Roth IRA

A Roth IRA is an individual retirement account (IRA) under United States law that is generally not taxed upon distribution, provided certain conditions are met. The principal difference between Roth IRAs and most other tax-advantaged retirement plans is that rather than granting a tax reduction for contributions to the retirement plan, qualified withdrawals from the Roth IRA plan are tax-free, and growth in the account is tax-free.

The Roth IRA was introduced as part of the Taxpayer Relief Act of 1997 and is named for Senator William Roth.

Overview

A Roth IRA can be an individual retirement account containing investments in securities, usually common stocks and bonds, often through mutual funds (although other investments, including derivatives, notes, certificates of deposit, and real estate are possible). A Roth IRA can also be an individual retirement annuity, which is an annuity contract or an endowment contract purchased from a life insurance company. As with all IRAs, the Internal Revenue Service mandates specific eligibility and filing status requirements. A Roth IRA's main advantages are its tax structure and the additional flexibility that this tax structure provides. Also, there are fewer restrictions on the investments that can be made in the plan than many other tax-advantaged plans, and this adds somewhat to their popularity, though the investment options available depend on the trustee (or the place where the plan is established).

The total contributions allowed per year to all IRAs is the lesser of one's taxable compensation (which is not the same as adjusted gross income) and the limit amounts as seen below (this total may be split up between any number of traditional and Roth IRAs. In the case of a married couple, each spouse may contribute the amount listed):

| Age 49 and Below | Age 50 and Above | |

|---|---|---|

| 1998–2001 | $2,000 | $2,000 |

| 2002–2004 | $3,000 | $3,500 |

| 2005 | $4,000 | $4,500 |

| 2006–2007 | $4,000 | $5,000 |

| 2008–2012 | $5,000 | $6,000 |

| 2013–2018[1] | $5,500 | $6,500 |

| 2019-2020[2] | $6,000 | $7,000 |

History

Originally called an "IRA Plus", the idea was proposed by Senator Bob Packwood of Oregon and Senator William Roth of Delaware in 1989.[3] The Packwood–Roth plan would have allowed individuals to invest up to $2,000 in an account with no immediate tax deductions, but the earnings could later be withdrawn tax-free at retirement.[3]

The Roth IRA was established by the Taxpayer Relief Act of 1997 (Public Law 105-34) and named for Senator Roth, its chief legislative sponsor. In 2000, 46.3 million taxpayers held IRA accounts worth a total of $2.6 trillion in value according to the Internal Revenue Service (IRS). Only a little over $77 billion of that amount was held in Roth IRAs. By 2007, the number of IRA owners has jumped to over 50 million taxpayers with $3.3 trillion invested.[4]

In 1997, then-Senator William Roth (R-Del) wanted to restore the traditional IRA which had been repealed in 1986, and the upfront tax deduction that goes with it. Under congressional budget rules, which work within a 10-year window, the revenue cost of giving that tax break to everyone was too high. So his staff limited deductible IRAs to people with very low income, and made Roth IRAs (initially with income limitations) available to others. That slid the revenue cost outside the 10-year window and got the legislation out from under the budget rules.[5]

Economists have warned about exploding future revenue losses associated with Roth IRAs. With these accounts, the government is "bringing in more now, but giving up much more in the future," said economist and Forbes contributor Leonard Burman. In a study for The Tax Policy Center, Burman calculated that from 2014 to 2046, the Treasury would lose a total of $14 billion as a result of IRA-related provisions in the 2006 tax law. The losses stem from both Roth conversions and the ability to make nondeductible IRA contributions and then immediately convert them to Roths.[5]

Differences from a traditional IRA

In contrast to a traditional IRA, contributions to a Roth IRA are not tax-deductible. Withdrawals are tax-free under certain conditions (for example, if the withdrawal is only on the principal portion of the account, or if the owner is at least 59½ years old). A Roth IRA has fewer withdrawal restrictions than traditional IRAs. Transactions inside a Roth IRA (including capital gains, dividends, and interest) do not incur a current tax liability.

