Student loan default in the United States

Defaulting on a student loan in the United States can have a number of negative consequences. To understand loan default, it is helpful to have a few common terms defined:

- Loan deferment is a postponement of a loan's repayment. There are many reasons why someone might seek to defer a loan, including a return to school, economic hardship, or unemployment.

- Loan delinquency is a failure to make loan payments when they are due. Extended delinquency can result in loan default.

- Loan default is the failure to repay a loan according to the terms agreed to in the promissory note. A lender may take legal action to get the money back.[1]

Consequences

Defaulting on a loan can adversely affect credit for many years. Default typically occurs when a loan receives no payment for 270 days. The loan leaves repayment status and is due in full when the lender requests. New collection costs are added to the loan's balance and the loan becomes drastically more expensive or eliminated through negotiation or legal action.

There are other negative consequences resulting from a defaulted loan. A student who wishes to return to school cannot qualify for federal aid in the United States until satisfactory payment arrangements are made on the defaulted loan or the loan is rehabilitated, a process that can take as long as a full year of on-time payments.[2]

Individuals who are worried that they are unable to service their student loan debt should receive advice and counseling. There are few options available for American students other than payment in full. The Bankruptcy Abuse Prevention and Consumer Protection Act makes discharging student loans through bankruptcy virtually impossible. Critics have noted that this lack of bankruptcy protection for consumers results in a "risk-free" loan for creditors, removing pressure on creditors to negotiate lower payments.

Garnishment of wages and tax refund

In addition, the IRS can take the borrower's income tax refund until the defaulted loan is paid in full.[3] This is a popular way of collecting on loan debt, and the Department of Education collects hundreds of millions of dollars this way.

To object, a written statement must be presented within 65 days of the IRS' notice, and must give evidence of any of the following:

- The loan has been repaid.

- Payments have been made under a negotiated repayment agreement, or a cancellation, deferment or forbearance has been granted.

- The borrower has filed for bankruptcy.

- The borrower is totally and permanently disabled.

- The loan in question is not the borrower's loan.

- The borrower dropped out of school and the school owes a refund.

- The borrower attended a trade school and the school closed.

- The school falsely certified the borrower as being eligible for a loan.

The government can also garnish wages as a way to recover money owed on a defaulted student loan. The United States Department of Education or a Student Loan Guarantor can garnish 15%[4] of a defaulted borrower's wages. The loan holder does not have to sue the borrower first. The borrower can object to the garnishment, but only under very specific circumstances, such as if his weekly gross income is less than or equivalent to 30 hours at the federal minimum wage (currently $7.25/hr x 30 hrs = $217.50).

Defaulting on student loans can also end in a lawsuit. The government and private lenders can sue in order to collect on loans. There is no time limit on suing to collect on federal student loans, and the borrower can be sued indefinitely. Private student loans, in most cases, are subject to statute of limitations laws depending on the state.

Getting out of default

There are rehabilitation programs designed to help borrowers get out of debt. Rehabilitation is a federally mandated program that gives federal student loan borrowers a way to bring their loans out of default. Rehabilitation can reverse the many negative consequences of defaulting on a student loan, and participation is one of the few rights granted to federal education loan borrowers.[2]

In the rehabilitation program, a borrower must do a number of things. He or she must make at least 9 qualifying, on-time student loan payments. If any payments are missed, the borrower must begin the repayment schedule from the beginning. After borrowers complete the agreement, the guarantor transfers the loan to a lender and servicer. The default status will be removed from your loan. You will regain eligibility for benefits that were available on the loan before you defaulted, such as deferment, forbearance, a choice of repayment plans, and loan forgiveness, and you will be eligible to receive additional federal student aid.[5]

Rehabilitation benefits

After completing loan rehabilitation, borrowers once again become eligible to receive financial aid. With the loan no longer in default, wage garnishment and the seizure of tax refunds ceases. Borrowers are able to apply for deferment and forbearance benefits as long as these have not been exhausted during default. And lastly, the outstanding balance of the loan is no longer due in full.[6]

Default prevention initiatives

Several new initiatives have arisen to combat high student loan cohort default rates, including an outreach effort by the Department of Education to borrowers struggling to repay their loans.[7]

Debt levels

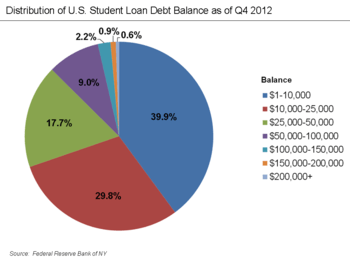

The Economist reported in June 2014 that U.S. student loan debt exceeded $1.2 trillion, with over 8 million debtors in default. Public universities increased their fees by a total of 27% over the five years ending in 2012, or 20% adjusted for inflation. Public university students paid an average of almost $8,400 annually for in-state tuition, with out-of-state students paying more than $19,000. For two decades ending in 2013, college costs have risen 1.6% more than inflation each year. Government funding per student fell 27% between 2007 and 2012. Student enrollments rose from 15.2 million in 1999 to 20.4 million in 2011, but fell 2% in 2012.[8][9]

See also

References

- "Student Loans for College - Stafford, PLUS, Perkins".

- "American Student Assistance".

- "Student Loan Resources: Lenders, Rehabilitation and Consolidation". DIY Credit Repair.

- "American Student Assistance".

- "Getting Out of Default". 24 October 2017.

- "Managing Default". American Student Assistance. Retrieved 2 February 2015.

- Lewin, Tamar (24 September 2013). "U.S. to Contact Borrowers With New Options for Repaying Student Loans" – via NYTimes.com.

- "Creative destruction". The Economist.

- "The digital degree". The Economist.