the U.S. banking system. Fearing imminent devaluation many depositors withdrew funds from U.S. banks.[39] As bank runs grew, a reverse multiplier effect caused a contraction in the money supply.[40] Additionally the New York Fed had loaned over $150 million in gold (over 240 tons) to European Central Banks. This transfer contracted the U.S. money supply. The foreign loans became questionable once Britain, Germany, Austria and other European countries went off the gold standard in 1931 and weakened confidence in the dollar.[41]

The forced contraction of the money supply resulted in deflation. Even as nominal interest rates dropped, deflation-adjusted real interest rates remained high, rewarding those who held onto money instead of spending it, further slowing the economy.[42] Recovery in the United States was slower than in Britain, in part due to Congressional reluctance to abandon the gold standard and float the U.S. currency as Britain had done.[43]

In the early 1930s, the Federal Reserve defended the dollar by raising interest rates, trying to increase the demand for dollars. This helped attract international investors who bought foreign assets with gold.[39]

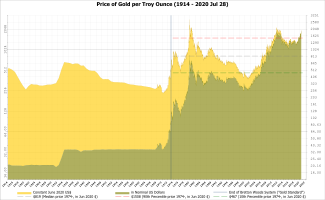

Congress passed the Gold Reserve Act on 30 January 1934; the measure nationalized all gold by ordering Federal Reserve banks to turn over their supply to the U.S. Treasury. In return the banks received gold certificates to be used as reserves against deposits and Federal Reserve notes. The act also authorized the president to devalue the gold dollar. Under this authority the president, on 31 January 1934, changed the value of the dollar from $20.67 to the troy ounce to $35 to the troy ounce, a devaluation of over 40%.

Other factors in the prolongation of the Great Depression include trade wars and the reduction in international trade caused by barriers such as Smoot–Hawley Tariff in the U.S. and the Imperial Preference policies of Great Britain, the failure of central banks to act responsibly,[44] government policies designed to prevent wages from falling, such as the Davis–Bacon Act of 1931, during the deflationary period resulting in production costs dropping slower than sales prices, thereby injuring business profits[45] and increases in taxes to reduce budget deficits and to support new programs such as Social Security. The U.S. top marginal income tax rate went from 25% to 63% in 1932 and to 79% in 1936,[46] while the bottom rate increased over tenfold, from .375% in 1929 to 4% in 1932.[47] The concurrent massive drought resulted in the U.S. Dust Bowl.

The Austrian School asserted that the Great Depression was the result of a credit bust.[48] Alan Greenspan wrote that the bank failures of the 1930s were sparked by Great Britain dropping the gold standard in 1931. This act "tore asunder" any remaining confidence in the banking system.[49] Financial historian Niall Ferguson wrote that what made the Great Depression truly 'great' was the European banking crisis of 1931.[50] According to Fed Chairman Marriner Eccles, the root cause was the concentration of wealth resulting in a stagnating or decreasing standard of living for the poor and middle class. These classes went into debt, producing the credit explosion of the 1920s. Eventually the debt load grew too heavy, resulting in the massive defaults and financial panics of the 1930s.[51]

World War II

Under the Bretton Woods international monetary agreement of 1944, the gold standard was kept without domestic convertibility. The role of gold was severely constrained, as other countries’ currencies were fixed in terms of the dollar. Many countries kept reserves in gold and settled accounts in gold. Still they preferred to settle balances with other currencies, with the American dollar becoming the favorite. The International Monetary Fund was established to help with the exchange process and assist nations in maintaining fixed rates. Within Bretton Woods adjustment was cushioned through credits that helped countries avoid deflation. Under the old standard, a country with an overvalued currency would lose gold and experience deflation until the currency was again valued correctly. Most countries defined their currencies in terms of dollars, but some countries imposed trading restrictions to protect reserves and exchange rates. Therefore, most countries' currencies were still basically inconvertible. In the late 1950s, the exchange restrictions were dropped and gold became an important element in international financial settlements.[17]

Bretton Woods

After the Second World War, a system similar to a gold standard and sometimes described as a "gold exchange standard" was established by the Bretton Woods Agreements. Under this system, many countries fixed their exchange rates relative to the U.S. dollar and central banks could exchange dollar holdings into gold at the official exchange rate of $35 per ounce; this option was not available to firms or individuals. All currencies pegged to the dollar thereby had a fixed value in terms of gold.[3]

Starting in the 1959–1969 administration of President Charles de Gaulle and continuing until 1970, France reduced its dollar reserves, exchanging them for gold at the official exchange rate, reducing U.S. economic influence. This, along with the fiscal strain of federal expenditures for the Vietnam War and persistent balance of payments deficits, led U.S. President Richard Nixon to end international convertibility of the U.S. dollar to gold on August 15, 1971 (the "Nixon Shock").

This was meant to be a temporary measure, with the gold price of the dollar and the official rate of exchanges remaining constant. Revaluing currencies was the main purpose of this plan. No official revaluation or redemption occurred. The dollar subsequently floated. In December 1971, the "Smithsonian Agreement" was reached. In this agreement, the dollar was devalued from $35 per troy ounce of gold to $38. Other countries' currencies appreciated. However, gold convertibility did not resume. In October 1973, the price was raised to $42.22. Once again, the devaluation was insufficient. Within two weeks of the second devaluation the dollar was left to float. The $42.22 par value was made official in September 1973, long after it had been abandoned in practice. In October 1976, the government officially changed the definition of the dollar; references to gold were removed from statutes. From this point, the international monetary system was made of pure fiat money.