Advantages

- Direct contributions to a Roth IRA (principal) may be withdrawn tax and penalty-free at any time.[6] Earnings may be withdrawn tax and penalty-free after 5 years if the condition of age 59½ (or other qualifying condition) is also met. Rollover, converted (before age 59½) contributions held in a Roth IRA may be withdrawn tax and penalty-free after 5 years. Distributions from a Roth IRA do not increase Adjusted Gross Income. This differs from a traditional IRA, where all withdrawals are taxed as ordinary income, and a penalty applies for withdrawals before age 59½. Even capital gains on stocks or other securities held in a regular taxable account, so long as they are held for at least a year, are generally treated more advantageously than traditional IRA withdrawals, being taxed not as Ordinary Income, but at the lower Long-Term Capital Gain rate. This potentially higher tax rate for withdrawals of capital gains from a traditional IRA is a quid pro quo for the deduction taken against ordinary income when putting money into the IRA.

- Up to a lifetime maximum $10,000 in earnings, withdrawals are considered qualified (tax-free) if the money is used to acquire a principal residence for the Roth IRA owner. This principal residence must be acquired by the Roth IRA owner, their spouse, or their lineal ancestors and descendants. The owner or qualified relative who receives such a distribution must not have owned a home in the previous 24 months.

- Contributions may be made to a Roth IRA even if the owner participates in a qualified retirement plan such as a 401(k). (Contributions may be made to a traditional IRA in this circumstance, but they may not be tax deductible.)

- If a Roth IRA owner dies, and his/her spouse becomes the sole beneficiary of that Roth IRA while also owning a separate Roth IRA, the spouse is permitted to combine the two Roth IRAs into a single plan without penalty.

- If the Roth IRA owner expects that the tax rate applicable to withdrawals from a traditional IRA in retirement will be higher than the tax rate applicable to the funds earned to make the Roth IRA contributions before retirement, then there may be a tax advantage to making contributions to a Roth IRA over a traditional IRA or similar vehicle while working. There is no current tax deduction, but money going into the Roth IRA is taxed at the taxpayer's current marginal tax rate, and will not be taxed at the expected higher future effective tax rate when it comes out of the Roth IRA. There is always risk, however, that retirement savings will be less than anticipated, which would produce a lower tax rate for distributions in retirement. Assuming substantially equivalent tax rates, this is largely a question of age. For example, at the age of 20, one is likely to be in a low tax bracket, and if one is already saving for retirement at that age, the income in retirement is quite likely to qualify for a higher rate, but at the age of 55, one may be in peak earning years and likely to be taxed at a higher tax rate, so retirement income would tend to be lower than income at this age and therefore taxed at a lower rate.

- Assets in the Roth IRA can be passed on to heirs.

- The Roth IRA does not require distributions based on age. All other tax-deferred retirement plans, including the related Roth 401(k),[7] require withdrawals to begin by April 1 of the calendar year after the owner reaches age 70½. If the account holder does not need the money and wants to leave it to their heirs, a Roth can be an effective way to accumulate tax-free income. Beneficiaries who inherit Roth IRAs are subject to the minimum distribution rules.

- Roth IRAs have a higher "effective" contribution limit than traditional IRAs, since the nominal contribution limit is the same for both traditional and Roth IRAs, but the post-tax contribution in a Roth IRA is equivalent to a larger pre-tax contribution in a traditional IRA that will be taxed upon withdrawal. For example, a contribution of the 2008 limit of $5,000 to a Roth IRA may be equivalent to a traditional IRA contribution of $6667 (assuming a 25% tax rate at both contribution and withdrawal). In 2008, one cannot contribute $6667 to a traditional IRA due to the contribution limit, so the post-tax Roth contribution may be larger.

- On estates large enough to be subject to estate taxes, a Roth IRA can reduce estate taxes since tax dollars have already been subtracted. A traditional IRA is valued at the pre-tax level for estate tax purposes.

