Banking crisis

A banking crisis usually refers to a situation in a general "market adjustment"[note 1] when faith in banking institutions falls, and people start trying to move their money to other places for safe keeping. This is called a "run on the banks". It can also occur due to overextending low quality loans, which in a down market can become essentially worthless.

| The dismal science Economics |

| Economic Systems |

|

$ Market Economy |

| Major Concepts |

| People |

|

v - t - e |

| How the sausage is made Politics |

| Theory |

| Practice |

| Philosophies |

| Terms |

| As usual |

| Country sections |

|

v - t - e |

Economies around the world have suffered financial crises for centuries. Afterwards, politicians boast of newly-adopted regulation that will minimize the risk of a future crash. But such claims are rarely borne out by experience.

One of the most famous banking crises in modern history occurred during the Great Depression, which only massive government intervention and guarantees (mostly in World War II) were able to turn around.

Notable historical banking crises

The South Sea Company (1711-1720)

Although not well known today, the South Sea Company is a prime example of just how crazy things can get. Originally set up as a public–private partnership to consolidate and reduce the cost of Britain's national debt, it was marketed to the general public as a trading company that in theory would equal or surpass the Dutch East India Company in terms of profits. In reality, the company NEVER made a profit in trading. The way the company made money was to hype the stock price and use various financial tricks to keep the stock rising. But 1720 is the year when things went insane as the stock went from a low of £128 in January to £1050 by June, making the company worth 10 times the debt it had originally been set up to manage. To put that in perspective, a comparable situation would be if in 2015 there was one US company whose stock was worth $186 trillion on the NYSE. It had gotten to the point in 1720 where the South Sea Company was lending people money to buy stock to keep the ball rolling. Of course, that type of hype cannot be sustained and the stock eventually fell, hitting £175 by September. As for the debt, the company was supposed to consolidate and reduce this; in 2014 the Chancellor of the Exchequer (equivalent of the US Department of Treasury) announced that it would be paying off that debt[1]. To put that in perspective, the United States paid off its national debt (from 1776 onwards) in 1835.

Panic of 1907

Most[note 2] agree the banking panic of 1907 forged a consensus of the need for banking regulation and a central bank in the United States.[2][3] This led to creation of the Federal Reserve in 1916 to oversee banks and serve as a lender of last resort in times of a cash crunch (or more formally, "liquidity crisis").

Black Tuesday

By 1930 there were approximately 30,000 banks in the United States. Most of these were mom 'n pop, unregulated neighborhood banks.[4] When the Crash of 1929 occurred, unemployment and foreclosures began to rise.[note 3] Some people needed to withdraw their savings from these banks, only to find the bank didn't have the cash in the vault and was holding worthless paper loans on defunct businesses that laid everyone off, or foreclosed real estate that had sunk in value with no market buyers.

In February 1932 the governor of Michigan declared a banking holiday throughout the state. This sent a tremor throughout the country. Rumors of inflation and going off the gold standard flooded the country, leading to more withdrawal of gold from the banks. Foreign depositors began withdrawing balances which set in motion an increased flow of gold out of the country. By inauguration day of the new president twenty-one states had closed their banks.

President Franklin Roosevelt's first act was to declare a bank holiday. After three days of re-organization and mergers, when the banks re-opened, fewer than half survived. Fractional-reserve banking was implemented with regulatory oversight by the Federal Reserve mandating reserve requirements (a portion of bank deposits held in cash reserve). Banks were also required to purchase deposit insurance to rebuild bank customers confidence with FDIC bailout gaurantees. Other reforms followed such as the Glass-Steagall Act

Great Recession

“”You couldn't advance in a finance department in this country unless you taught that the world was flat. |

| —Warren Buffett on the "efficient" market paradigm (back in 2005[5]) |

This newest recession was caused by the subprime mortgage crisis in 2007. It left many people devastated, purchase power decreased and people lost their savings. That recession combined with waves of refugees contributed to the rise of populism in Europe and United States.

The great recession presented the perfect opportunity for goldbuggery consolidation and buying up competing businesses and assets that were performing poorly due to the recession. It produced the most bubbalicious form of economy, and in the ten years that followed we've learned absolutely nothing from it except that we won't rise up to stop the bankers next time.

