Pawnbroker

A pawnbroker is an individual or business (pawnshop or pawn shop) that offers secured loans to people, with items of personal property used as collateral. The items having been pawned to the broker are themselves called pledges or pawns, or simply the collateral. While many items can be pawned, pawnshops typically accept jewelry, musical instruments, home audio equipment, computers, video game systems, coins, gold, silver, televisions, cameras, power tools, firearms, and other relatively valuable items as collateral.

| Personal finance |

|---|

|

| Credit · Debt |

| Employment contract |

| Retirement |

|

| Personal budget and investment |

| See also |

If an item is pawned for a loan (colloquially "hocked" or "popped"[1]), within a certain contractual period of time the pawner may redeem it for the amount of the loan plus some agreed-upon amount for interest. The amount of time, and rate of interest, is governed by law and by the pawnbroker's policies. If the loan is not paid (or extended, if applicable) within the time period, the pawned item will be offered for sale to other customers by the pawnbroker. Unlike other lenders, the pawnbroker does not report the defaulted loan on the customer's credit report, since the pawnbroker has physical possession of the item and may recoup the loan value through outright sale of the item. The pawnbroker also sells items that have been sold outright to them by customers. Some pawnshops are willing to trade items in their shop for items brought to them by customers.

History

In the West, pawnbroking existed in the Ancient Greek and Roman Empires. Most contemporary Western law on the subject is derived from the Roman jurisprudence. As the empire spread its culture, pawnbroking went with it. Likewise, in the East, the business model existed in China 1,500 years ago in Buddhist monasteries no different from today, through the ages strictly regulated by Imperial or other authorities.

In spite of early Roman Catholic Church prohibitions against charging interest on loans, there is some evidence that the Franciscans were permitted to begin the practice as an aid to the poor. [2] In 1338, Edward III pawned his jewels to raise money for his war with France. King Henry V did much the same in 1415. The Lombards were not a popular class, and Henry VII harried them a good deal. In 1603 an Act against Brokers was passed and remained on the statute-book until 1872. It was aimed at the many counterfeit brokers in London. This type of broker was evidently regarded as a fence.

Crusaders, predominantly in France, brokered their land holdings to monasteries and diocese for funds to supply, outfit, and transport their armies to the Holy Land. Instead of outright repayment, the Church reaped a certain amount of crop returns for a certain amount of seasons, which could additionally be re-exchanged in a type of equity.

A pawnbroker can also be a charity. In 1450, Barnaba Manassei, a Franciscan friar, began the Monte di Pietà movement in Perugia, Italy. It provided financial assistance in the form of no-interest loans secured with pawned items. Instead of interest, the Monte di Pietà urged borrowers to make donations to the Church. It spread through Italy, then to other parts of Europe. The first Monte de Piedad organization in Spain was founded in Madrid, and from there the idea was transferred to New Spain by Pedro Romero de Terreros, the Count of Santa Maria de Regla[3] and Knight of Calatrava.[4] The Nacional Monte de Piedad is a charitable institution and pawn shop whose main office is located just off the Zócalo, or main plaza of Mexico City. It was established between 1774 and 1777 by Pedro Romero de Terreros as part of a movement to provide interest-free or low-interest loans to the poor. It was recognized as a national charity in 1927 by the Mexican government.[4] Today it is a fast-growing institution with over 152 branches all over Mexico and with plans to open a branch in every Mexican city.[5]

Business model

Assessment of items

The pawning process begins when a customer brings an item into a pawn shop. Common items pawned (or, in some instances, sold outright) by customers include jewelry, electronics, collectibles, musical instruments, tools, and (depending on local regulations) firearms. Gold, silver, and platinum are popular items—which are often purchased, even if in the form of broken jewelry of little value. Metal can still be sold in bulk to a bullion dealer or smelter for the value by weight of the component metals. Similarly, jewelry that contains genuine gemstones, even if broken or missing pieces, have value.