- Most employer sponsored retirement plans tend to be pre-tax dollars and are similar, in that respect, to a traditional IRA, so if additional retirement savings are made beyond an employer-sponsored plan, a Roth IRA can diversify tax risk.

- Unlike distributions from a regular IRA, qualified Roth distributions do not affect the calculation of taxable social security benefits.[8]

- Roth Conversions not only convert highly taxed IRA income to tax-free income, but if the IRA holds alternative assets such as REITs (Real Estate Investment Trusts), Leasing Programs, Oil and Gas Drilling Partnerships and Royalty Partnerships, a Fair Market Valuation (FMV) or "Substantially Discounted Roth-Conversion" may provide reductions in the conversion income tax by up to 75%, possibly more, depending on assets and the Fair Market Valuation.

- Roth Conversions using the FMV or "Substantially Discounted Roth-Conversion" may reduce the estate tax attributed to IRA's on large estates by up to 75%, or more, depending on the assets held at the time of conversion.

- Roth Conversions main benefit is in the conversion of highly taxed IRA income to tax-free Roth income, however Roth-Conversion income does not add to MAGI, hence reducing the taxpayers Medicare Part B Premiums (another tax).

- FMV or "Substantially Discounted Roth-Conversion" may allow the taxpayer to reduce RMDs by up to 75%.

Disadvantages

- Funds that reside in a Roth IRA cannot be used as collateral for a loan per current IRS rules and therefore cannot be used for financial leveraging or as a cash management tool for investment purposes.

- Contributions to a Roth IRA are not tax deductible. By contrast, contributions to a traditional IRA are tax deductible (within income limits). Therefore, someone who contributes to a traditional IRA instead of a Roth IRA gets an immediate tax savings equal to the amount of the contribution multiplied by their marginal tax rate while someone who contributes to a Roth IRA does not realize this immediate tax reduction. Also, by contrast, contributions to most employer sponsored retirement plans (such as a 401(k), 403(b), Simple IRA or SEP IRA) are tax deductible with no income limits because they reduce a taxpayer's adjusted gross income.

- Eligibility to contribute to a Roth IRA phases out at certain income limits. By contrast, contributions to most tax deductible employer sponsored retirement plans have no income limit.

- Contributions to a Roth IRA do not reduce a taxpayer's adjusted gross income (AGI). By contrast, contributions to a traditional IRA or most employer sponsored retirement plans reduce AGI. Reducing one's AGI has a benefit (besides reducing taxable income) if it puts the AGI below some threshold to make the taxpayer eligible for tax credits or deductions that would not be available at the higher AGI with a Roth IRA. The amount of credits and deductions may increase as the taxpayer slides down the phaseout scale. Examples include the child tax credit, the earned income credit, the student loan interest deduction.

- A Roth IRA contribution is taxed at the taxpayer's current income tax rate, which is higher than the income tax rate during retirement for most people. This is because most people have a lower income, that falls in a lower tax bracket, during retirement than during their working years. (A lower tax rate can also occur if Congress lowers income tax rates before retirement.) By contrast, contributions to traditional IRAs or employer-sponsored tax-deductible retirement plans result in an immediate tax savings equal to the taxpayer's current marginal tax bracket multiplied by the amount of the contribution. The higher the taxpayer's current marginal tax rate, the higher the potential disadvantage. However, this issue is more complicated because withdrawals from traditional IRA or employer sponsored tax deductible retirement plans are fully taxable, up to 85% of Social Security income is taxable, personal residence mortgage interest deduction decreases as the mortgage is paid down, and there may be pension plan income, investment income and other factors.

- A taxpayer who pays state income taxes and who contributes to a Roth IRA (instead of a traditional IRA or a tax deductible employer sponsored retirement plan) will have to pay state income taxes on the amount contributed to the Roth IRA in the year the money is earned. However, if the taxpayer retires to a state with a lower income tax rate, or no income taxes, then the taxpayer will have given up the opportunity to avoid paying state income taxes altogether on the amount of the Roth IRA contribution by instead contributing to a traditional IRA or a tax deductible employer sponsored retirement plan, because when the contributions are withdrawn from the traditional IRA or tax deductible plan in retirement, the taxpayer will then be a resident of the low or no income tax state, and will have avoided paying the state income tax altogether as a result of moving to a different state before the income tax became due.

