Efficient frontier

In modern portfolio theory, the efficient frontier (or portfolio frontier) is an investment portfolio which occupies the 'efficient' parts of the risk-return spectrum. Formally, it is the set of portfolios which satisfy the condition that no other portfolio exists with a higher expected return but with the same standard deviation of return (i.e., the risk).[1][2] The efficient frontier was first formulated by Harry Markowitz in 1952;[3] see Markowitz model.

Overview

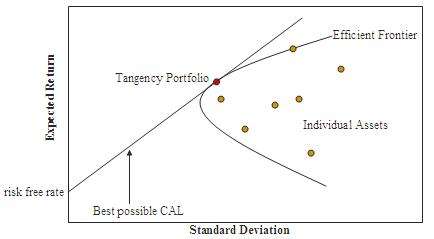

A combination of assets, i.e. a portfolio, is referred to as "efficient" if it has the best possible expected level of return for its level of risk (which is represented by the standard deviation of the portfolio's return).[4] Here, every possible combination of risky assets can be plotted in risk–expected return space, and the collection of all such possible portfolios defines a region in this space. In the absence of the opportunity to hold a risk-free asset, this region is the opportunity set (the feasible set). The positively sloped (upward-sloped) top boundary of this region is a portion of a hyperbola[5] and is called the "efficient frontier".

If a risk-free asset is also available, the opportunity set is larger, and its upper boundary, the efficient frontier, is a straight line segment emanating from the vertical axis at the value of the risk-free asset's return and tangent to the risky-assets-only opportunity set. All portfolios between the risk-free asset and the tangency portfolio are portfolios composed of risk-free assets and the tangency portfolio, while all portfolios on the linear frontier above and to the right of the tangency portfolio are generated by borrowing at the risk-free rate and investing the proceeds into the tangency portfolio.

See also

- Markowitz model

- Modern portfolio theory

- Critical line method, an optimization algorithm developed by Markowitz for this problem

References

- "Efficient Frontier". Investopedia. investopedia.com. Retrieved 15 May 2017.

- "Markowitz efficient frontier". NASDAQ. nasdaq.com. Retrieved 15 May 2017.

- Markowitz, H.M. (March 1952). "Portfolio Selection". The Journal of Finance. 7 (1): 77–91. doi:10.2307/2975974. JSTOR 2975974.

- Edwin J. Elton and Martin J. Gruber (2011). Investments and Portfolio Performance. World Scientific. pp. 382–383. ISBN 978-981-4335-39-3.

- Merton, Robert. "An analytic derivation of the efficient portfolio frontier," Journal of Financial and Quantitative Analysis 7, September 1972, 1851-1872.