The pawnbroker assumes the risk that an item might have been stolen. However, laws in many jurisdictions protect both the community and broker from unknowingly handling stolen goods (also known as fencing). These laws often require that the pawnbroker establish positive identification of the seller through photo identification (such as a driver's license or government-issued identity document), as well as a holding period placed on an item purchased by a pawnbroker (to allow time for local law enforcement authorities to track stolen items). In some jurisdictions, pawnshops must give a list of all newly pawned items and any associated serial number to police, so the police can determine if any of the items have been reported stolen. Many police departments advise burglary or robbery victims to visit local pawnshops to see if they can locate stolen items. Some pawnshops set up their own screening criteria to avoid buying stolen property.

The pawnbroker assesses an item for its condition and marketability by testing the item and examining it for flaws, scratches or other damage. Another aspect that affects marketability is the supply and demand for the item in the community or region. In some markets, the used goods market is so flooded with used stereos and car stereos, for example, that pawnshops will only accept the higher-quality brand names. Alternatively, a customer may offer to pawn an item that is difficult to sell, such as a surfboard in an inland region, or a pair of snowshoes in warm-winter regions. The pawnshop owner either turns down hard-to-sell items, or offers a low price. While some items never get outdated, such as hammers and hand saws, electronics and computer items quickly become obsolete and unsaleable. Pawnshop owners must learn about different makes and models of computers, software, and other electronic equipment, so they can value objects accurately.

To assess value of different items, pawnbrokers use guidebooks ("blue books"), catalogs, Internet search engines, and their own experience. Some pawnbrokers have trained in identification of gems, or employ a specialist to assess jewelry. One of the risks of accepting secondhand goods is that the item may be counterfeit. If the item is counterfeit, such as a fake Rolex watch, it may have only a fraction of the value of the genuine item. Once the pawnbroker determines the item is genuine and not likely stolen, and that it is marketable, the pawnbroker offers the customer an amount for it. The customer can either sell the item outright if (as in most cases) the pawnbroker is also a licensed secondhand dealer, or offer the item as collateral on a loan. Most pawnshops are willing to negotiate the amount of the loan with the client.

Determining amount of loan

To determine the amount of the loan, the pawnshop owner needs to take into account several factors. A key factor is the predicted resale value of the item. This is often thought of in terms of a range, with the low point being the wholesale value of the used good, in the case that the pawnshop is unable to sell it to pawnshop customers, and they decide to sell it to a wholesale merchant of used goods. The higher point in the range is the retail sale price in the pawnshop. For example, a five-year-old laptop may have been bought by the customer for $1,000. However, as a used item in a pawnshop, it might only fetch $250 as a purchase price in the pawnshop, because the customers will be wary that it might be a "lemon" that the seller is getting rid of because it has some hard-to-detect problem, and because pawnshops do not typically offer a warranty with goods sold. Used electronics wholesalers will buy the laptop from the pawnshop owner for $100 to $150. The wholesaler pays a lower price than the retail value because they have the added cost of hiring electronics technicians who overhaul and repair the items so that they can be sold in used electronics stores.

The pawnshop owner also takes into account their knowledge of supply and demand for the item in question to determine if they think that they will end up selling the laptop for $100 to a wholesaler or $250 to a pawnshop customer. If the pawnshop owner believes that the local market for used laptops is saturated (overloaded with used laptops), they may fear that they will only get $100 for the laptop if they have to unload it to a wholesaler. With that figure in mind as the expected revenue, the pawnshop owner has to factor in the overhead costs of the store (rent, heat, electricity, phone connection, yellow pages advertisement, website costs, staff costs, insurance, alarm system, items lost when they are confiscated by police, etc.), and a profit for the business. As such, the customer who comes in with this laptop that they paid $1,000 for when it was new may be offered as little as $50 by the pawnshop owner, who is taking into account all of the risk and cost factors.