Production of gold

An estimated total of 174,100 tonnes of gold have been mined in human history, according to GFMS as of 2012. This is roughly equivalent to 5.6 billion troy ounces or, in terms of volume, about 9,261 cubic metres (327,000 cu ft), or a cube 21 metres (69 ft) on a side. There are varying estimates of the total volume of gold mined. One reason for the variance is that gold has been mined for thousands of years. Another reason is that some nations are not particularly open about how much gold is being mined. In addition, it is difficult to account for the gold output in illegal mining activities.[52]

World production for 2011 was circa 2,700 tonnes. Since the 1950s, annual gold output growth has approximately kept pace with world population growth (i.e. a doubling in this period)[53] although it has lagged behind world economic growth (approximately 8-fold increase since the 1950s,[54] and 4x since 1980[55]).

Theory

Commodity money is inconvenient to store and transport in large amounts. Furthermore, it does not allow a government to manipulate the flow of commerce with the same ease that a fiat currency does. As such, commodity money gave way to representative money and gold and other specie were retained as its backing.

Gold was a preferred form of money due to its rarity, durability, divisibility, fungibility and ease of identification,[56] often in conjunction with silver. Silver was typically the main circulating medium, with gold as the monetary reserve. Commodity money was anonymous, as identifying marks can be removed. Commodity money retains its value despite what may happen to the monetary authority. After the fall of South Vietnam, many refugees carried their wealth to the West in gold after the national currency became worthless.

Under commodity standards currency itself has no intrinsic value, but is accepted by traders because it can be redeemed any time for the equivalent specie. A U.S. silver certificate, for example, could be redeemed for an actual piece of silver.

Representative money and the gold standard protect citizens from hyperinflation and other abuses of monetary policy, as were seen in some countries during the Great Depression. Commodity money conversely led to deflation and bank runs.

Countries that left the gold standard earlier than other countries recovered from the Great Depression sooner. For example, Great Britain and the Scandinavian countries, which left the gold standard in 1931, recovered much earlier than France and Belgium, which remained on gold much longer. Countries such as China, which had a silver standard, almost entirely avoided the depression (due to the fact it was then barely integrated into the global economy). The connection between leaving the gold standard and the severity and duration of the depression was consistent for dozens of countries, including developing countries. This may explain why the experience and length of the depression differed between national economies.[57]

Variations

A full or 100%-reserve gold standard exists when the monetary authority holds sufficient gold to convert all the circulating representative money into gold at the promised exchange rate. It is sometimes referred to as the gold specie standard to more easily distinguish it. Opponents of a full standard consider it difficult to implement, saying that the quantity of gold in the world is too small to sustain worldwide economic activity at or near current gold prices; implementation would entail a many-fold increase in the price of gold. Gold standard proponents have said, "Once a money is established, any stock of money becomes compatible with any amount of employment and real income."[58] While prices would necessarily adjust to the supply of gold, the process may involve considerable economic disruption, as was experienced during earlier attempts to maintain gold standards.[59]

In an international gold-standard system (which is necessarily based on an internal gold standard in the countries concerned),[60] gold or a currency that is convertible into gold at a fixed price is used to make international payments. Under such a system, when exchange rates rise above or fall below the fixed mint rate by more than the cost of shipping gold, inflows or outflows occur until rates return to the official level. International gold standards often limit which entities have the right to redeem currency for gold.

Impact

A poll of forty prominent U.S. economists conducted by the IGM Economic Experts Panel in 2012 found that none of them believed that returning to the gold standard would be economically beneficial. The specific statement with which the economists were asked to agree or disagree was: "If the U.S. replaced its discretionary monetary policy regime with a gold standard, defining a 'dollar' as a specific number of ounces of gold, the price-stability and employment outcomes would be better for the average American." 40% of the economists disagreed, and 53% strongly disagreed with the statement; the rest did not respond to the question. The panel of polled economists included past Nobel Prize winners, former economic advisers to both Republican and Democratic presidents, and senior faculty from Harvard, Chicago, Stanford, MIT, and other well-known research universities.[61]

The economist Allan H. Meltzer of Carnegie Mellon University was known for refuting Ron Paul's advocacy of the gold standard from the 1970s onward. He sometimes summarized his opposition by stating simply, "[W]e don’t have the gold standard. It’s not because we don’t know about the gold standard, it’s because we do."[62]

Advantages

According to Michael D. Bordo, the gold standard has three benefits: "its record as a stable nominal anchor; its automaticity; and its role as a credible commitment mechanism."[63]

- Long-term price stability has been described as one of the virtues of the gold standard,[64] but historical data shows that the magnitude of short run swings in prices were far higher under the gold standard.[65][66][64]

- The gold standard provides fixed international exchange rates between participating countries and thus reduces uncertainty in international trade. Historically, imbalances between price levels were offset by a balance-of-payment adjustment mechanism called the "price–specie flow mechanism".[67] Gold used to pay for imports reduces the money supply of importing nations, causing deflation, which makes them more competitive, while the importation of gold by net exporters serves to increase their money supply, causing inflation, making them less competitive.[68]

- A gold standard does not allow some types of financial repression.[69] Financial repression acts as a mechanism to transfer wealth from creditors to debtors, particularly the governments that practice it. Financial repression is most successful in reducing debt when accompanied by inflation and can be considered a form of taxation.[70][71] In 1966 Alan Greenspan wrote "Deficit spending is simply a scheme for the confiscation of wealth. Gold stands in the way of this insidious process. It stands as a protector of property rights. If one grasps this, one has no difficulty in understanding the statists' antagonism toward the gold standard."[72]

Disadvantages

- The unequal distribution of gold deposits makes the gold standard more advantageous for those countries that produce gold.[73] In 2010 the largest producers of gold, in order, were China, Australia, U.S., South Africa and Russia.[74] The country with the largest unmined gold deposits is Australia.[75]