{kind=link}

Credit default swaps

The Commodity Futures Modernization Act of 2000

On top of this, the de facto repeal of the Glass-Steagall Act in 1999 presented investment banks with the spectre of competition from much larger, much stabler, much more richly capitalised commercial banks.[7] Many investment banks responded by embracing greater risk and increasing levels of leverage in order to maximise income from market sources that commercial bank regulations prohibited commercial banks from entering.

The main "writers" of credit default swaps were large insurance companies, asked by investment banks around the world, who were securitizing much of the newly created "sub-prime" loans. The end result was that the true risk of lower-quality borrowers was held by individuals and institutions who had not evaluated, and were not aware of the risks. Because of the Gaussian[note 4] copula formula,[8] and a belief that the various securitizations were not correlated, the least-risky tranches[9] of securitizations were packaged together and sold via CDS to these insurance companies, who believed them to be almost riskless.

Because state regulators were not requiring insurers to retain enough in reserve, AIG underwrote over $3 trillion (to compare, more than the entire GDPs of India, France or the UK at the time) worth of these derivatives. And these default swaps, of course, were purchased by holders of crappy loan bundles (mainly Goldman Sachs, in the case of AIG) as insurance against a system-wide shock. The unintended consequence was that the limited number of large firms (notably AIG) that issued credit default swaps managed to re-concentrate much of the risk that securitization had theoretically distributed throughout the economy — on their own balance sheets.

Relationship to the War on Terror

George Friedman writes in The Next Decade, "The Bush Administration didn't want to raise taxes to pay for the war on terror, and Fed cooperated by financing the war by, essentially, lending money to the government. The result was that no one felt the war's economic impact - at least not right away." Low interest rates encouraged home buying and increasingly "sub-prime" loans, some with adjustable mortgage rates. The war in Iraq went badly,[citation NOT needed] and the Fed never got around to raising rates.[10]

Beginning to fall apart

As mortgage rates on adjustable rate mortgages rose and individual borrowers were unable to make payments on their loans after the expiry of teaser rates and other features, default rates in securities began to rise and repossessed houses began to flood the market. Noticing this, a number of market participants tried to get "short" of the housing market, creating even more demand for CDS, but now based not on insuring actual housing risk, but just making bets.

The system was set to correct itself, and did so in late 2007 and 2008. Spreads on housing risk indices increased dramatically as expected losses rose, and a number of large market participants who had large, leveraged bets on the continued housing boom began to fail, from structured investment vehicles (designed as a rating-arbitrage vehicle) to derivatives products companies (a purely-synthetic high-leveraged vehicle) failed first, but were shortly followed by a number of housing-related hedge funds.

It's a TARP!

By the fall of 2008, the US government was struggling to prevent the all-out collapse of the financial system, and eventually settled on an undersized $700 billion rescue package[note 5] to try to tackle the crisis before the US economy (and by extension, the entire world) froze into a second dark age. The original draft pursued by the Bush administration was 3 pages that included a non-reviewable provision,[11] but grew to 451 pages. It passed with House Democrats' help on September 29.[12]

Later, it was revealed that the added 448 pages weren't enough to stop AIG from drenching themselves with undeserved bonus money.[13] (Because the devil's advocate never dies, there were some in the media who believed the outrage was all a bunch of populist claptrap.[note 6])

If that was tl;dr...

Here's a four minute summary:

Casualties of the crisis

“”The foreclosure rate is the worst since the Great Depression, [but] it's spurious to evoke memories of that great national calamity when talking about today — it's akin to equating a sore throat with stomach cancer... Whatever the political outcome this year, hopefully this will prove to be yet another instance of that iron law of economics and markets: The sentiment of the majority is always wrong at key turning points. And the majority is plenty pessimistic right now. That suggests that we're on the brink not of recession, but of accelerating prosperity. |

| —Donald Luskin, NRO columnist and author of I am John Galt, on Sept. 14, 2008[14] |