In determining the amount of the loan, the pawnshop owner also assesses the likelihood that the customer will pay the interest for several weeks or months and then return to repay the loan and reclaim the item. Since the key to the pawnshop business model is earning interest on the loaned money, pawnshop owners want to accept items that the customer is likely to want to recover, after having paid interest for a period on the loan. If, in an extreme case, a pawnshop only accepted items that customers had no interest in ever reclaiming, it would not make any money from interest, and the store would in effect become a second-hand dealer. Determining if the customer is likely to return to reclaim an item is a subjective decision, and the pawnshop owner may take many factors into account. For example, if a young able-bodied man comes into the pawnshop to pawn an electric wheelchair (perhaps claiming it to be the possession of his late grandparent), the pawnshop owner may doubt that the item will be redeemed. On the other hand, if a middle-aged man pawns a top quality set of golf clubs, the pawnshop owner may assess it as more credible that he will return for the items. Some customers may attempt to persuade the pawnshop owner that the item in question is important to them ("that necklace belonged to my grandmother, so I will certainly return for it") as a means of obtaining a loan. Other customers return to the same store, repeatedly pawn the same items as a way of borrowing money, and return to pay the interest and recover the items before the end of the loan period; thus, the pawnbroker knows that redemption is likely and will, therefore, make the loan.

The saleability of the item and the amount that the customer wants for it are also factored into the pawnbroker's assessment; if a customer offers a very salable item at a low price, the pawnbroker may accept it even if it is unlikely that the customer will return, because the pawnshop can turn around a quick profit on the item. However, if a customer offers an extremely low price the pawnbroker may turn down the offer because this suggests that the item may either be counterfeit or stolen.

In some countries such as Sweden, there is legislation to prevent the pawnbroker from making unfair profits (usury due to financial distress or ignorance of the customer) at the expense of the customer by low valuations of their collaterals. It is stated that the pawnbroker may not keep the collateral but must sell them at public auction. Any excess after paying the loan, the interest and auction costs must be paid to the customer. If the item does not fetch a price that will cover these expenses the pawnbroker may keep the item and sell it through other channels. Despite this protection, the cost for the customer to borrow money this way will be high, and if he cannot redeem the collateral it would in many cases be better to sell the goods directly.

Inventory management

Pawnshops have to be careful to manage how many new items they accept as pawns: either too little inventory or too much is bad. A pawnshop might have too little inventory if, for example, it mostly buys jewels and gold that it resells or smelts—or perhaps the pawnshop owner quickly sells most items through specialty shops (e.g., musical instruments to music stores, stereos to used hi-fi audio stores, etc.). In this case, the pawnshop is less interesting to customers, because it is mostly empty.

On the other extreme, a pawnshop with a huge inventory has several disadvantages. If the store is crammed with used athletic gear, old stereos, and old tools, the store owner must spend time and money shelving and sorting items, displaying them on different stands or in glass cases, and monitoring customers to prevent shoplifting. If there are too many low-value, poor quality items, such as old toasters, scratched-up 20-year-old TVs, and worn-out sports gear piled into cardboard boxes, the store may begin to look more like a rummage sale or flea market. Small, high-value items such as iPod players or cell phones must be in locked glass display cases, which means the owner may need additional staff to unlock the cabinets for items customers want to examine. As a store fills with items, an owner must protect inventory from theft by hiring staff to supervise the different areas or install security cameras and alarms. Too much unsold inventory means that the store has not been able to realize value from these items to provide cash to lend.

The better option lies in the middle: a store with a moderate amount of good quality, brand-name items arranged neatly in the display windows attracts passersby, who are more likely to enter and shop. If items are attractively laid out in display cases and shelves, the pawnshop looks more professional and reputable. Once passersby start shopping in the store, they may be more inclined to pawn or sell their own items to the pawnshop. Some pawnshop owners prevent cluttered look by storing overstocked items, or less attractive items such as snow tires, in a backroom or basement. Some pawnshop companies operate a chain of stores in a state or province. This way, they can balance inventory between stores. For example, they can move some of a rural store's surfeit of fishing gear to an urban store.

Some stores also slim down inventory by selling items to speciality retailers. A pawnshop in a low-income neighborhood that pays a customer $300 for a power amplifier with a used value of $2000 may find the unit hard to sell alongside much less expensive merchandise. They may sell the amplifier to a used audio equipment store whose customers expect higher-end equipment. Some pawnshops sell speciality items online, on eBay or other websites. A speciality item such as a high-end model railroad set may not sell in the store for its "blue book" value. On an online auction, it stands a good chance of bringing a good price.

Another growing trend in the industry is vehicle pawn or auto pawning. This form of Pawnbroking works like a traditional pawn loan, however, these stores only accept vehicles as security. Many stores are also accepting "Title Loans", where you can pawn the ownership or "Title" documents of your vehicle. This essentially means that the pawnbroker owns your car while you drive it, and you regain ownership once you pay back your loan.