- Some economists believe that the gold standard acts as a limit on economic growth. "As an economy's productive capacity grows, then so should its money supply. Because a gold standard requires that money be backed in the metal, then the scarcity of the metal constrains the ability of the economy to produce more capital and grow."[76]

- Mainstream economists believe that economic recessions can be largely mitigated by increasing the money supply during economic downturns.[77] A gold standard means that the money supply would be determined by the gold supply and hence monetary policy could no longer be used to stabilize the economy.[78]

- Although the gold standard brings long-run price stability, it is historically associated with high short-run price volatility.[64][79] It has been argued by Schwartz, among others, that instability in short-term price levels can lead to financial instability as lenders and borrowers become uncertain about the value of debt.[79]

- Deflation punishes debtors.[80][81] Real debt burdens therefore rise, causing borrowers to cut spending to service their debts or to default. Lenders become wealthier, but may choose to save some of the additional wealth, reducing GDP.[82]

- The money supply would essentially be determined by the rate of gold production. When gold stocks increase more rapidly than the economy, there is inflation and the reverse is also true.[64][83] The consensus view is that the gold standard contributed to the severity and length of the Great Depression, as under the gold standard central banks could not expand credit at a fast enough rate to offset deflationary forces.[84][85][86]

- Hamilton contended that the gold standard is susceptible to speculative attacks when a government's financial position appears weak. Conversely, this threat discourages governments from engaging in risky policy (see moral hazard). For example, the U.S. was forced to contract the money supply and raise interest rates in September 1931 to defend the dollar after speculators forced the UK off the gold standard.[86][87][88][89]

- Devaluing a currency under a gold standard would generally produce sharper changes than the smooth declines seen in fiat currencies, depending on the method of devaluation.[90]

- Most economists favor a low, positive rate of inflation of around 2%. This reflects fear of deflationary shocks and the belief that active monetary policy can dampen fluctuations in output and unemployment. Inflation gives them room to tighten policy without inducing deflation.[91]

- A gold standard provides practical constraints against the measures that central banks might otherwise use to respond to economic crises.[92] Creation of new money reduces interest rates and thereby increases demand for new lower cost debt, raising the demand for money.[93]

Advocates

A return to the gold standard was considered by the U.S. Gold Commission back in 1982, but found only minority support.[94] In 2001 Malaysian Prime Minister Mahathir bin Mohamad proposed a new currency that would be used initially for international trade among Muslim nations, using a Modern Islamic gold dinar, defined as 4.25 grams of pure (24-carat) gold. Mahathir claimed it would be a stable unit of account and a political symbol of unity between Islamic nations. This would purportedly reduce dependence on the U.S. dollar and establish a non-debt-backed currency in accord with Sharia law that prohibited the charging of interest.[95] However, this proposal has not been taken up, and the global monetary system continues to rely on the U.S. dollar as the main trading and reserve currency.[96]

Former U.S. Federal Reserve Chairman Alan Greenspan acknowledged he was one of "a small minority" within the central bank that had some positive view on the gold standard.[97] In a 1966 essay he contributed to a book by Ayn Rand, titled "Gold and Economic Freedom", Greenspan argued the case for returning to a 'pure' gold standard; in that essay he described supporters of fiat currencies as "welfare statists" intending to use monetary policy to finance deficit spending.[98] More recently he claimed that by focusing on targeting inflation "central bankers have behaved as though we were on the gold standard", rendering a return to the standard unnecessary.[99]

Similarly, economists like Robert Barro argued that whilst some form of "monetary constitution" is essential for stable, depoliticized monetary policy, the form this constitution takes—for example, a gold standard, some other commodity-based standard, or a fiat currency with fixed rules for determining the quantity of money—is considerably less important.[100]

The gold standard is supported by many followers of the Austrian School of Economics, free-market libertarians and some supply-siders.[101]

U.S. politics

Former congressman Ron Paul is a long-term, high-profile advocate of a gold standard, but has also expressed support for using a standard based on a basket of commodities that better reflects the state of the economy.[102]

In 2011 the Utah legislature passed a bill to accept federally issued gold and silver coins as legal tender to pay taxes.[103] As federally issued currency, the coins were already legal tender for taxes, although the market price of their metal content currently exceeds their monetary value. As of 2011 similar legislation was under consideration in other U.S. states.[104] The bill was initiated by newly elected Republican Party legislators associated with the Tea Party movement and was driven by anxiety over the policies of President Barack Obama.[105]

A 2012 survey of forty economists by the University of Chicago business school found that none agreed that returning to a gold standard would improve price stability and employment outcomes for the average American.[106][61]

In 2013, the Arizona Legislature passed SB 1439, which would have made gold and silver coin a legal tender in payment of debt, but the bill was vetoed by the Governor.[107]

In 2015, some Republican candidates for the 2016 presidential election advocated for a gold standard, based on concern that the Federal Reserve's attempts to increase economic growth may create inflation. Economic historians did not agree with the candidates' assertions that the gold standard would benefit the U.S. economy.[106]

See also

- A Program for Monetary Reform (1939) – The Gold Standard

- Bimetallism/Free Silver

- Black Friday (1869)—Also referred to as the Gold Panic of 1869

- Coinage Act of 1792

- Coinage Act of 1873

- Executive Order 6102

- Full-reserve banking

- Gold as an investment

- Gold dinar

- Gold points

- Hard money (policy)

- Metal as money

- Metallism

International institutions

- Bank for International Settlements

- International Monetary Fund

- United Nations Monetary and Financial Conference

- World Bank

References

- "Gold standard Facts, information, pictures Encyclopedia.com articles about Gold standard". www.encyclopedia.com. Retrieved 2015-12-05.