- The perceived tax benefit may never be realized. That is, one might not live to retirement or much beyond, in which case the tax structure of a Roth only serves to reduce an estate that may not have been subject to tax. To fully realize the tax benefit, one must live until one's Roth IRA contributions have been withdrawn and exhausted. By contrast, with a traditional IRA, tax might never be collected at all, such as if one dies before retirement with an estate below the tax threshold, or retires with income below the tax threshold. (To benefit from this exemption, the beneficiary must be named in the appropriate IRA beneficiary form. A beneficiary inheriting the IRA solely through a will is not eligible for the estate tax exemption. Additionally, the beneficiary will be subject to income tax unless the inheritance is a Roth IRA.) Heirs will have to pay taxes on withdrawals from traditional IRA assets they inherit, and must continue to take mandatory distributions (although they will be based on their life expectancy). It is also possible that tax laws may change by the time one reaches retirement age.

- Congress may change the rules that allow for tax-free withdrawal of Roth IRA contributions. Therefore, someone who contributes to a traditional IRA is guaranteed to realize an immediate tax benefit, whereas someone who contributes to a Roth IRA must wait for a number of years before realizing the tax benefit, and that person assumes the risk that the rules might be changed during the interim. On the other hand, taxing earnings on an account which were promised to be untaxed may be seen as a violation of contract and completely defeat the purpose of Roth IRAs as encouraging saving for retirement – individuals contributing to a Roth IRA now may in fact be saving themselves from new, possibly higher income tax obligations in the future. However, the federal government is not restricted by the Contract Clause of the U.S. Constitution that prohibits "Law[s] impairing the Obligation of Contracts". By its terms, this prohibition applies only to state governments.

Double taxation

Double taxation may still occur within these tax sheltered investment plans. For example, foreign dividends may be taxed at their point of origin, and the IRS does not recognize this tax as a creditable deduction. There is some controversy over whether this violates existing Joint Tax Treaties, such as the Convention Between Canada and the United States of America With Respect to Taxes on Income and on Capital.[9]

For Canadians with U.S. Roth IRAs: A new rule (2008) provides that Roth IRAs (as defined in section 408A of the U.S. Internal Revenue Code) and similar plans are considered to be pensions. Accordingly, distributions from a Roth IRA (as well as other similar plans) to a resident of Canada will generally be exempt from Canadian tax to the extent that they would have been exempt from U.S. tax if paid to a resident of the U.S. Additionally, a resident of Canada may elect to defer any taxation in Canada with respect to income accrued in a Roth IRA but not distributed by the Roth IRA, until and to the extent that a distribution is made from the Roth IRA or any plan substituted therefor. The effect of these rules is that, in most cases, no portion of the Roth IRA will be subject to taxation in Canada.

However, where an individual makes a contribution to a Roth IRA while they are a resident of Canada (other than rollover contributions from another Roth IRA), the Roth IRA will lose its status as a "pension" for purposes of the Treaty with respect to the accretions from the time such contribution is made. Income accretions from such time will be subject to tax in Canada in the year of accrual. In effect, the Roth IRA will be bifurcated into a "frozen" pension that will continue to enjoy the benefit of the exemption for pensions and a non-pension (essentially a savings account) that will not.