Auxiliary operations

While the main business activities of a pawnshop are lending money for interest based on valuable items that customers bring in, some pawnshops also undertake other business activities, such as selling brand-new retail items that are in demand in the neighborhood of the store. Depending on where a pawnshop is located, these other retail items may range from musical instruments to firearms. Some pawnbrokers also sell brand-new self-defense items such as pepper spray or stun guns.

Many pawnshops will also trade used items, as long as the transaction turns a profit for pawn shop. In cases where the pawnshop buys items outright, the money is not a loan; it is a straight payment for the item. On sales, the pawnshop may offer layaway plans, subject to conditions (down payment, regular payments, and forfeiture of previously paid amounts if the item is not paid off).

Some pawnshops may keep a few unusual, high value items on display to capture the interests of passersby, such as a vintage Harley Davidson motorcycle; the owner is not typically expecting to sell these items. Other activities carried out by pawnshops are financial services including fee-based check cashing, payday loans, vehicle title or house title loans, and currency exchange services.

Upscale pawnshops

Upscale pawnshops began to appear in the early 20th century, often referred to as "loan offices", since the term “pawn shop” had a very negative historical reputation at this point.[6] Some of these so-called loan offices are even located in the upper floors of office buildings. The modern euphemism for the upscale pawn shop is the "high-end collateral lender",[7] lending to upper-class often white-collar individuals, including doctors, lawyers and bankers, as well as more colorful individuals like high-rolling gamblers.[8] They are also interchangeably called "upscale pawnshops" and "high-end pawnshops" due to their acceptance of higher value merchandise in exchange for short-term loans. These objects can include wine collections, jewelry, large diamonds, fine art, cars, and unique memorabilia. Loans are often sought to deal with business revenue shortfalls and other expensive fiscal issues.[9] Upscale pawnshops have also been featured in reality television

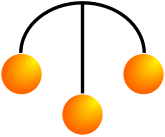

Symbol

The pawnbrokers' symbol is three spheres suspended from a bar. The three sphere symbol is attributed to the Medici family of Florence, Italy, owing to its symbolic meaning of Lombard. This refers to the Italian region of Lombardy, where pawn shop banking originated under the name of Lombard banking. It has been conjectured that the golden spheres were originally three flat yellow effigies of bezants, or gold coins, laid heraldically upon a sable field, but that they were converted into spheres to better attract attention.

Most European towns called the pawn shop the "Lombard". The Lombards were a banking community in medieval London, England. According to legend, a Medici employed by Charlemagne slew a giant using three bags of rocks. The three-ball symbol became the family crest. Since the Medicis were so successful in the financial, banking, and moneylending industries, other families also adopted the symbol. Throughout the Middle Ages, coats of arms bore three balls, orbs, plates, discs, coins and more as symbols of monetary success.

Saint Nicholas is the patron saint of pawnbrokers. The symbol has also been attributed to the story of Nicholas giving a poor man's three daughters each a bag of gold so they could get married.[12]

In Asia

In Hong Kong the practice follows the Chinese tradition, and the counter of the shop is typically higher than the average person for security. A customer can only hold up his hand to offer belongings and there is a wooden screen between the door and the counter for customers' privacy. The symbol of a pawn shop in Hong Kong is a bat holding a coin (Chinese: 蝠鼠吊金錢, Cantonese: fūk syú diu gām chín). The bat signifies fortune and the coin signifies benefits. In Japan, the usual symbol for a pawn shop is a circled number seven (7) because "shichi", the Japanese word for seven, sounds similar to the word for "pawn" (質).

The majority of pawnbrokers in Malaysia, a multi-race country wherein Malaysian Chinese consists 25% of the population, are managed by Malaysian Chinese. In Malay, pawn is called "pajak gadai". A valid and licensed pawnshop in Malaysia must always declare themselves as a "pajak gadai" or a pawn shop for their company registration. They must also fulfill the requirements of the Ministry of Housing and Local Government which states the pawn counter must not be higher than 4 feet, is bullet-proof, has stainless-steel counters/doors, strong rooms with automatic locks, safes, equipped with fully computerized system, CCTV, alarm, and pawnbroker insurance.