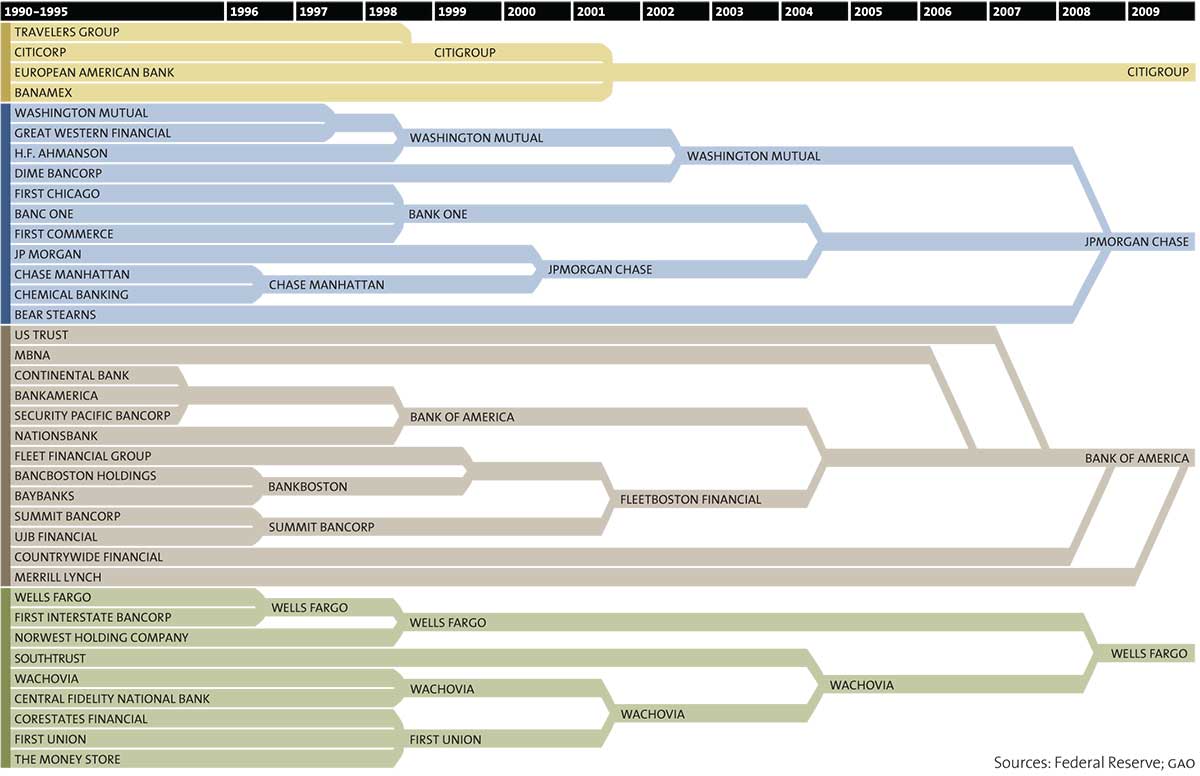

As the losses started to mount, many banks faced hard times. Some collapsed, some were nationalized, some were swallowed up by larger rivals, and others needed government bailouts. At the end of September 2008, over 284 banks and lenders worldwide had collapsed, the largest ones being:

- Northern Rock - A large British bank and mortgage lender, Northern Rock had a business model where it borrowed money from larger banks in order to extend mortgages to its borrowers. When the markets lost liquidity, it borrowed £25 billion from the Bank of England, but even this failed to save it. Eventually on February 17, the UK government had to nationalize the bank, leaving thousands of shareholders with nothing and costing 2000 jobs.[15]

- Bear Stearns - One of the first to appeal to the US government for help, Bear Stearns was propped up by the US government and eventually sold to JP Morgan on March 17.[16]

- Dresdner Kleinwort - German investment bank taken over by Commerzbank AG. 31 August.[17]

- Fannie Mae and Freddie Mac - The two largest US mortgage lenders were taken over by the US government, except on a much larger scale. The two government-sponsored enterprises, which guarantee about half of the US mortgage market (worth a cool $12 trillion) were placed in conservatorship on September 7, costing the federal government a potential $200 billion.[18]