- William O. Scroggs. "What Is Left of the Gold Standard?". foreignaffairs.com. Retrieved 28 January 2015.

- Lipsey 1975, pp. 683-702.

- Bordo, Dittmar & Gavin 2003 "in a world with two capital goods, the one with the lower depreciation rate emerges as commodity money"

- "World's Oldest Coin - First Coins". rg.ancients.info. Retrieved 2015-12-05.

- Lopez, Robert Sabatino (Summer 1951). "The Dollar of the Middle Ages". The Journal of Economic History. 11 (3): 209–234. doi:10.1017/s0022050700084746. JSTOR 2113933.

- Especially the period 1500-1870; K. Kıvanç Karaman, Sevket Pamuk, and Seçil Yıldırım-Karaman, "Money and Monetary Stability in Europe, 1300-1914", column for Vox Center for Economic and Policy Research (24 February 2018); available online at https://voxeu.org/article/money-and-monetary-stability-europe-1300-1914

- Keary, Charles Francis. (2005). A Catalogue of English Coins in the British Museum. Anglo-Saxon Series. Volume I. Poole, Reginald Stewart, ed. Elibron Classics. pp. ii, xxii–xxv

- Rothwell, Richard Pennefather. (1893). Universal Bimetallism and An International Monetary Clearing House, together with A Record of the World's Money, Statistics of Gold and Silver, Etc. New York: The Scientific Publishing Company. pp. 45.

- Andrei, Liviu C. (2011). Money and Market in the Economy of All Times: Another World History of Money and Pre-Money Based Economies. Xlibris Corporation. pp. 146–147.

- James Powell, A History of the Canadian Dollar (Ottawa: Bank of Canada, 2005), pp. 22-23, 33.

- Consolidated Statutes of Newfoundland (1st Series, 1874), Title XXV, "Of the Regulation of Trade in Certain Cases", c. 92, Of the Currency, s. 8.

- "Small change". UK Parliament. Retrieved 2019-02-09.

- Morrison, James Ashley (2016). "Shocking Intellectual Austerity: The Role of Ideas in the Demise of the Gold Standard in Britain". International Organization. 70 (1): 175–207. doi:10.1017/S0020818315000314. ISSN 0020-8183.

- Walton & Rockoff 2010.

- Metzler, Mark (2006). Lever of Empire: The International Gold Standard and the Crisis of Liberalism in Prewar Japan. Berkeley: University of California Press. ISBN 978-0-520-24420-7.

- Elwell 2011.

- Friedman & Schwartz 1963, p. 79.

- Kemmerer, Edwin Walter (1994). Gold and the Gold Standard: The Story of Gold Money Past, Present and Future. Princeton, NJ: McGraw-Hill Book, Company, Inc. pp. 154 (238 pg). ISBN 9781610164429.

- Nicholson, J. S. (April 1915). "The Abandonment of the Gold Standard". The Quarterly Review. 223: 409–423.

- Officer

- Eichengreen 1995.

- Drummond, Ian M. The Gold Standard and the International Monetary System 1900–1939. Macmillan Education, LTD, 1987.

- "The Gold Standard Act Of 1925.pdf (PDFy mirror)". January 1, 2014 – via Internet Archive.

- "Articles: Free the Planet: Gold Standard Act 1925". Free the Planet. 2009-06-10. Archived from the original on 2012-07-13. Retrieved 2012-07-09.

- Keynes, John Maynard (1920). Economic Consequences of the Peace. New York: Harcourt, Brace and Rowe.

- "Thatcher warned Major about exchange rate risks before ERM crisis". The Guardian. 2017-12-29. Retrieved 2017-12-29.

- Cassel, Gustav. The Downfall of the Gold Standard. Oxford University Press, 1936.

- "Chancellor's Commons Speech". Freetheplanet.net. Archived from the original on 2012-07-09. Retrieved 2012-07-09.

- Eichengreen, Barry J. (September 15, 2008). Globalizing Capital: A History of the International Monetary System. Princeton University Press. pp. 61–. ISBN 978-0-691-13937-1. Retrieved November 23, 2010.

- Officer, Lawrence. "Breakdown of the Interwar Gold Standard". Eh.net. Archived from the original on November 24, 2005. Retrieved 2012-07-09.

- Officer, Lawrence. "there was ongoing tension with France, that resented the sterling-dominated gold- exchange standard and desired to cash in its sterling holding for gold to aid its objective of achieving first-class financial status for Paris". Eh.net. Archived from the original on November 24, 2005. Retrieved 2012-07-09.

- International data from Maddison, Angus. "Historical Statistics for the World Economy: 1–2003 AD".CS1 maint: ref=harv (link). Gold dates culled from historical sources, principally Eichengreen, Barry (1992). Golden Fetters: The Gold Standard and the Great Depression, 1919–1939. New York: Oxford University Press. ISBN 978-0-19-506431-5.CS1 maint: ref=harv (link)

- Eichengreen 1995, Preface.

- American Economic Association (2000–2011). "The Elasticity of the Federal Reserve Note". The American Economic Review. ITHAKA. 26 (4): 683–690. JSTOR 1807996.

- "Remarks by Governor Ben S. Bernanke At the Conference to Honor Milton Friedman". The Federal Reserve Board. November 8, 2002. Retrieved December 24, 2011.

- Friedman & Schwartz 1963, p. 543.

- Friedman & Schwartz 1963, p. 544.