Eligibility

Income limits

Congress has limited who can contribute to a Roth IRA based upon income. A taxpayer can contribute the maximum amount listed at the top of the page only if their Modified Adjusted Gross Income (MAGI) is below a certain level (the bottom of the range shown below). Otherwise, a phase-out of allowed contributions runs proportionally throughout the MAGI ranges shown below. Once MAGI hits the top of the range, no contribution is allowed at all; however, a minimum of $200 may be contributed as long as MAGI is below the top of the range (e.g., a single 40-year-old with MAGI $124,999 may still contribute $200 to a Roth IRA vs. $30). Excess Roth IRA contributions may be recharacterized into Traditional IRA contributions as long as the combined contributions do not exceed that tax year's limit. The Roth IRA MAGI phase out ranges for 2019 are:[10]

- Single filers: Up to $122,000 (to qualify for a full contribution); $122,000–$137,000 (to be eligible for a partial contribution)

- Joint filers: Up to $189,000 (to qualify for a full contribution); $193,000–$203,000 (to be eligible for a partial contribution)

- Married filing separately (if the couple lived together for any part of the year): $0 (to qualify for a full contribution); $0–$10,000 (to be eligible for a partial contribution).

The lower number represents the point at which the taxpayer is no longer allowed to contribute the maximum yearly contribution. The upper number is the point as of which the taxpayer is no longer allowed to contribute at all. People who are married and living together, but who file separately, are only allowed to contribute a relatively small amount.

However, once a Roth IRA is established, the balance in the plan remains tax-sheltered, even if the taxpayer's income rises above the threshold. (The thresholds are just for annual eligibility to contribute, not for eligibility to maintain a Roth IRA.)

To be eligible, one must meet the earned income minimum requirement. In order to make a contribution, one must have taxable compensation (not taxable income from investments). If one makes only $2,000 in taxable compensation, one's maximum IRA contribution is $2,000.

If a taxpayer's income exceeds the income limits, they may still be able to effectively contribute by using a "backdoor" contribution process (see #Traditional IRA conversion as a workaround to Roth IRA income limits below).

Contribution limits

Contributions to both a Roth IRA and a traditional IRA are limited to the total amount allowed for either of them.[11] Generally, the contribution cannot exceed your earned income for the year in question. The one exception is for a "spousal IRA" where a contribution can be made for a spouse with little or no earned income provided the other spouse has sufficient earned income and the spouses file a joint tax return.[12]

Conversion rules

The government allows people to convert Traditional IRA funds (and some other untaxed IRA funds) to Roth IRA funds by paying income tax on any account balance being converted that has not already been taxed (e.g., the Traditional IRA balance minus any non-deductible contributions).[13]

Prior to 2010, two circumstances prohibited conversions: Modified Adjusted Gross Income exceeding $100,000 or the participant's tax filing status is Married Filing Separately. These limitations were removed as part of the Tax Increase Prevention and Reconciliation Act of 2005.

Traditional IRA conversion as a workaround to Roth IRA income limits

Regardless of income but subject to contribution limits, contributions can be made to a Traditional IRA and then converted to a Roth IRA.[14] This allows for "backdoor" contributions where individuals are able to avoid the income limitations of the Roth IRA.[15]

One major caveat to the entire "backdoor" Roth IRA contribution process, however, is that it only works for people who do not have any pre-tax contributed money in IRA accounts at the time of the "backdoor" conversion to Roth; conversions made when other IRA money exists are subject to pro-rata calculations and may lead to tax liabilities on the part of the converter.[13]

For example, if someone has contributed $10,000 post-tax and $30,000 pre-tax to a traditional IRA and wants to convert the post tax $10,000 into a Roth, the pro-rated amount (ratio of taxable contributions to total contributions) is taxable. In this example, $7500 of the post tax contribution is considered taxable when converting it to a Roth IRA. The pro-rata calculation is made based on all traditional IRA contributions across all the individual's traditional IRA accounts (even if they are in different institutions).