- Lehman Brothers

File:Wikipedia's W.svg - It begins. Up to the credit crunch, Lehman was the fourth largest investment bank in the US, but on September 15 it fell victim to the crisis and filed for Chapter 11 bankruptcy protection. Previously, it had approached the Korean Investment Corporation for backing, who wisely walked away when it became clear how exposed Lehman were to the crisis. Thousands of jobs were lost, although UK bank Barclays picked up some of the US assets.[19][note 7] - Merrill Lynch - Another major investment bank, Merrill Lynch actively sought to be taken over by Bank of America in order to prevent its own collapse (Merrill had already written off $50 billion due to sub-prime losses, and had failed to secure overseas investment). The deal was worth a bargain basement $50 billion. 15 September.[20]

- American International Group (AIG) - The biggest insurance group in the US, AIG was rescued by the US Federal Reserve to the tune of $85 billion, effectively nationalizing the company. 16 September.[21]

- Halifax Bank of Scotland (HBOS) - The UK's largest mortgage lender, HBOS, came under scrutiny from investors, concerned at its exposure to the slowdown in the UK market. As a result, its shares plummeted and it was taken over by rival bank Lloyds TSB on September 18 in a deal worth only £12 billion. Such a takeover would have been impossible before the credit crunch, as UK competition laws would have prevented a merger of two of the largest UK banks.[22]

- Washington Mutual - On September 25, WaMu (the self-professed "Wal-Mart of Banking") was closed by its regulators and sold to JP Morgan for a pocket-change amount of $1.9 billion. With assets of $307 billion it was the largest bank to fail to date, and its acquisition by JP Morgan meant that the latter is now the second largest bank in the US.[23]

- Bradford & Bingley - Mortgages from B&B placed into public ownership by the British government on September 29, while the bank's £20 billion in savings deposits, 2.7 million customers and its 197 branches were sold to Spanish bank Santander, who also bought up the struggling Alliance and Leicester bank.[24]

- Fortis - One of the largest banks in the Low Countries. Rescued and part nationalized by Belgium, the Netherlands and Luxembourg. 29 September.[25]

- Wachovia - Bought out by Citigroup. 29 September.[26] However, Wells Fargo outbid Citigroup, acquired Wachovia on December 31 and converted it to Wells Fargo.[27]

- Glitnir - Icelandic bank nationalized. 29 September.[28]

- Hypo Real Estate - German bank bailed out by German government. 29 September.[29]

- Dexia - Belgian bank bailed out by Belgium, France and Luxembourg. 30 September.[30]

- The nation of Iceland? 6 October.[31]

- Landsbanki - Icelandic bank bailed out by Russian funds, 8 October. Refuses to recognize deposits by foreign nationals.[32]

- Yamato Life - The first Japanese victim of the crisis, insurance company Yamato Life went bankrupt on October 10.[33]

- You and me. 'Nuff said.

RationalWiki's hot tip for shares to short-sell now

- HSBC (Hongkong and Shanghai Banking Corporation) - You heard it here first. Update 26/09/08[34]

It's official, we're worse than Jim Cramer

If you actually took our advice, well... sucks to be you, fucker!

The moral of this story

Deregulation in one part of the economy has had far reaching consequences, causing a global slowdown in the money markets and a knock on effect to consumers. It has treated us to the somewhat bizarre spectacle of a particularly right-wing Republican government nationalizing vast swathes of the American economy, to the point where the United States government now not only owns about half of the mortgaged properties in the US, but also is in the business of insuring against defaults on those very same properties — a potential "double-whammy" of monstrous proportions. At this juncture, the slinging about of phrases like "house of cards" might not be considered inappropriate.

Let's make it bleeding obvious

“”[We have] an ideological fixation with free markets and lack of regulation...obviously, people missed the boat on a lot of the risks that a lot of financial instruments entailed. |

| —Stephen J. Kobrin[35] |

Free market libertarianism didn't work. Keynesian policies enacted since the Great Depression prevented what used to be a common occurrence in "free markets" — disastrous contractions which created extreme hardship — even though the market players and their political tools continue to try to break things, most notably via supply side economics and deregulation of financial institutions.[36]

The Republican cover story

“”No believer in the free market can think that bankers have to be told by government bureaucrats to go out and make money. |

| —Dean Baker[37] |

In December 2010, the Financial Crisis Inquiry Commission released its report to Congress, and "there was a virtually unanimous, critical reaction: the report said little new."[38] However, during the process of writing the report, the GOP broke off from the rest of the commission and released their own report, putting wingnut talking points into the record: They excised words like "Wall Street," "deregulation," and "shadow banking system." The official alternate-universe narrative is as follows: "Democrats, especially Bawney Fwank, blocked new regulations[note 8] on Fannie Mae and Freddie Mac, which forced them to loan to po' black hispanic people.[note 9] They were forced to make these bad loans because of the Community Reinvestment Act, passed by the dastardly Jimmy Carter. Democrats did it, gummint bad, gummint bad, gummint bad, Reagan smash!"