In the Philippines, pawnshops are generally privately-owned businesses and are regulated by the Bangko Sentral ng Pilipinas (BSP). Pawnshops in the country traditionally have Spanish names beginning with "Agencia de Empeños" (lit. "Pawn agency"), contrary to "Casa de Empeños" in Spain and Latin America.[13] Most pawnshops accept jewelry, vehicles or electronic valuables as collateral. They also offer various forms of other finance-related services such as remittance, bills payment and microfinancing. Therefore, they serve as financial one stop shops primarily to communities in which alternatives such as banks are not available. Recently, they have also started conducting services online and through mobile applications although this is yet subject to regulation by the BSP.

In India, the Marwari Jain community pioneered the pawnbroking business, but today others are involved; the work is done by many agents called "saudagar". Instead of working from a shop, they go to needy people's homes and motivate them to become involved in the business. Pawn shops are often run as part of jewelry stores. Gold, silver, and diamonds are frequently accepted as collateral.

Pawnbroking is also a traditional trade in Thailand, where pawn shops are run both privately and by local governments.

In Sri Lanka, pawnbroking is a lucrative business engaged in by specialized pawnbrokers as well as commercial banks and other finance companies.

In Indonesia, there is a state-owned company called Pegadaian which provides a range of conventional and Sharia-compliant pawnbroking services across the archipelago. The company accepts high-value items such as gold, motor vehicles, and other expensive items as collateral. In addition to pawnbroking activities, the company provides a range of other services, such as a safe deposit box and gold trading services.

See also

- Consignment shop

- Lombard banking

- Wilson v First County Trust Ltd (No 2) [2003] UKHL 40, [2004] 1 AC 816

- In April 2011, the VOA Special English service of the Voice of America broadcast a 15-minute program on pawnbrokers. A transcript and MP3 of the program, intended for English learners, can be found at Voice of America website.[14]

References

- "pop". Oxford English Dictionary (3rd ed.). Oxford University Press. September 2005. (Subscription or UK public library membership required.)

- Gregg, Samuel (2016). "How Medieval Monks Changed the Face of Banking". American Banker. 1 no. 88 – via EBSCOhost.

- Leon Teutli Ficachi. "Nacional Monte de Piedad" (PDF). Archived from the original (PDF) on December 19, 2008. Retrieved 2008-10-01.

- Alvarez, Jose Rogelio (2000). "Nacional Piedad de Monte". Enciclopedia de Mexico. 10. Mexico City: Encyclopædia Britannica. pp. 5699–5701. ISBN 1-56409-034-5.

- Notimex. "Dispone Monte de Piedad de 905 mdp para préstamos" (in Spanish). Torreón: El siglo de Torreón. Retrieved 2008-10-01.

- Wendy A. Woloson (2009). In Hock: Pawning in America from Independence through the Great Depression. University of Chicago Press. p. 66 and 70–72. ISBN 9780226905693. Retrieved July 11, 2013.

upscale pawnshops.

- "Pawn Shops for the (Formerly) Rich". Wall Street Journal. September 28, 2010. Retrieved July 11, 2013.

- Sally Brown and David R. Brown (2011). A Biography of Mrs. Marty Mann: The First Lady of Alcoholics Anonymous. Hazelden Publishing. p. 51. ISBN 9781616491413. Retrieved July 11, 2013.

- Russ Wiles (July 15, 2012). "Pawn shops are going upscale for affluent clients". USA Today. Retrieved July 11, 2013.

- "U.S. Pawn Shops Industry Sails Through The Recession". prweb.com. Cision. Retrieved 2 February 2016.

- "Pawn Industry Statistics". nationalpawnbrokers.org. National Pawn Brokers Association. Retrieved 2 February 2016.

- Archived February 2, 2013, at the Wayback Machine

- "Official Gazette, Vol. 1". Official Gazette (Philippines). Philippine Executive Commission. 1942.

- "Inside the World of Pawn Shops". Voanews.com. 2011-04-17. Retrieved 2013-04-28.

| Wikimedia Commons has media related to Pawnbrokers. |

| Authority control |

|

|---|