Distributions

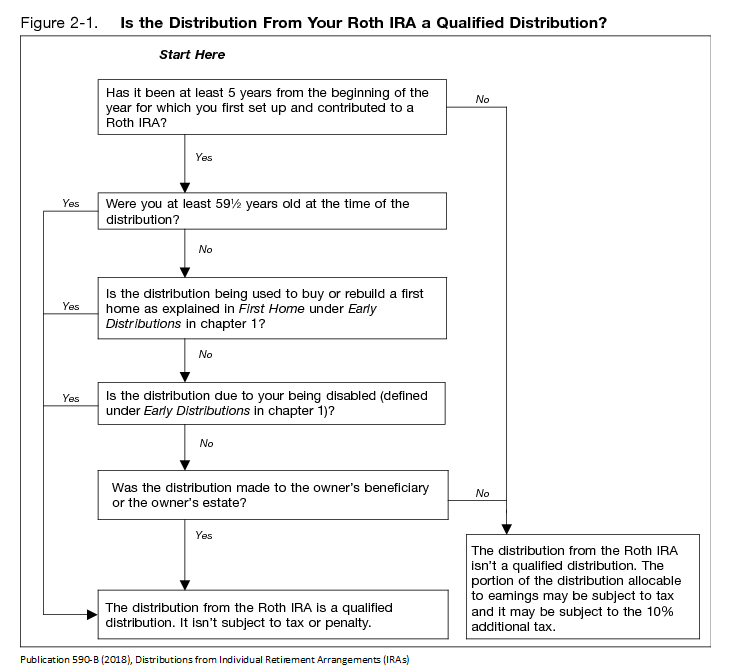

Returns of your regular contributions from your Roth IRA(s) are always withdrawn tax and penalty-free.[6] Eligible (tax and penalty-free) distributions of earnings must fulfill two requirements. First, the seasoning period of five years since the opening of the Roth IRA account must have elapsed, and secondly a justification must exist such as retirement or disability. The simplest justification is reaching 59.5 years of age, at which point qualified withdrawals may be made in any amount on any schedule. Becoming disabled or being a "first time" home buyer can provide justification for limited qualified withdrawals. Finally, although one can take distributions from a Roth IRA under the substantially equal periodic payments (SEPP) rule without paying a 10% penalty,[16] any interest earned in the IRA will be subject to tax[17]—a substantial penalty which forfeits the primary tax benefits of the Roth IRA.

Inherited Roth IRAs

When a spouse inherits a Roth IRA:

- the spouse can combine the Roth IRA with his or her own Roth IRA

- the spouse can make contributions and otherwise control the account

- required minimum distributions do not apply

- income tax does not apply to distributions

- estate tax (if any) does not apply at the time of transfer

When a non-spouse inherits a Roth IRA:

- the non-spouse cannot combine the Roth IRA with his or her own

- the non-spouse cannot make additional contributions

- required minimum distributions apply

- income tax does not apply to distributions, if the Roth IRA was established for at least five years before the distribution occurs.[18]

- estate tax (if any) applies

In addition, the beneficiary may elect to choose from one of two methods of distribution. The first option is to receive the entire distribution by December 31 of the fifth year following the year of the IRA owner's death. The second option is to receive portions of the IRA as distributions over the life of the beneficiary, terminating upon the death of the beneficiary and passing on to a secondary beneficiary. If the beneficiary of the Roth IRA is a trust, the trust must distribute the entire assets of the Roth IRA by December 31 of the fifth year following the year of the IRA owner's death, unless there is a "Look Through" clause, in which case the distributions of the Roth IRA are based on the Single Life Expectancy table over the life of the beneficiary, terminating upon the death of the beneficiary. Subtract one (1) from the "Single Life Expectancy" for each successive year. The age of the beneficiary is determined on 12/31 of the first year after the year that the owner died.

See also

- Retirement plans in the United States

- Comparison of 401(k) and IRA accounts – 401(k) & IRA comparisons (401(k) vs Roth 401( k) vs Traditional IRA vs Roth IRA)

- Form 1099-R

- Coverdell Education Savings Account – sometimes termed the "Roth IRA for Education", describes tax-sheltered savings accounts for college.

- Substantially equal periodic payments (SEPP) – an exception to the age 59.5 rule

- myRA - a 2014 Obama administration initiative based on the Roth IRA

- Tax-Free Savings Account in Canada since 2008

- Individual Savings Account in the United Kingdom since 1999

References

- "IRA FAQs - Contributions". www.irs.gov. Retrieved 2016-09-02.