Fannie and Freddie did buy up and repackage a lot of bullshit loans, yet it's completely absurd to put the blame for a global financial crisis entirely on them. And the CRA as well — nobody is quite sure how a law passed under Carter (revised in the early 90s) could be responsible for a housing bubble in the mid-2000s.[39][40] Fannie and Freddie actually stepped out during the peak of the housing bubble due to accounting fraud charges and then joined in on the fun buying up shitty loans after Wall Street had eaten away their market share.[41][42][43] But at least "Fannie and Freddie weren't guaranteeing loans in Latvia."[44] Both claims have effectively become PRATTs for economists.[45]

Adding further insult to injury, see the completely ravaged, horrific commie wreck of an economy only a few kilometers north, eh.[46][47][48]

As yet unannounced

Right now, the global financial system is playing a game of Jenga. Once you start removing bricks, it becomes more and more unstable, until finally, a brick crucial to the stack is removed. This can happen for any number of reasons.

Some experts believe that the cause for the next crash will be stock equities, since there's a disconnect between stock prices and quarterly earnings.[49] That might convince investors to cash in, causing a panic as the prices drop more, causing more investors to cash in, and so on.

But since the oligarchs are playing Jenga, that only makes it a possible culprit. Another is the so-called "shadow banking" industry (every bank is connected to each other through loans we can't see), which is subject to fewer regulations. Another is China's deflating real estate and securities markets.[50] It could happen because a TBTF bank takes on outsized risk based on bailout guarantees,[51] causing a bank run, causing a crash.

See also

- IBGYBG

- Too big to fail

- The British term for a group of bankers is a "wunch"

External links

- The Banking Crisis: Causes, Consequences, and Remedies, Paul De Grauwe

- Inside Job, essentially the crisis for dummies. Won Best Documentary Feature at the 83rd Academy Awards.

- From financial market deregulation to fragmentation: Ladies and gentlemen, you screwed up, OECD

- The great story, Columbia Journalism Review

- The Fed’s Actions in 2008: What the Transcripts Reveal, The New York Times (How the fuck does Richard Fisher still have a job?[52])

- Why Can’t the Banking Industry Solve Its Ethics Problems?, The New York Times

Notes

- In many cases (notably 1929 and 2008), this is rather like calling nuclear warfare an "exchange of hostilities".

- But don't forget the Austrians.

- The failure of Austria's Credit-Anstalt

File:Wikipedia's W.svg in 1931 was the first in a wave of international banking crisis which further unsettled Wall Street after the Crash of '29. - Aka, "normal"; "Gaussian" is the alternate name for the normal distribution, and only used to make you look smarter than you are. The first warning sign...

- Equal to about one quarter of all federal outlays at the time, and $200 billion more than the balance sheet of the Federal Reserve Board, which would have to purchase the new government debt from the U.S. Treasury.

- It's on Wikipedia if you want to torture yourself.

- Incidentally, George Herbert Walker IV

File:Wikipedia's W.svg was Investment Management Director at the time. - Really. They prided themselves on government regulation.

- The racism here might seem latent, but take a look at this Byron York interview. Shorter York: Poor black people diddit. And for further debunking of this point, and some more racism by Neil Cavuto, see this article in McClatchy, and, oh yeah, can't forget Ann Coulter: "They Gave Your Mortgage To A Less Qualified Minority!"

References

- STEPHEN CASTLE (DEC. 27, 2014) "That Debt From 1720? Britain’s Payment Is Coming" New York Times

- Milton R. Friedman. "Origin of the Federal Reserve System", Free to Choose. San Diego: Harcourt, 1980.