- "FRB: Speech, Bernanke-Money, Gold, and the Great Depression – March 2, 2004". Federalreserve.gov. 2004-03-02. Retrieved 2010-07-24.

- "1931—"The Tragic Year"". Ludwig von Mises Institute. Retrieved December 24, 2011.

The inflationary attempts of the government from January to October were thus offset by the people's attempts to convert their bank deposits into legal tender" "Hence, the will of the public caused bank reserves to decline by $400 million in the latter half of 1931, and the money supply, as a consequence, fell by over four billion dollars in the same period.

- "1931—"The Tragic Year"". Ludwig von Mises Institute. Retrieved December 24, 2011.

Throughout the European crisis, the Federal Reserve, particularly the New York Bank, tried its best to aid the European governments and to prop up unsound credit positions. ... The New York Federal Reserve loaned, in 1931, $125 million to the Bank of England, $25 million to the German Reichsbank, and smaller amounts to Hungary and Austria. As a result, much frozen assets were shifted, to become burdens to the United States.

- "In the 1930s, the United States was in a situation that satisfied the conditions for a liquidity trap. Over 1929–1933 overnight rates fell to zero, and they remained on the floor through the 1930's" (PDF). Archived from the original on 2004-07-22.CS1 maint: BOT: original-url status unknown (link)

- The European Economy between Wars; Feinstein, Temin, and Toniolo

- M. Friedman "the severity of each of the major contractions – 1920–21, 1929–33 and 1937–38 is directly attributable to acts of commission and omission by the Reserve authorities".

- Robert P. Murphy. "Another major factor is that governments in the 1930s were interfering with wages and prices more so than at any prior point in (peacetime) history". Mises.org. Retrieved 2012-07-09.

- "High Taxes and High Budget Deficits-The Hoover–Roosevelt Tax Increases of the 1930s" (PDF).

- "per data from Economics Professor Mark J. Perry". Mjperry.blogspot.com. 2008-11-09. Retrieved 2012-07-09.

- Eichengreen, Barry; Mitchener, Kris (August 2003). "The Great Depression as a Credit Boom Gone Wrong" (PDF). Retrieved December 24, 2011.

- Gold and Economic Freedom by Alan Greenspan 1966 "Great Britain fared even worse, and rather than absorb the full consequences of her previous folly, she abandoned the gold standard completely in 1931, tearing asunder what remained of the fabric of confidence and inducing a world-wide series of bank failures."

- Farrell, Paul B. (December 13, 2011). "Our decade from hell will get worse in 2012". MarketWatch. Retrieved December 24, 2011.

As financial historian Niall Ferguson writes in Newsweek: "Double-Dip Depression ... We forget that the Great Depression was like a soccer match, there were two halves." The 1929 crash kicked off the first half. But what "made the depression truly 'great' ... began with the European banking crisis of 1931." Sound familiar?

- Aftershock by Robert B. Reich, published 2010 Chapter 1 Eccles's Insight.

- Prior, Ed (1 April 2013). "How much gold is there in the world?" – via www.bbc.com.

- "FAQs | Investment | World Gold Council". Gold.org. Retrieved 2013-09-12.

- "Measuring Worth - GDP result".

- "Download entire World Economic Outlook database, April 2013".

- Krech III, Shepard; McNeill, John Robert; Merchant, Carolyn (2004). Encyclopedia of World Environmental History. 2: F–N. New York City: Routledge. p. 597. ISBN 978-0-415-93734-4. OCLC 174950341.

- Bernanke, Ben (March 2, 2004), "Remarks by Governor Ben S. Bernanke: Money, Gold and the Great Depression", At the H. Parker Willis Lecture in Economic Policy, Washington and Lee University, Lexington, Virginia.

- Hoppe, Hans-Herman (1992). Mark Skousen (ed.). Dissent on Keynes, A Critical Appraisal of Economics. pp. 199–223.

- "Gold as Money: FAQ". Mises.org. Ludwig von Mises Institute. Archived from the original on July 14, 2011. Retrieved 12 August 2011.

- The New Palgrave Dictionary of Economics, 2nd edition (2008), Vol.3, S.695

- "Gold Standard". IGM Forum. 12 January 2012. Retrieved 27 December 2015.

- Bowyer, Jerry (23 October 2013). "My Friendly Debate On The Gold Standard With Allan Meltzer, The World's Leading Monetarist". Forbes / Contributor Opinions. Retrieved 27 December 2015.

- Bordo, Michael D. (May 1999). "The Gold Standard and Related Regimes: Collected Essays". Cambridge Core. doi:10.1017/cbo9780511559624. Retrieved 2020-03-28.

- Bordo 2008.

- "Why the Gold Standard Is the World's Worst Economic Idea, in 2 Charts – Matthew O'Brien". The Atlantic. 2012-08-26. Retrieved 2013-04-19.

- Kydland, Finn E. (1999). "The Gold Standard as a Commitment Mechanism". The Gold Standard and Related Regimes: Collected Essays. Cambridge University Press. Retrieved 2020-03-28.

- "Advantages of the Gold Standard" (PDF). The Gold Standard: Perspectives in the Austrian School. The Ludwig von Mises Institute. Retrieved 9 January 2011.

- "Reform of the International Monetary and Financial System" (PDF). Bank of England. December 2011. Archived from the original (PDF) on December 18, 2011. Retrieved December 24, 2011.

Countries with current account surpluses accumulated gold, while deficit countries saw their gold stocks diminish. This, in turn, contributed to upward pressure on domestic spending and prices in surplus countries and downward pressure on them in deficit countries, thereby leading to a change ... that should, eventually, have reduced imbalances.

- "Financial Repression Redux". International Monetary Fund. June 2011. Retrieved December 24, 2011.