- "401(k) contribution limit increases to $19,000 for 2019; IRA limit increases to $6,000". www.irs.gov. Retrieved 2018-11-10.

- Blustein, Paul (October 21, 1989). "Critics Call New IRA Plan a Budget Gimmick: Backers See Proposal as Idel Way to Spur Savings, Cut Deficit". The Washington Post. p. D12. ProQuest 139926770.

- "What Senator William Roth Envisioned For The Roth IRA". rothira.com. 2011-08-30. Retrieved 2016-09-02.

- Jacobs, Deborah L. "Why--And How--Congress Should Curb Roth IRAs". Forbes.

- "Publication 590-B (2014), Individual Retirement Arrangements (IRAs)". Irs.gov. Retrieved October 7, 2015.

- See Final IRS Regulations, passed December 30, 2005 not exempting Roth 401(k) from mandatory distributions at age 70½.

- Internal Revenue Code Section 86(b)(2)(B)

- "Status of Tax Treaty Negotiations". fin.gc.ca. Department of Finance Canada. Retrieved 2016-09-02.

- "Amount of Roth IRA Contributions That You Can Make For 2019". irs.gov. Internal Revenue Service. Retrieved 2018-01-01.

- "Publication 17 (2013), Your Federal Income Tax". Irs.gov. June 30, 1943. Retrieved April 15, 2014.

- "Publication 590-A (2015), Contributions to Individual Retirement Arrangements (IRAs)". Irs.gov. Retrieved 2016-08-23.

- Steinberg, Joseph (2012). "Warning About Roth IRA Conversions: Often Misunderstood IRS Rule Can Cost You Money and Aggravation". Forbes. Forbes. Retrieved December 12, 2012.

- Bader, Mary; Schroeder, Steve (2009). "TIPRA and the Roth IRA, New Planning Opportunity for High-Income Taxpayers". The CPA Journal. The New York State Society of CPAs. Retrieved January 31, 2012.

- https://www.modestmoney.com/roth-ira-conversion-ladder-for-early-retirees-decoded/40950. Missing or empty

|title=(help) - IRS Publication 590, Chapter 2, "Additional Tax on Early Distributions"

- IRS Publication 590, Chapter 2, Worksheet 2–3

- IRS Publication 590 (2010), "What is a Qualified Distribution"

Further reading

- Bledsoe, John D. (1998). Roth to Riches: The Ordinary to Roth IRA handbook. Dallas, TX: Legacy Press. ISBN 0-9629114-1-0. OCLC 40158081.

- Daryanani, Gobind (1998). Roth IRA Book: An Investor's Guide: Including a Personal Interview with Senator William V. Roth, Jr. (R-De), Chairman, U.S. Senate Finance Committee. Bernardsville, NJ: Digiqual Inc. ISBN 0-9665398-1-8. OCLC 40340829.

- Merritt, Steve (1998). All about the New IRA, Roth, Traditional, Educational: How to Cash in on the New Tax Law Changes. Melbourne, FL: Halyard Press. ISBN 1-887063-07-2. OCLC 39363078.

- Slesnick, Twila; Suttle, John C. (2007). IRAs, 401(k)s, & Other Retirement Plans: Taking Your Money Out (8th ed.). Berkeley, CA: Nolo. ISBN 978-1-4133-0696-5. OCLC 85162294.

- Thomas, Kaye A. (2004). Fairmark Guide to the Roth IRA: Retirement Planning in Plain Language. Lisle, IL: Fairmark Press, Inc. ISBN 0-9674981-0-4. OCLC 55048948.

- Trock, Gary R. (1998). The Roth IRA Made Simple. Grifith, IN: Conquest Pub. ISBN 0-9666227-0-7. OCLC 40641031.

External links

- IRS Publication 590 (IRAs) (pdf)

- Comparision Roth IRA vs Traditional IRA

- Humberto Cruz (February 13, 2010). "Traditional to Roth IRA conversions: Don't be tripped up by tax implications". The Boston Globe.

- Rothify Your 401(k) Forbes.com

- IRA Limits sites.google.com