- Eric Dinallo, Testimony to Congress, November 2008 on (Naked) Credit Default Swaps: "A more lasting result was passage of New York’s anti-bucket shop law in 1909. The law, General Business Law Section 351, made it a felony to operate or be connected with a bucket shop or 'fake exchange' …Section 351 prohibits the making or offering of a purchase or sale of security, commodity, debt, property, options, bonds, etc. without intending a bona fide purchase or sale of the security, commodity, debt, property, options, bonds, etc. If you think that sounds exactly like a naked credit default swap, you are right."

- James Stuart Olson. Historical Dictionary of the Great Depression, 1929-1940. Santa Barbara: Greenwood Publishing Group, 2001.

- The Heresy That Made Them Rich, The New York Times

- Clinton: I Was Wrong to Listen to Wrong Advice Against Regulating Derivatives, ABC News (Larry Summers was then appointed by Barack Obama as Director of the President's National Economic Council.)

- Repeal of Glass-Steagall: Not a cause, but a multiplier, The Washington Post

- The Real—and Simple—Equation That Killed Wall Street, Scientific American

- Tranches on Investopedia

- Friedman, George, 2011. The Next Decade. New York, Doubleday. P. 42. ISBN 978-0-385-53294-5

- Fuck off, Henry Paulson

- Bailout Plan Wins Approval; Democrats Vow Tighter Rules, The New York Times

- AIG's Bonuses: A Dangerous Failure of Leadership, Harvard Business Review

- The whole thing is spectacular. (John McCain really knew how to pick 'em.)

- Timeline: Northern Rock bank crisis, BBC

- JP Morgan Pays $2 a Share for Bear Stearns, The New York Times

- Germany's Commerzbank Agrees to Buy Dresdner, Deutsche Welle

- Nobody Panic: Government Seizes Freddie Mac, Fannie Mae, The Consumerist

- Barclays to buy Lehman Brothers assets, The Guardian

- How Merrill Lynch bankers helped blow up their own firm, NBC

- U.S. to Take Over AIG in $85 Billion Bailout; Central Banks Inject Cash as Credit Dries Up, Wall Street Journal

- HBOS falls to Lloyds in £12 billion deal, The New York Times

- Regulator sells Washington Mutual, BBC

- Santander buys Bradford & Bingley's branches, The Telegraph

- Timeline of Fortis downfall, Financial Times

- Citigroup buys Wachovia bank assets for $2.2B, CNN

- Wells Fargo completes Wachovia purchase, Reuters

- Timeline of the Icelandic Financial Crisis, Iceland Chamber of Commerce

- Hypo Real Estate to Get EU35 Billion Bailout From State, Banks, Bloomberg

- EU approves Dexia bailout, The New York Times

- The party's over for Iceland, the island that tried to buy the world, The Guardian

- Britain to compensate Iceland bank savers, RTE

- Fear grips global stock markets, BBC

- Bank giant HSBC axes 1,100 jobs, BBC

- Why Economists Failed to Predict the Financial Crisis, University of Pennsylvania

- "It's Bozo the Clown's Fault", HuffPo

- The Blame the Community Reinvestment Act Industry, Beat the Press

- The Private Sector Failed, The Atlantic

- Debunking the CRA Myth – Again, University of North Carolina

- The Effectiveness of the Community Reinvestment Act, Congressional Research Service

- The Current Financial Crisis: Causes and Policy Issues, OECD

- The housing meltdown: Why did it happen in the United States?, Bank for International Settlements (The good stuff is on p. 5-15.)

- Understanding the Boom and Bust in Nonprime Mortgage Lending, Harvard JCHS (The good stuff is on p. 103-112.)

- Krugman being snarky

- Fannie and Freddie: guilty?, The Economist

- Contrasting Canadian and U.S. banking, regulation, Maclean's

- Why Canada Avoids Banking Crises, Barry Ritholtz

- Come on, ING, lighten up a bit.

- Authers, John, "Fears grow over US stock market bubble", Financial Times via MSNBC (9/14/15 at 6:12 AM ET).

- Balding, Christopher, "The Shadow Looming Over China", Bloomberg (6/6/16 at 6:00 PM EDT).

- Dayen, Daniel, "Big Bank 'Living Wills' Are a Failure — and Point to a Bigger Problem", Fiscal Times 4.15.16.

- One take