Financial repression occurs when governments implement policies to channel to themselves funds that in a deregulated market environment would go elsewhere

- Reinhart, Carmen M.; Rogoff, Kenneth S. (2008). This Time is Different. Princeton University Press. p. 143.

- Giovannini, Alberto; De Melo, Martha (1993). "Government Revenue from Financial Repression". The American Economic Review. 83 (4): 953–963. JSTOR 2117587.

- Greenspan, Alan (1966). "Gold and Economic Freedom". Constitution.org. Retrieved December 24, 2011.

- Goodman, George J.W., Paper Money, 1981, p. 165–6

- Hill, Liezel (January 13, 2011). "Gold mine output hit record in 2010, more gains likely this year – GFMS". Mining Weekly. Retrieved December 24, 2011.

- U.S. Geological Survey (January 2011). "GOLD" (PDF). U.S. Geological Survey, Mineral Commodity Summaries. U.S. Department of the Interior | U.S. Geological Survey. Retrieved 10 July 2012.

- Mayer, David A. Gold standard at Google Books The Everything Economics Book: From theory to practice, your complete guide to understanding economics today (Everything Series) ISBN 978-1-4405-0602-4. 2010. pp. 33–34.

- Mankiw, N. Gregory (2002). Macroeconomics (5th ed.). Worth. pp. 238–255. ISBN 978-0-324-17190-7.

- Krugman, Paul. "The Gold Bug Variations". Slate.com. Retrieved 2009-02-13.

- Bordo, Dittmar & Gavin 2003.

- Keogh, Bryan (May 13, 2009). "Real Rate Shock Hits CEOs as Borrowing Costs Impede Recovery". Bloomberg. Retrieved December 24, 2011.

Deflation hurts borrowers and rewards savers," said Drew Matus, senior economist at Banc of America Securities-Merrill Lynch in New York, in a telephone interview. "If you do borrow right now, and we go through a period of deflation, your cost of borrowing just went through the roof.

- Mauldin, John; Tepper, Jonathan (2011-02-09). Endgame: The End of the Debt SuperCycle and How It Changes Everything. Hoboken, N.J.: John Wiley. ISBN 978-1-118-00457-9.

- "The greater of two evils". The Economist. May 7, 2009. Retrieved December 24, 2011.

- DeLong, Brad (1996-08-10). "Why Not the Gold Standard?". Berkeley, California: University of California, Berkeley. Archived from the original on 2010-10-18. Retrieved 2008-09-25.

- Timberlake, Richard H. (2005). "Gold Standards and the Real Bills Doctrine in US Monetary Policy". Econ Journal Watch. 2 (2): 196–233.

- Warburton, Clark (1966). "The Monetary Disequilibrium Hypothesis". Depression, Inflation, and Monetary Policy: Selected Papers, 1945–1953. Baltimore: Johns Hopkins University Press. pp. 25–35. OCLC 736401.

- Hamilton 2005.

- Hamilton 1988.

- Christina D. Romer (20 December 2003). "Great Depression" (PDF). ELSA. University of California Regents. Archived from the original (PDF) on 7 December 2011. Retrieved 10 July 2012.

- "Remarks by Governor Ben S. Bernanke". The Federal Reserve Board. March 2, 2004. Retrieved December 24, 2011.

"In September 1931, following a period of financial upheaval in Europe that created concerns about British investments on the Continent, speculators attacked the British pound, presenting pounds to the Bank of England and demanding gold in return. ... Unable to continue supporting the pound at its official value, Great Britain was forced to leave the gold standard, ... With the collapse of the pound, speculators turned their attention to the U.S. dollar

- McArdle, Megan (2007-09-04). "There's gold in them thar standards!". The Atlantic Monthly. Retrieved 2008-11-12.

- Hummel, Jeffrey Rogers. "Death and Taxes, Including Inflation: the Public versus Economists" (January 2007). p.56

- Demirgüç-Kunt, Asli; Enrica Detragiache (April 2005). "Cross-Country Empirical Studies of Systemic Bank Distress: A Survey". National Institute Economic Review. 192 (1): 68–83. doi:10.1177/002795010519200108. ISSN 0027-9501. OCLC 90233776. Retrieved 2008-11-12.

- "the quantity of money supplied by the Fed must be equal to the quantity demanded by money holders" (PDF). Archived from the original (PDF) on June 16, 2012. Retrieved 2012-07-09.

- Paul, Ron; Lewis Lehrman (1982). The case for gold: a minority report of the U.S. Gold Commission (PDF). Washington, D.C.: Cato Institute. p. 160. ISBN 978-0-932790-31-6. OCLC 8763972. Retrieved 2008-11-12.

- al-'Amraawi, Muhammad; Al-Khammar al-Baqqaali; Ahmad Saabir; Al-Hussayn ibn Haashim; Abu Sayf Kharkhaash; Mubarak Sa'doun al-Mutawwa'; Malik Abu Hamza Sezgin; Abdassamad Clarke; Asadullah Yate (2001-07-01). "Declaration of 'Ulama on the Gold Dinar". Islam i Dag. Archived from the original on 2008-06-24. Retrieved 2008-11-14.

- McGregor, Richard (2011-01-16). "Richard McGregor:Hu questions future role of US dollar. Financial Times, January 16, 2011". Financial Times. Retrieved December 24, 2011.

- "Conduct of Monetary Policy: Report of the Federal Reserve Board Pursuant to the Full Employment and Balanced Growth Act of 1978, P.L. 95-523 and The State of the Economy : Hearing Before the Subcommittee on Domestic and International Monetary Policy of the Committee on Banking and Financial Services, House of Representatives, One Hundred Fifth Congress, Second Session, July 22, 1998 - FRASER - St. Louis Fed".

- Greenspan, Alan (July 1966). "Gold and Economic Freedom". The Objectivist. 5 (7). Retrieved 2008-10-16.

- Paul, Ron. End the Fed. p. xxiii.

- Salerno 1982.

- Boaz, David (2009-03-12). "Time to Think about the Gold Standard?". Cato Institute. Retrieved 2018-05-05.

- Channel: CNBC. Show: Squawk Box. Date: 11/13/2009. Interview with Ron Paul

- Clark, Stephen (March 3, 2011). "Utah Considers Return to Gold, Silver Coins". Fox News. Retrieved December 24, 2011.

- "Utah: Forget dollars. How about gold?". CNN. 2011-03-29.

- Spillius, Alex (2011-03-18). "Tea Party legislation reveals anxiety at US direction under Barack Obama". The Daily Telegraph. London.

- Appelbaum, Binyamin (2015-12-01). "The Good Old Days of the Gold Standard? Not Really, Historians Say". The New York Times. ISSN 0362-4331. Retrieved 2015-12-02.

- http://www.azleg.gov/govlettr/51leg/1R/SB1439.pdf

Sources

- Bordo, Michael D.; Dittmar, Robert D.; Gavin, William T. (June 2003). "Gold, Fiat Money and Price Stability" (PDF). Working Paper Series. Research Division – Federal Reserve Bank of St. Louis. Retrieved December 24, 2011.CS1 maint: ref=harv (link)

- Cassel, Gustav. The Downfall of the Gold Standard. Oxford University Press, 1936.

- Drummond, Ian M. The Gold Standard and the International Monetary System 1900–1939. Macmillan Education, LTD, 1987.

- Eichengreen, Barry J. (1995). Golden Fetters: The Gold Standard and the Great Depression, 1919–1939. New York City: Oxford University Press. ISBN 978-0-19-510113-3. OCLC 34383450.CS1 maint: ref=harv (link)

- Elwell, Craig K. (2011). Brief History of the Gold Standard in the United States. Congressional Research Service.CS1 maint: ref=harv (link)

- Friedman, Milton; Schwartz, Anna Jacobson (1963). A Monetary History of the US 1867–1960. Princeton University Press. p. 543. ISBN 978-0-691-04147-6. Retrieved 2012-07-09.CS1 maint: ref=harv (link)

- Hamilton, James D. (April 1988). "Role of the International Gold Standard in Propagating the Great Depression". Contemporary Economic Policy. 6 (2): 67–89. doi:10.1111/j.1465-7287.1988.tb00286.x. Archived from the original on 2013-01-05. Retrieved 2008-11-12.CS1 maint: ref=harv (link)

- Lipsey, Richard G. (1975). An introduction to positive economics (fourth ed.). Weidenfeld & Nicolson. pp. 683–702. ISBN 978-0-297-76899-9.CS1 maint: ref=harv (link)

- Officer, Lawrence. "Gold Standard." 1 February 2010. EH.net. 13 April 2013.

Further reading

- Bensel, Richard Franklin (2000). The political economy of American industrialization, 1877–1900. Cambridge: Cambridge University Press. ISBN 978-0-521-77604-2. OCLC 43552761.

- Eichengreen, Barry J.; Marc Flandreau (1997). The gold standard in theory and history. New York City: Routledge. ISBN 978-0-415-15061-3. OCLC 37743323.

- Bordo, Michael D. (1999). Gold standard and related regimes: collected essays. Cambridge: Cambridge University Press. ISBN 978-0-521-55006-2. OCLC 59422152.

- Bordo, Michael D; Anna Jacobson Schwartz; National Bureau of Economic Research (1984). A Retrospective on the classical gold standard, 1821–1931. Chicago: University of Chicago Press. ISBN 978-0-226-06590-8. OCLC 10559587.

- Coletta, Paolo E. "Greenbackers, Goldbugs, and Silverites: Currency Reform and Politics, 1860-1897,” in H. Wayne Morgan (ed.), The Gilded Age: A Reappraisal. Syracuse, NY: Syracuse University Press, 1963; pp. 111–139.

- Officer, Lawrence H. (2007). Between the Dollar-Sterling Gold Points: Exchange Rates, Parity and Market Behavior. Chicago: Cambridge University Press. ISBN 978-0-521-03821-8. OCLC 124025586.

- Einaudi, Luca (2001). Money and politics: European monetary unification and the international gold standard (1865–1873). Oxford: Oxford University Press. ISBN 978-0-19-924366-2. OCLC 45556225.

- Roberts, Mark A (March 1995). "Keynes, the Liquidity Trap and the Gold Standard: A Possible Application of the Rational Expectations Hypothesis". The Manchester School of Economic & Social Studies. 61 (1): 82–92. doi:10.1111/j.1467-9957.1995.tb00270.x.

- Thompson, Earl A.; Charles Robert Hickson (2001). Ideology and the evolution of vital institutions: guilds, the gold standard, and modern international cooperation. Boston: Kluwer Acad. Publ. ISBN 978-0-7923-7390-2. OCLC 46836861.

- Pollard, Sidney (1970). The gold standard and employment policies between the Wars. London: Methuen. ISBN 978-0-416-14250-1. OCLC 137456.

- Hanna, Hugh Henry; Charles Arthur Conant; Jeremiah Jenks (1903). Stability of international exchange: Report on the introduction of the gold-exchange standard into China and other silver-using countries. OCLC 6671835.

- Banking in modern Japan. Tokyo: Fuji Bank. 1967. ISBN 978-0-333-71139-2. OCLC 254964565.

- Officer, Lawrence H. (2008). "bimetallism". In Steven N. Durlauf and Lawrence E. Blume (ed.). The New Palgrave Dictionary of Economics. The New Palgrave Dictionary of Economics, 2nd Edition. Basingstoke: Palgrave Macmillan. p. 488. doi:10.1057/9780230226203.0136. ISBN 978-0-333-78676-5. OCLC 181424188. Retrieved 2008-11-13.

- Drummond, Ian M.; The Economic History Society (1987). The gold standard and the international monetary system 1900–1939. Houndmills, Basingstoke, Hampshire: Macmillan Education. ISBN 978-0-333-37208-1. OCLC 18324084.

- Hawtrey, Ralph George (1927). The Gold Standard in theory and practice. London: Longman. ISBN 978-0-313-22104-0. OCLC 250855462.

- Flandreau, Marc (2004). The glitter of gold: France, bimetallism, and the emergence of the international gold standard, 1848–1873. Oxford: Oxford University Press. ISBN 978-0-19-925786-7. OCLC 54826941.

- Lalor, John (2003) [1881]. Cyclopedia of Political Science, Political Economy and the Political History of the United States. London: Thoemmes Continuum. ISBN 978-1-84371-093-6. OCLC 52565505.

- Bernanke, Ben; Harold James (October 1990). "The Gold Standard, Deflation, and Financial Crisis in the Great Depression: An International Comparison". NBER Working Paper No. 3488. doi:10.3386/w3488. Also published as: Bernanke, Ben; Harold James (1991). "The Gold Standard, Deflation, and Financial Crisis in the Great Depression: An International Comparison". In R. Glenn Hubbard (ed.). Financial markets and financial crises. Chicago: University of Chicago Press. pp. 33–68. ISBN 978-0-226-35588-7. OCLC 231281602.

- Rothbard, Murray Newton (2006). "The World Currency Crisis". Making Economic Sense. Burlingame, California: Ludwig von Mises Institute. pp. 295–299. ISBN 978-0-945466-46-8. OCLC 78624652.

- Cassel, Gustav (1936). The downfall of the gold standard. Oxford: Clarendon Press. OCLC 237252.

- Braga de Macedo, Jorge; Barry J. Eichengreen; Jaime Reis (1996). Currency convertibility: the gold standard and beyond. New York City: Routledge. ISBN 978-0-415-14057-7. OCLC 33132906.

- Russell, William H. (1982). The Deceit of the Gold Standard and of Gold Monetization. American Classical College Press. ISBN 978-0-89266-324-8.

- Mitchell, Wesley C. (1908). Gold, prices, and wages under the greenback standard. Berkeley, California: The University Press. OCLC 1088693.

- Mouré, Kenneth (2002). The gold standard illusion: France, the Bank of France, and the International Gold Standard, 1914–1939. Oxford: Oxford University Press. ISBN 978-0-19-924904-6. OCLC 48544538.

- Bayoumi, Tamim A.; Barry J. Eichengreen and Mark P. Taylor (1996). Modern perspectives on the gold standard. Cambridge: Cambridge University Press. ISBN 978-0-521-57169-2. OCLC 34245103.

- Keynes, John Maynard (1925). The economic consequences of Mr. Churchill. London: Hogarth Press. OCLC 243857880.

- Keynes, John Maynard (1930). A treatise on money in two volumes. London: MacMillan. OCLC 152413612.

- Ferderer, J. Peter (1994). Credibility of the interwar gold standard, uncertainty, and the Great Depression. Annandale-on-Hudson, New York: Jerome Levy Economics Institute. OCLC 31141890.

- Aceña, Pablo Martín; Jaime Reis (2000). Monetary standards in the periphery: paper, silver and gold, 1854–1933. London: Macmillan Press. ISBN 978-0-333-67020-0. OCLC 247963508.

- Gallarotti, Giulio M. (1995). The anatomy of an international monetary regime: the classical gold standard, 1880–1914. Oxford: Oxford University Press. ISBN 978-0-19-508990-5. OCLC 30511110.

- Dick, Trevor J. O.; John E. Floyd (2004). Canada and the Gold Standard: Balance of Payments Adjustment Under Fixed Exchange Rates, 1871–1913. Cambridge: Cambridge University Press. ISBN 978-0-521-61706-2. OCLC 59135525.

- Kenwood, A.G.; A. L. Lougheed (1992). The growth of the international economy 1820–1990. London: Routledge. ISBN 978-91-44-00079-4.

- Hofstadter, Richard (1996). "Free Silver and the Mind of "Coin" Harvey". The Paranoid Style in American Politics and Other Essays. Harvard: Harvard University Press. ISBN 978-0-674-65461-7. OCLC 34772674.

- Lewis, Nathan K. (2006). Gold: The Once and Future Money. New York: Wiley. ISBN 978-0-470-04766-8. OCLC 87151964.

- Withers, Hartley (1919). War-Time Financial Problems. London: J. Murray. OCLC 2458983. Retrieved 2008-11-14.

- Metzler, Mark (2006). Lever of Empire: The International Gold Standard and the Crisis of Liberalism in Prewar Japan. Berkeley, California: University of California Press. p. . ISBN 978-0-520-24420-7.

- Pietrusza, David (2011). 'It Shines for All': The Gold Standard Editorials of The New York Sun. New York City, New York: New York Sun Books. ISBN 978-1-4611-5612-3.

External links

- 1925: Churchill & The Gold Standard - UK Parliament Living Heritage

- What is The Gold Standard? University of Iowa Center for International Finance and Development

- History of the Bank of England Bank of England

- Timeline: Gold's history as a currency standard